TL;DR

Banks that run open-ended proofs of concept produce inconclusive results. Banks that define their sandbox precisely produce actionable ones. This roadmap defines a controlled 90-day pilot: one commodity type, one certified warehouse, one lender, one receipt workflow, one collateral registry, and one repayment path. It covers sandbox architecture, three phase gates, six KPIs, legal enforceability stress scenarios, warehouse operator SLAs, and a go/no-go decision framework with expansion and termination criteria.

Why Scope Discipline Determines Pilot Value

Inventory collateral pilots fail for one of two reasons. The scope is too wide to produce interpretable results. Or the scope is too narrow to test the real operational risks.

UNCITRAL-UNIDROIT Model Law on Warehouse Receipts establishes that stored goods may be used as collateral while held in a warehouse. Translating that legal framework into a working bank program requires testing specific workflow decisions under controlled conditions.

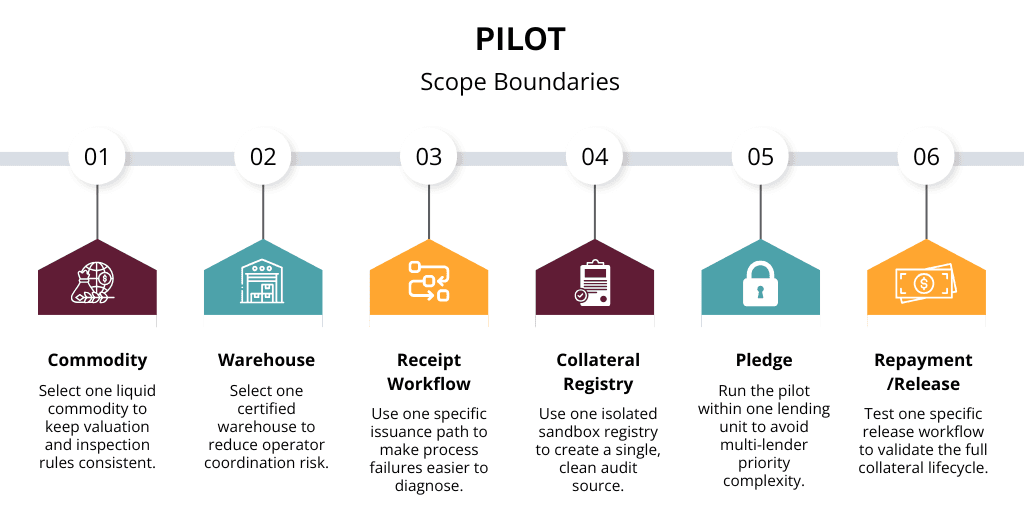

Pilot Scope Boundaries

Pilot Boundary | Recommended Scope | Why It Matters |

Commodity | One commodity type | Keeps valuation and inspection rules consistent |

Warehouse | One certified warehouse | Reduces operator coordination risk |

Lender | One lending unit | Avoids multi-lender priority complexity |

Borrower | One borrower or borrower profile | Controls credit risk variables |

Receipt workflow | One issuance and verification path | Makes process failures easier to diagnose |

Registry | One sandbox collateral registry | Creates a single audit source |

Repayment/release | One repayment and release workflow | Tests the full collateral lifecycle |

Exceptions | One escalation process | Keeps legal and operational evidence clean |

These constraints are not permanent. They are the conditions that make pilot results interpretable.

Sandbox Architecture

The pilot runs in an isolated environment. Phases one and two do not touch production systems, live customer accounts or real settlement flows.

Isolated platform instance. The tokenization and registry platform must run as a separate instance. It must have its own receipt registry, its own event log and its own API endpoints. No sandbox event appears in production dashboards.

Test data design. Use synthetic receipt data modeled on real warehouse profiles. The test data must reflect the lot sizes, grades, moisture levels, and storage conditions the bank expects in production. Unrealistic test data produces unrealistic exception rates.

Mock settlement. In Phase 1 and 2, the fund movements are simulated. There is no actual money exchanged. Phase 3 is a live transaction rehearsal in a controlled environment with the risk committee’s sign off.

Full audit logging from day one. Every event in the sandbox is logged immutably from the first day of phase one. The audit log is the primary evidence source for KPI measurement and phase gate review. A pilot that does not log from day one cannot produce a complete audit trail for regulatory review purposes.

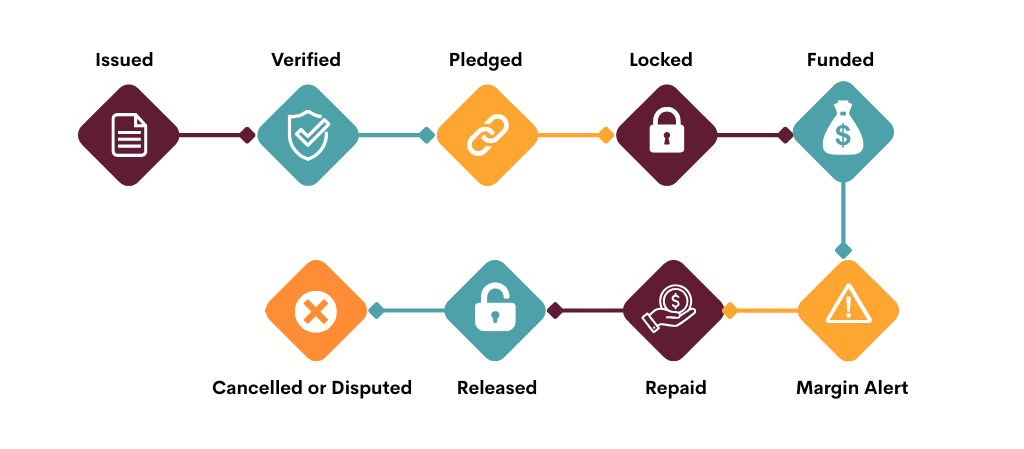

Collateral Registry State Model

The sandbox registry should track each receipt through a fixed status sequence:

Each status change should record the actor, timestamp, source system, receipt hash, warehouse confirmation, and approval evidence. This gives the bank one audit source for credit, legal, compliance, and technology review.

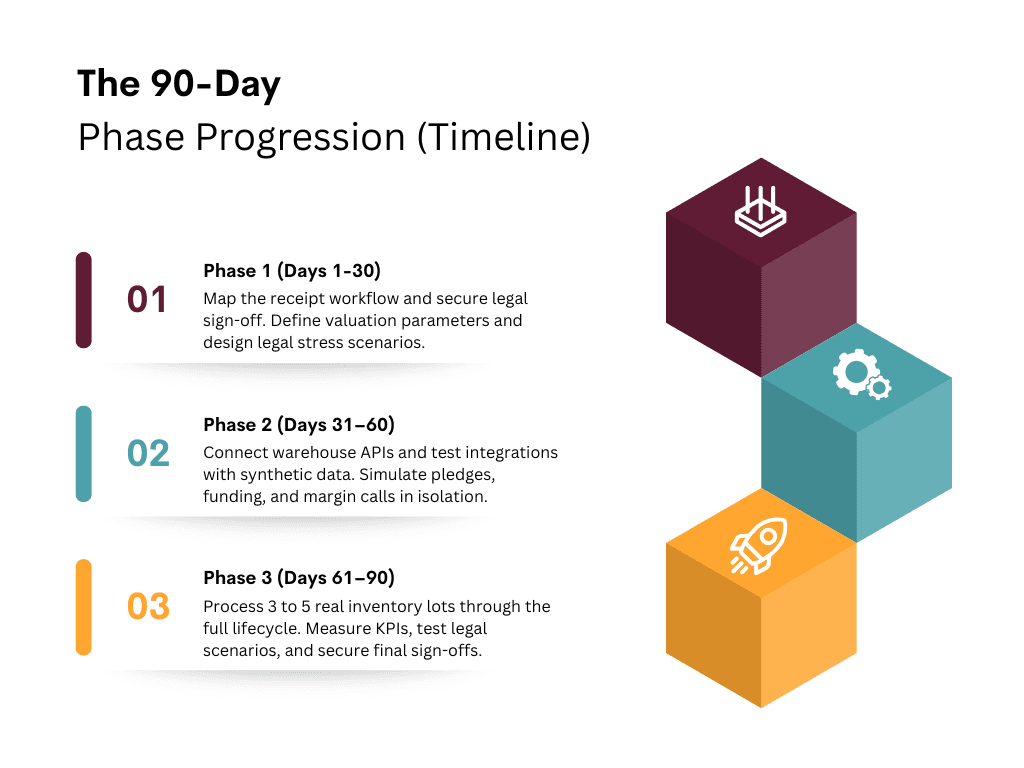

Phase 1 (Days 1 to 30): Foundation

Phase one runs four workstreams simultaneously.

Warehouse receipt digitization workflow. Map the warehouse operator's current receipt issuance process to the digital format. Identify the fields the operator can populate automatically and the fields that require manual input. Document every mapping decision. This document becomes the integration specification for phase two.

Define the unique identifier format for receipts in this pilot. Confirm that the format includes the operator's license ID and a sequential lot counter. All submissions must use the same cryptographic hash function as used on each receipt.

Legal control review. Before phase two, legal counsel must review four items. First, the warehouse agreement and whether it gives the bank instruction authority. Second, the tripartite agreement template and its relevance for the specific commodity and jurisdiction. Third, the perfection requirements for the relevant jurisdiction, including whether the bank must file in a public registry. Fourth, the enforceability of electronic receipts under local law and whether MLETR-aligned legislation applies.

This review must produce a written sign-off. Phase two does not start without it.

Valuation methodology confirmation. Confirm the price reference to be used for mark-to-market valuation. Check the update frequency. Set the margin call threshold: the percentage decrease in collateral value which requires a top up. Set the top up window: the number of business days the borrower has to react. Write these parameters into the eligibility policy before phase two begins.

Legal enforceability stress scenario design. Design two legal stress scenarios in phase one. First, test whether the borrower can dispute the bank's authority to instruct the warehouse. Second, test how the bank handles a competing creditor that claims a prior security interest after the pledge is registered. These scenarios must be designed in phase one so that legal counsel can prepare the evidence requirements before phase three begins.

Phase 1 gate criteria

Deliverable | Owner | Status Required |

Receipt field mapping document | Integration lead | Complete |

Unique identifier and hash format confirmed | Technology lead | Complete |

Legal control review sign-off | General counsel | Written approval |

Valuation methodology and margin call parameters | Credit risk lead | Documented in eligibility policy |

Legal stress scenario design | General counsel | Draft scenarios approved |

Sandbox environment deployed and tested | Technology lead | Confirmed live |

Phase 2 (Days 31 to 60): Integration and Simulation

Integration testing. Connect the warehouse operator’s issuance system to the sandbox via the defined API. Submit 30-50 synthetic receipts through the full ingestion, validation and verification process. Record pass rate, rejection rate and reasons for failure. Target a pass rate above 90 percent before moving on.

Warehouse confirmation workflow. Test the operator's confirmation channel. Submit pledge requests and measure the time from request to signed operator attestation. Identify any manual steps. The goal is to verify in less than 24 hours for a production program.

Pledge and funding simulation. Conduct pledge registration, advance calculation, and mock disbursement for 15-20 synthetic receipts. Validate each status transition log correctly. Verify the audit trail is complete for each simulated transaction.

Mark-to-market and margin call simulation. Simulate a 15% price decrease on the pilot commodity. Confirm margin call alert fires within the defined window. Confirm exception queue captures event and assigns to correct team.

Test to prevent duplicate receipts. Submit the same receipt hash twice. Confirm that the second submission is rejected automatically. Confirm that the rejection is logged with a timestamp and error code. Send a receipt with a minor data change designed to prevent hash matching. Check that the system catches it, using the secondary uniqueness check.

Phase 2 gate criteria

Metric | Target | Actual |

Receipt ingestion pass rate | Above 90% | |

Warehouse confirmation turnaround | Under 24 hours | |

Status transition log completeness | 100% of simulated receipts | |

Margin call trigger test | Fires within defined window | |

Duplicate receipt rejection | 100% of duplicate submissions caught | |

Open integration defects | Zero critical, under 3 minor |

Phase 3 (Days 61 to 90): Live Rehearsal and Go/No-Go

Live transaction rehearsal. Select three to five real lots from the pilot borrower's inventory. Run them through the full collateral lifecycle: receipt issuance, verification, pledge registration, funding, mark-to-market monitoring, repayment, and release. Use real warehouse receipts and real operator confirmations. Use real settlement only if the risk committee has approved it. Otherwise, use mock settlement with a documented cash equivalent.

Repayment and Release Workflow

Test one repayment path from borrower payment to collateral release. Confirm that repayment is matched to the correct pledged receipt, the outstanding exposure is reduced, the release instruction is sent to the warehouse, and the registry status changes from pledged or locked to released. The audit log should show payment reference, approval owner, release timestamp, warehouse acknowledgment, and final receipt status.

Step | Evidence Required |

Borrower repayment received | Payment reference and account match |

Exposure reduced | Loan balance update |

Release approved | Credit or operations approval |

Warehouse instructed | Release instruction and operator acknowledgment |

Registry updated | Receipt status changed to released |

Audit package completed | Full event log export |

KPI measurement across live rehearsal transactions

KPI | Definition | Target |

Receipt issuance time | Time from goods deposit to verified digital receipt | Under 4 hours |

Pledge confirmation time | Time from pledge request to operator attestation | Under 24 hours |

Funding cycle time | Time from verified pledge to advance disbursement | Under 24 hours |

Reconciliation break rate | Percentage of payments requiring manual reconciliation | Below 2% |

Exception rate | Percentage of receipts triggering an exception workflow | Below 5% |

Audit effort | Hours to produce a complete event log for one lot | Under 30 minutes |

Legal enforceability stress scenarios. Run the two scenarios designed in phase one against live rehearsal transactions.

Scenario A: Borrower disputes bank instruction authority.

The borrower challenges the bank's authority to instruct the warehouse. The bank must prove that the tripartite agreement gives it authority to give instructions without the borrower's consent. The evidence package supports the bank's instruction rights, and counsel confirms that no further borrower consent is required under the pilot documents unless a court order, insolvency stay, or formal dispute notice triggers an escalation process.Scenario B: Creditor with competing security interest.

A competing creditor may claim that a prior security interest covers the same inventory lot. The bank must determine if the prior security interest covers the specific lot in question. The test should show whether the bank's registry record and public filing information provide enough priority evidence to support an enforcement path within 48 hours, subject to local law and any formal dispute process.

Stress Scenario | Evidence Required | Pass Criteria |

Borrower disputes instruction authority | Tripartite agreement, operator acknowledgment | The evidence package supports the bank's instruction rights, and counsel confirms that no further borrower consent is required under the pilot documents unless a court order, insolvency stay, or formal dispute notice triggers an escalation process. |

Competing creditor asserts prior interest | Public filing search, registry timestamp | Bank can determine priority position within 48 hours, subject to local law and any formal dispute process. |

Warehouse operator SLA validation. Confirm that the warehouse operator met the following SLAs across the live rehearsal transactions.

SLA | Target |

Receipt issuance after goods deposit | Under 4 hours |

Pledge confirmation after request | Under 24 hours |

Monthly inventory confirmation | Delivered by the 5th of each month |

Response to bank audit request | Within 5 business days |

Physical re-inspection scheduling | Within 10 business days of request |

An operator that misses two or more SLAs should not move into production without remediation, replacement, or a revised operating agreement.

Go/No-Go decision framework

Function | Sign-Off Requirement |

Technology lead | Zero critical defects, all integration tests passed |

General counsel | Legal stress scenarios passed, tripartite agreement confirmed |

Credit risk lead | All KPI targets met, no unresolved margin call exceptions |

Compliance | AML, KYC, and data privacy review complete |

Transformation PMO | Phase gate documentation complete, pilot report drafted |

All five sign-offs are required for a go decision.

For the full collateral lifecycle behind this pilot, read Tokenized Inventory Collateral Guide 2026: Warehouse Receipts, Lender Control, and Audit Trails.

Governance and Risk Controls

Change management. Any change to the sandbox architecture, eligibility policy, or valuation methodology requires a documented change request. Undocumented changes invalidate phase gate evidence. The transformation PMO owns the change log.

Rollback procedures. Phase one rollback suspends the sandbox and reverts to pre-pilot state. Phase two rollback stops integration testing and reverts to phase one configuration. Phase three rollback halts live rehearsal and switches to mock settlement. Rollback triggers are to be defined before the commencement of each phase.

Compliance sign-off. The compliance team assesses the pilot against AML, KYC and data privacy requirements before phase three commences. This differs from the phase one assessment of legal control. It is intended for operational compliance, not legal enforceability.

Governance cadence. The pilot steering group should review progress weekly and approve any phase-gate movement before the next workstream begins.

Exit Criteria

Outcome | Trigger Conditions | Next Step |

Expand | All KPI targets met, all five sign-offs received | Define expansion scope within 30 days |

Extend | Minor gaps only, no blocker findings | Set 30-day remediation plan with new gate date |

Terminate | Blocker findings, legal stress scenarios failed, or material KPI misses | Root cause review before redesign |

Expansion checklist: The bank must meet five conditions before it can expand to a second commodity type or warehouse. All phase three KPI targets were met. All five go/no-go sign-offs were received. Both legal stress scenarios passed or have documented remediation plans. The warehouse operator met all SLAs during the live rehearsal. The eligibility policy has been updated to reflect pilot findings.

For a deeper KPI framework, read Operational KPIs for Tokenized Receivables and Inventory Collateral Pilots.

Design a 90-Day Inventory Collateral Sandbox With TokenMinds

Banks do not need a broad tokenization program to test inventory-backed collateral. They need a controlled pilot with clear boundaries, legal sign-offs, warehouse SLAs, measurable KPIs, and a go/no-go decision framework.

TokenMinds helps banks design tokenized inventory collateral sandboxes, map warehouse receipt workflows, define registry requirements, structure phase gates, and prepare pilot evidence for legal, risk, compliance, and technology teams.

Request a sandbox design session with TokenMinds.

Frequently Asked Questions

Q: Can a bank run this pilot without selecting a tokenization platform vendor first?

A: Phase one data mapping and legal review can proceed without a platform decision. Integration testing in phase two requires a platform. Banks that have not selected a vendor by day 20 of phase one will not meet the phase two start date.

Q: What is the minimum number of live rehearsal lots needed in phase three?

A: Three lots is the minimum. Fewer than three does not produce enough data points to validate KPIs statistically. More than ten introduces complexity that a pilot team cannot manage without production-level staffing. Three to five lots gives enough data but is still within the pilot governance constraints.

Q: Why are legal stress scenarios included in phase three rather than phase one?

A: Phase one legal review confirms the framework is correctly designed. Phase three stress scenarios confirm the framework holds under adversarial conditions with real transaction data. Running stress scenarios in phase one, before integration and warehouse confirmation workflows are tested, produces findings that cannot be acted on because the operational layer does not yet exist.

Q: How should a bank pilot tokenized inventory collateral?

A: A bank should start with one commodity type, one certified warehouse, one lending unit, one receipt workflow, one collateral registry, and one repayment and release path. The first pilot should test control, verification, valuation, pledge registration, exception handling, repayment, and release before expanding.

Q: What is a sandbox roadmap for digital warehouse receipt lending?

A: It is a controlled 90-day plan that separates design, integration, simulation, and live rehearsal. The roadmap defines phase gates, test data, warehouse confirmations, legal stress scenarios, KPIs, and go/no-go criteria before production rollout.

Q: How can banks test inventory-backed tokenization safely?

A: Banks can test safely by isolating the sandbox from production systems, using synthetic data in early phases, limiting live rehearsal to a small number of real lots, requiring legal and compliance sign-off, and using mock settlement unless risk approval is granted.

References

UNCITRAL-UNIDROIT: Model Law on Warehouse Receipts. Establishes that stored goods may be used as collateral while held in a warehouse and supports warehouse receipt systems as instruments for accessing credit.