TL;DR

Inventory collateral is well understood in asset-based lending. What is less understood is how tokenization changes the control mechanics. This guide goes beyond the standard warehouse receipt explanation. It covers collateral substitution logic, partial release workflows, legal perfection across competing creditor claims, operational exception handling, and portfolio-level governance. It maps the full bank-grade lifecycle with the specific controls that distinguish a production program from a conceptual one.

Why Inventory Collateral Matters in 2026

In 2026, commodity financing faces intense liquidity pressure. Traditional inventory collateral programs are constrained by manual inspection cycles, paper-based documentation, and fragmented warehouse operator networks.

The digitization gap in warehouse receipt systems means banks often lack real-time visibility into the physical assets backing their loans. Tokenization bridges this gap by transforming static warehouse receipts into dynamic, programmable collateral. This shift reduces operational friction, accelerates substitution workflows, and provides the cryptographic audit trails required for institutional-scale asset-based lending.

Paper vs. Tokenized Warehouse Receipts

Before detailing the control mechanics, it is essential to understand the operational shift tokenization introduces:

Dimension | Paper Warehouse Receipts | Tokenized Warehouse Receipts |

Pledge State Visibility | Manual ledger updates; delayed reporting | Real-time pledge state visibility on a shared ledger |

Audit Trail | Physical signatures; prone to loss or forgery | Automated audit trail with cryptographic timestamps and tamper-evident status records |

Fraud & Duplication Risk | High; relies on manual registry checks | Reduced; hash-based deduplication and system-level pledge locks |

Substitution Validation | Slow; requires physical document exchange | Faster; automated eligibility checks and instant token state updates |

Operational Impact of Tokenization

Tokenized inventory collateral can deliver measurable improvements across the asset-based lending lifecycle, though actual timelines depend on warehouse integration maturity, inspection requirements, and bank control frameworks:

Faster settlement cycles: Substitution workflows can be reduced from multi-day manual processes to same-day or near-real-time approval cycles when warehouse integrations and inspection workflows are mature.

Reduced reconciliation effort: Automated pledge locks and real-time status updates eliminate manual ledger matching between bank systems and warehouse operators.

Lower fraud exposure windows: Cryptographic verification and hash-based deduplication close the time gaps where duplicate pledges or forged receipts could be exploited.

What Must Be Controlled in Inventory Collateral Systems

Before detailing the control architecture, banks must understand the three core control objectives that any inventory tokenization program must satisfy:

Physical-to-digital binding: The token must represent a specific, verified lot of goods at a specific location. Any disconnect between the token and the physical asset creates enforcement risk.

Pledge exclusivity: Once pledged, only the bank can authorize release, substitution, or transfer. The borrower cannot unilaterally move or cancel pledged inventory.

Legal enforceability: The control model must align with jurisdiction-specific perfection requirements. A token-level pledge lock without legal recognition provides operational convenience but no priority protection.

These three objectives form the foundation for the control model detailed below.

Why the Warehouse Is the Control Point - System & Operational Foundation

Banks lend against inventory because it has tangible value. The control problem is physical. The bank cannot hold the goods. It needs a legal mechanism to establish priority without taking possession.

The answer is warehouse receipts. The UNCITRAL-UNIDROIT Model Law recognizes both paper and electronic receipts as legal instruments. It provides that goods in storage can be collateral while they are stored in a warehouse. This legal framework is the basis for all tokenized inventory programs.

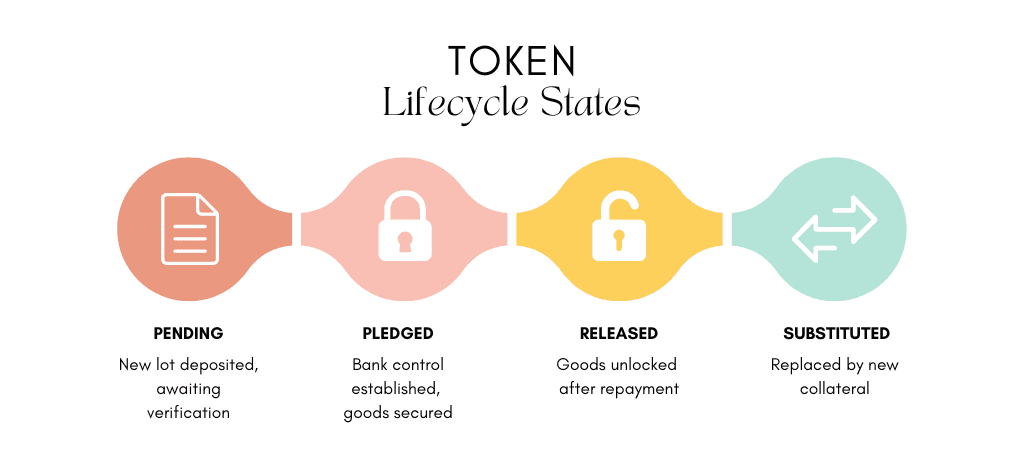

A tokenized warehouse receipt is a digital token that represents a specific lot of goods at a specific warehouse location. Every status change is logged automatically, giving the lender a real-time view of its control position.

Control Model: Three Mechanisms That Must Coexist - System Layer

Warehouse instruction authority. The bank becomes the party to whose directions the warehouse must conform. No goods can be released without authority of the bank. This must be in the warehouse agreement before any deposit takes place.

Token-level pledge lock. Once a receipt has been pledged, the token state becomes Pledged and the borrower will not be able to transfer or cancel it. Only the bank can authorize a status change. This sits at the system level, not just the contract level.

Tripartite agreement. The bank, borrower, and warehouse operator sign one agreement. It details each party's rights, establishes the bank's priority claim, and defines the conditions for release and substitution.

Without all three, the control position is incomplete. A contract without system-level enforcement is a weak control.

Collateral Substitution and Partial Release Logic - Operational Layer

This is the operational gap most inventory collateral guides skip entirely. Borrowers do not hold static inventory. They sell goods and replace them continuously. The bank has to manage this churn without losing priority or creating gaps in coverage.

Substitution workflow

The borrower wants to replace pledged grain lot A with grain lot B. The bank does not release lot A until lot B meets eligibility requirements. The substitution sequence runs as follows.

First, the borrower deposits lot B at the warehouse. The operator issues a new receipt. The bank verifies lot B for eligibility: right grade, right quantity, right location, right insurance. Then the bank approves lot B and registers its pledge. The token for lot B moves to Pledged. Third, the bank releases the pledge on lot A. The token for lot A moves to Released. The borrower can now access or sell lot A.

The critical control is sequencing. The new pledge must be confirmed before the old pledge is released. Any reversal of this order creates a window where the bank holds less collateral than the outstanding advance requires.

Partial release workflow

The borrower repays a part of the advance. The bank releases a part of the goods in proportion. The proportion is calculated at the current, not at the original, value of the collateral, which has been verified at that time. If prices have fallen since origination, a smaller quantity is released per unit of repayment.

Event | Token Action | Control Requirement |

New lot deposited | New token minted, status: Pending | Eligibility verification before pledge |

New lot approved | New token status: Pledged | Bank authorization recorded |

Old lot released | Old token status: Released | Only after new pledge confirmed |

Partial repayment | Proportional quantity released | Release quantity recalculated at current price |

Legal Perfection and Priority Against Competing Creditors - Legal Layer

Tokenization records a pledge. It does not automatically create legal priority. Priority is determined by the law of the jurisdiction where the goods are stored.

Three legal mechanisms interact in most markets.

Warehouse receipt possession. In jurisdictions that treat a warehouse receipt as a document of title, the holder of the receipt has priority over the goods. Transfer of the receipt transfers priority. The bank that holds or controls the receipt ranks ahead of unsecured creditors.

Registry filings. Under UCC Article 9 jurisdictions, the bank is required to file a financing statement to perfect its security interest in inventory. A tokenized pledge without the support of a UCC-1 filing may be subordinate to a creditor who files first. The same principle applies in jurisdictions with equivalent secured transaction registries.

Conflict between mechanisms. A bank that controls the tokenized receipt but has not filed in the public registry may face a priority challenge from a creditor who has filed. Conversely, a creditor who has filed but does not control the receipt may lose priority to the bank in a possession-based system.

Banks will need to check the priority regime in each jurisdiction before they accept inventory as collateral. Legal counsel must produce a jurisdiction matrix. It must map the receipt type, the required filing, and the priority rule for each location where goods are stored.

Jurisdiction Type | Primary Priority Mechanism | Required Bank Action |

Document of title systems | Receipt possession or control | Maintain registered control of token |

UCC Article 9 (US) | Financing statement filing | File UCC-1 before or at pledge |

Civil law registry systems | Registration in secured creditor registry | File in local registry at pledge |

Hybrid systems | Both possession and filing | Dual registration required |

Operational Exception Handling - Operational Layer

Exception handling extends the control model into real-world scenarios where standard workflows break down. Banks must build automated responses for four high-probability failure modes before go-live.

Failed inspection. The inspector finds that goods do not match the receipt description. Quantity is short or quality is below the stated grade. The bank immediately freezes the affected token, stops any pending funding against that receipt and notifies the borrower and requests an explanation within a defined window, usually 48 hours. If the shortfall is verified, the advance rate is recalculated. A margin call is issued for the difference.

Insurance lapse. The goods insurance policy expires or is cancelled. The monitoring system automatically detects the lapse. New advances against the affected receipts are suspended by the bank. The borrower is notified, with a cure period, typically 5 business days. If insurance is not reinstated in the cure period, the bank may declare a default event and commence enforcement.

Warehouse closure or operator failure. The warehouse operator becomes insolvent or the warehouse closes. The goods are still in store. The operator goes into insolvency and the ownership does not transfer. The bank steps in, under its right in the tripartite agreement. It appoints a new operator. The token record is updated to show acceptance by the new operator. No release can be made until the new operator confirms that the goods are intact and accounted for.

Disputed quantity. The borrower disputes the quantity on a receipt. The dispute is recorded as a pending exception. The token status is changed to Disputed. No release or substitution can be made until the dispute is resolved. An independent inspector is appointed. The resolution outcome is recorded in the audit log with a timestamp and a reference to the inspector's report.

Exception | Immediate Action | Resolution Trigger |

Failed inspection | Freeze token, suspend funding, notify borrower | Confirmed quantity or margin call met |

Insurance lapse | Suspend new advances, issue cure notice | Insurance reinstated within cure period |

Warehouse failure | Exercise step-in right, appoint replacement | Replacement operator confirms goods intact |

Disputed quantity | Move token to Disputed, block release | Independent inspection report accepted |

Portfolio-Level Risk Governance - Portfolio Layer

While individual collateral controls protect single positions, portfolio-level governance ensures the aggregate risk remains within bank policy limits. These controls operate across all pledged inventory regardless of location or operator.

Warehouse concentration limits. No single warehouse location should hold more than a defined share of the total pool. A reasonable starting limit is 20 to 25 percent per location. Concentration by operator should be tracked separately. An operator failure at one site must not impair more than a defined percentage of the portfolio.

Collateral aging thresholds. Inventory that has been pledged for longer than a defined period requires a mandatory re-inspection. The threshold depends on the asset class. Perishable goods may require re-inspection every 30 days. Durable commodities may allow 90-day cycles. Receipts past their re-inspection date are flagged and excluded from new advance calculations until inspection is complete.

Commodity price stress testing. The portfolio must be stress-tested against price decline scenarios. A 20 percent price drop in a key commodity class should not result in a margin deficit across more than a defined percentage of the book. Banks should run this test quarterly and after significant market moves.

Inventory turnover monitoring. High turnover commodities require more frequent substitution events. The monitoring system should track the substitution rate per borrower. An unusually low substitution rate may indicate that pledged inventory is not actually moving. This is a fraud signal worth investigating.

Bank Adoption Pathway: From Pilot to Portfolio

Banks should not attempt to tokenize their entire inventory book at once. A structured adoption pathway mitigates operational and legal risk:

Pilot Phase: Select a single commodity class, one trusted warehouse operator, and a single jurisdiction. Focus on validating the tripartite agreement, token-level pledge locks, and the substitution workflow in a controlled sandbox.

Scale Phase: Expand to multiple warehouse operators and commodity classes. Integrate the tokenization platform with the bank’s core lending system and implement automated portfolio concentration limits.

Portfolio Integration Phase: Expand interoperability across approved warehouse operators and jurisdictions. Implement advanced portfolio risk governance, including automated commodity price stress testing and dynamic aging thresholds.

Assess Tokenized Inventory Collateral Readiness With TokenMinds

Moving inventory collateral on-chain requires strict alignment between physical warehouse controls, digital pledge locks, and jurisdiction-specific legal perfection.

TokenMinds supports asset-based lending teams with three core deliverables:

Readiness assessment: Evaluate current warehouse operator integration, legal perfection gaps, and control model maturity.

Pilot design: Structure a controlled sandbox environment with defined success metrics and phase gates.

Integration mapping: Design the API flow between ERP systems, warehouse management platforms, and the tokenization layer.

Request a diagnostic review tailored to your bank's asset-based lending workflow. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: Can inventory be tokenized for collateral?

A: Yes. Inventory can be tokenized when each token is tied to a verified warehouse receipt, a specific lot of goods, lender-controlled pledge status, and jurisdiction-specific legal perfection.

Q: How do tokenized warehouse receipts support lending?

A: They give lenders a digital control record for pledged inventory. The bank can track receipt status, pledge locks, substitutions, partial releases, inspections, and exceptions through an auditable collateral record.

Q: What controls are needed for inventory-backed digital collateral?

A: Banks need physical verification, warehouse instruction authority, token-level pledge locks, tripartite agreements, insurance monitoring, legal perfection checks, and portfolio-level risk controls.

Q: How does the bank release partial inventory while keeping the loan in place?

A: The bank calculates the release quantity against the current verified collateral value, not the original advance amount. If prices have fallen, fewer goods are released per unit of repayment. The above described substitution workflow allows the borrower to substitute released goods with new inventory. The bank maintains coverage throughout.

Q: What happens when two creditors claim the same warehouse receipt?

A: Depends on the jurisdiction. In the document of title systems, the one who has control over the receipt wins. In filing systems, the one who registered first usually wins. Banks need to check the applicable rule in each jurisdiction. Dual registration (controlling the token and registering in the public registry) usually provides the most protection in most markets.

Q: Can a bank take inventory collateral across several warehouse locations?

A: Yes, with concentration controls. Each location is treated as a separate collateral position in the monitoring system. Concentration limits apply per location and per operator. The tripartite agreement must be executed separately for each location. A failure at one location must not trigger automatic default on positions at other locations.

References

UNCITRAL-UNIDROIT: Model Law on Warehouse Receipts. Recognizes electronic and paper warehouse receipts as legally valid instruments and confirms that stored goods may be used as collateral while held in a warehouse. https://uncitral.un.org/en/mlwr