TL;DR

Most banks evaluating tokenized receivables platforms lack a structured procurement framework. This guide fills that gap. It adds three layers most RFP guides skip: production architecture blueprints, measurable operational benchmarks, and failure scenario testing. Every section is vendor-neutral and built for bank procurement teams.

Why a Structured RFP Matters

The BIS highlights how tokenization of deposits and financial assets is moving into institutional use cases. For banks evaluating receivables collateral, the question is shifting from concept validation to platform readiness.

A platform strong on invoice ingestion may lack legal control support. Strong APIs may come with weak failure recovery. No vendor excels equally across all dimensions. A well-structured RFP prompts vendors to respond on the bank’s terms and exposes gaps before the contract is signed.

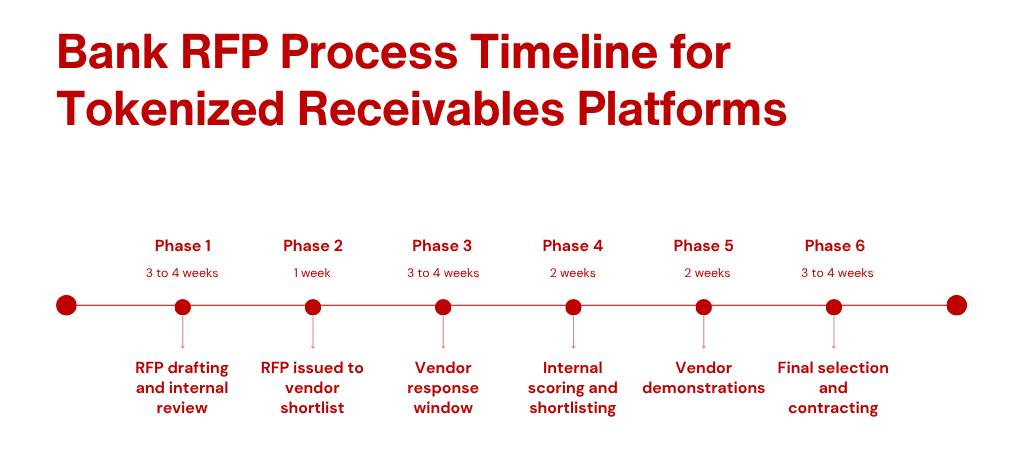

Section 1: RFP Structure Overview

A well-structured RFP helps banks evaluate vendors consistently and align platform selection with business objectives.

Scope statement: Define the boundaries of the program: invoice volume, debtor jurisdictions, currency requirements, environment for integration.

Scoring weights: More weight should be given to legal and compliance in a bank with complex cross border programs. A bank prioritizing speed to market should weight API readiness higher.

Notes: Timeline durations are indicative only and should be adapted to the bank's procurement processes, governance requirements, and project scope.

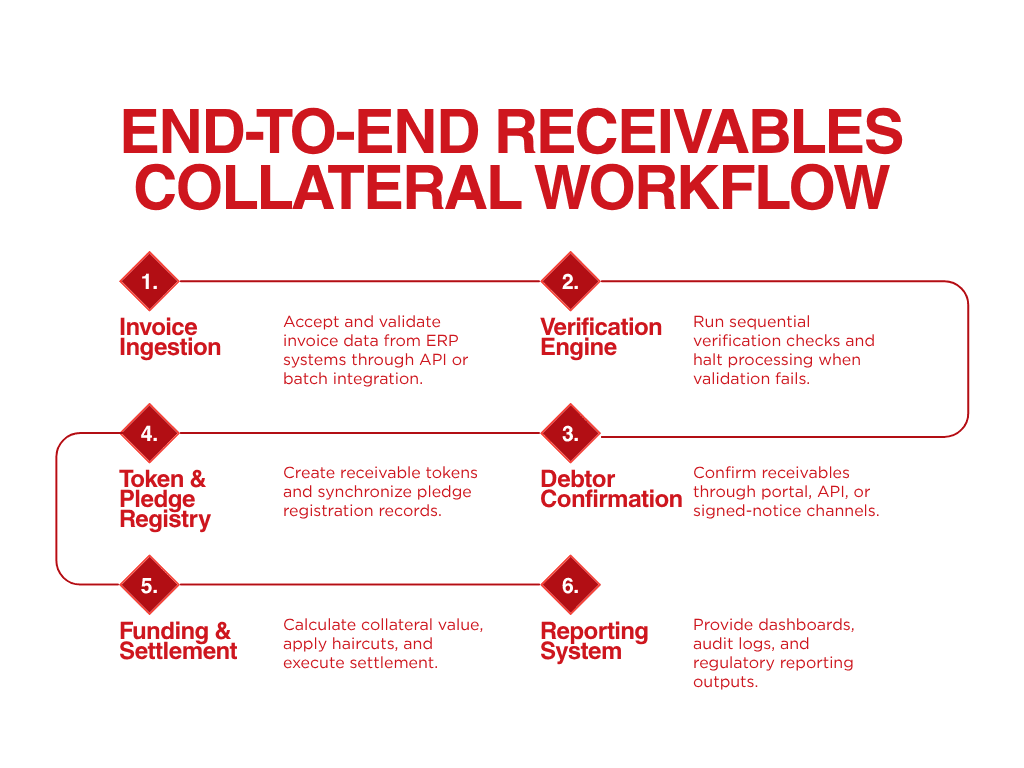

Section 2: Reference Architecture Blueprint

Bank-grade RFPs require vendors to demonstrate a complete end-to-end architecture. The required workflow runs in six stages:

ERP to Invoice Ingestion. The platform must accept structured invoice data via API and batch modes. The platform must validate field completeness and perform hash-based de-duplication. The platform must reject invalid records with logged error codes.

Verification Engine. The engine must run all eight verification checks in sequence. Each check must be atomic. A failure halts the sequence and logs the specific failure reason.

Debtor Confirmation. The module must operate independently from the verification engine. It must support portal-based, API-based, and signed-notice channels.

Token Registry to Pledge Registry. A token minted in the token registry must trigger an immediate pledge registration event. Synchronization latency must be measurable and reported.

Funding Engine to Settlement Layer. Before triggering settlement, the funding engine has to calculate the eligible collateral value, apply configured haircuts and record the advance amount. Settlement must support tokenized deposits, regulated stablecoins and traditional cash.

Reporting System. Must support real-time dashboards, scheduled regulatory exports and on-demand retrieval of audit logs.

Architecture Stage | Key Requirement | Vendor Demonstration Required |

Invoice Ingestion | Hash deduplication, rejection logging | Live ERP ingestion in sandbox |

Verification Engine | Sequential checks, atomic failure handling | Failure injection test |

Debtor Confirmation | Multi-channel, cryptographic signing | Portal and API confirmation demo |

Token to Pledge Registry sync | Sub-60-second synchronization | Latency measurement in sandbox |

Funding to Settlement | Haircut calculation, multi-asset support | End-to-end funding flow demo |

Reporting System | Real-time and scheduled export | Regulatory export sample |

Section 3: Production Architecture Governance

Production deployments require governance controls that ensure operational integrity, security, and accountability.

Multi-admin approval workflows. Pledge registration above a defined threshold, advance disbursement, and pledge release each require dual or multi-party sign-off.

RBAC governance layers. Role permissions must be technically enforced at the platform layer. No user should escalate their own permissions without a separate authorization event.

MFA at action level. Token issuance, pledge registration and pledge release should be subject to multi-factor authentication. MFA via login only is not sufficient.

Compliance module controls. The platform must include four tools: asset freeze for receivables under investigation, debtor blacklist management, exception management workflows, and a compliance event log separate from the operational log.

Section 4: Measurable Operational Benchmarks

Vendors must disclose the following benchmarks from at least two production deployments.

Debtor confirmation turnaround. Target: under 24 hours. Vendors must state median and 95th percentile times from production data.

Accuracy of duplicate financing detection. Target: false negative rate < 0.1%. Vendors must state their detection rate and measurement methodology.

Registry synchronization latency. Target: under 60 seconds from pledge registration to confirmed sync. Latency above this creates priority ambiguity.

Reconciliation exception rate. Goal: Under 2 percent of payment events should require manual intervention. Higher rates indicate that the process is not mature.

Audit log export performance. Target: under 4 hours for a 10,000-event export. Vendors must state export times for defined portfolio sizes.

Benchmark | Bank-Grade Target | What Vendors Must Disclose |

Debtor confirmation turnaround | Under 24 hours | Median and 95th percentile from production |

Duplicate detection accuracy | False negative rate below 0.1% | Detection rate and measurement methodology |

Registry synchronization latency | Under 60 seconds | Average and peak latency from production |

Reconciliation exception rate | Below 2% | Exception rate from at least two live programs |

Audit log export performance | Under 4 hours for 10,000 events | Export times across defined portfolio sizes |

Vendors that can only provide estimates from pilots have not proven performance at scale.

Section 5: Failure and Exception Scenario Testing

Banks must require vendors to demonstrate these five scenarios in a sandbox before contract signature.

Scenario 1: Registry outage during pledge registration. The platform should queue the request, retry on a defined schedule, and keep the invoice in pending status. It should not move to funding until registration is confirmed. The bank should get an alert within 5 minutes.

Scenario 2 : Revocation of debtor after confirmation. The platform should stop funding immediately, change the confirmation status to Revoked, inform the bank and seller and record the revocation with timestamp and reason code.

Duplicate financing detected after funding. The platform should flag the position, freeze the collateral record, send a notice to compliance and kick off a manual review workflow. The platform should not release the pledge until the review is resolved.

Scenario 4: Partial repayment combined with dispute status. The platform is to apply the partial payment to reduce the outstanding advance, hold the disputed part separately, keep the pledge on the disputed balance and alert collections.

Scenario 5: Settlement asset failure. The platform needs to stop paying out, inform the treasury and offer a fallback to another settlement asset or manual workflow without complete re-initiation.

Failure Scenario | Expected Platform Behavior | Pass Criteria |

Registry outage during pledge | Queue, retry, hold pending, alert within 5 minutes | Sandbox demo with timing logs |

Debtor revocation after confirmation | Halt funding, update status, notify parties, log event | Full event trail in audit log |

Duplicate detected post-funding | Freeze position, notify compliance, trigger review | No release until review resolves |

Partial repayment with dispute | Split status, maintain pledge on disputed balance, alert collections | Correct balance split in dashboard |

Settlement asset failure | Pause disbursement, alert treasury, offer fallback | Fallback demonstrated without re-initiation |

Failure Patterns Banks Should Test During Vendor Sandboxes

Banks evaluating tokenized collateral platforms should watch for three recurring failure modes during vendor sandbox testing:

Reconciliation drift under concurrent load. During high-volume tests, payment webhooks fire out of sequence. The platform applies partial payments before full confirmation, creating false "Funded" collateral positions. This typically indicates immature event-queue handling.

Post-funding duplicate detection gaps. Vendors demonstrate pre-funding deduplication well but fail to flag duplicate pledges submitted after funding begins. This gap causes priority ambiguity and delayed compliance escalation in live programs.

Overpromised registry sync latency. Vendors claim sub-60-second sync in marketing materials but deliver 3–10 minutes under concurrent load. This creates enforcement timing risk during pledge registration peaks.

Request vendors disclose how their architecture handles these specific patterns. Sandbox tests should simulate concurrent loads and exception injection, not single-transaction flows.

Section 6: Legal, Technical, Security, and Settlement

Legal control is not a compliance checkbox. It is the foundation of collateral validity. A platform with flawless APIs and fast settlement cannot compensate for weak assignment mechanics or unenforceable pledge records.

Assignment and perfection support. The platform must generate formal assignment notices, support jurisdiction-specific perfection filing outputs, and maintain an immutable audit trail exportable for regulatory review. Legal control must be provable, not assumed.

Cross-border enforceability. If the program spans multiple debtor jurisdictions, the platform must document how pledge records align with local secured transactions law. Token registry entries alone do not substitute for statutory filing, debtor notice, or UCC, MLETR, or local secured transactions requirements where applicable.

Enforcement readiness. In a default scenario, the platform must allow the bank to freeze receivables, trigger collection workflows, and export a complete chain-of-custody log within one business day. Delayed export, missing timestamps, or unstructured legal documentation weaken enforcement positions and complicate insolvency proceedings.

Read Bank-Grade API Requirements for Tokenized Trade Collateral Platforms for the full API specification.

Read Vendor Due Diligence for Tokenized Trade Collateral: Security, Privacy, Compliance, and Auditability for the full due diligence framework.

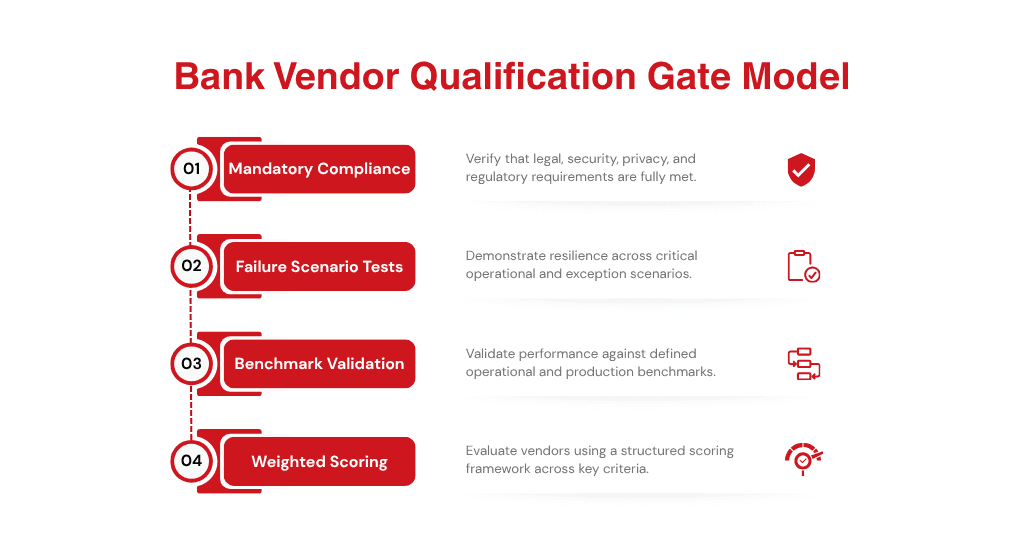

Section 7: Vendor Evaluation and Scoring Template

A structured evaluation framework helps banks compare vendors consistently and objectively.

Support model. Dedicated implementation support? Escalation paths for critical issues?

Implementation timeline. What is the standard go-live timeline for a comparable bank?

Reference customers. Has the vendor deployed a production program at a regulated bank?

Total cost of ownership. All licensing, implementation, integration and ongoing support costs need to be quoted.

Read Build vs Buy vs Partner for Tokenized Receivables and Inventory Collateral Platforms for the strategic framework behind this decision.

Evaluation Area | Weight | Score (1 to 5) | Weighted Score |

Reference architecture blueprint | 20% | ||

Failure and exception scenario testing | 20% | ||

Legal and control requirements | 15% | ||

Operational benchmarks | 15% | ||

Technical requirements | 10% | ||

Security and privacy | 10% | ||

Vendor evaluation | 10% | ||

Total | 100% |

Scoring Rubric: What Each Score Means

1 (Fail): Critical gap. Missing mandatory feature, weak failure recovery, or non-compliant with legal/perfection standards. Automatically disqualifies vendor.

2 (Below Standard): Feature exists but requires heavy customization or manual workarounds. Production benchmarks not met.

3 (Meets Baseline): Core functionality works in sandbox. Benchmarks met at low volume. Legal and compliance workflows documented but not production-tested.

4 (Strong): Production-proven at scale across two or more regulated banks. All failure scenarios pass. Legal and compliance workflows automated and auditable.

5 (Exceptional): Market-leading performance. p95 registry synchronization materially below SLA under concurrent load, documented duplicate detection controls with no unresolved false negatives in tested production samples, full MLETR/UCC alignment, and real-time regulatory export without manual intervention.

Procurement Threshold Rules

Hard pass/fail gates. Vendors must pass all five failure scenario tests in the sandbox. Any failure triggers immediate disqualification.

Minimum architecture and legal scores. A weighted score below 80% in Reference Architecture or Legal/Compliance categories results in automatic shortlist exclusion.

No conditional legal compliance. Vendors claiming legal readiness must provide jurisdiction-specific implementation evidence. Marketing claims without documentation or legal-opinion alignment score 1.

Benchmark validation requirement. Vendors must attach production benchmark reports or audited performance data. Pilot-only estimates do not qualify for scores 4 or 5.

Sample RFP Questions for Vendors

Use these questions to structure your vendor evaluation:

How does your platform verify invoice uniqueness before funding?

How do you prevent post-funding duplicate pledge risk?

Which legal assignment and perfection outputs can your platform generate?

What production benchmark data can you provide for registry sync latency?

How does the system behave during registry outage or settlement asset failure?

Evaluate Tokenized Receivables Vendors With TokenMinds

Banks need more than vendor demos. They need clear RFP criteria, failure testing, legal control checks, and benchmark validation before shortlisting a platform.

TokenMinds helps procurement, product, and trade finance technology teams design vendor-neutral RFPs, score tokenized receivables platforms, and validate integration readiness from ERP ingestion to collateral settlement.

Request a vendor-neutral RFP scoring template for your bank's collateral workflow.

https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: How many vendors should a bank include in an initial RFP process?

A: Three to five. Use a request for information process first to qualify vendors. Require benchmark data at that stage. Vendors without production benchmark data should not reach the full RFP round.

Q: Should failure scenario testing be a pass or fail gate?

A: Yes. The five scenarios represent failure modes that will occur in any live program. A vendor that cannot demonstrate correct handling in a sandbox is not production-ready. Treat it as a gate that must be cleared before scored evaluation proceeds.

Q: What is the most common gap in vendor RFP responses?

A: Three gaps appear consistently. Vendors cannot provide production benchmark data. Vendors cannot demonstrate the full architecture end-to-end in a sandbox. Vendors have not built failure recovery logic for post-funding duplicate detection or settlement asset failure.

Q: What should an RFP include for tokenized receivables platforms?

A: It should include architecture requirements, invoice verification rules, debtor confirmation workflows, legal control support, registry synchronization benchmarks, settlement and reconciliation requirements, audit log exports, failure scenario tests, security controls, support model, and weighted vendor scoring.

References

Bank for International Settlements: “Tokenisation of deposits and other financial assets” (othp92). Provides institutional context on tokenization, financial asset infrastructure, and platform readiness considerations. https://www.bis.org/publ/othp92.pdf