TL;DR: Banks deploying stablecoin payment infrastructure often face a governance gap. Vendor documentation describes key management in crypto-native terms that do not map to bank control frameworks. This article translates wallet architecture into bank standard language: segregation of duties, approval matrices, transaction limits, audit trails, and emergency controls. Use it as a pre-production control checklist before vendor sign-off.

The Control Gap in Bank Crypto Payment Approvals

Most banks approaching stablecoin payments already operate mature control environments. They use transaction approval matrices. They have policies for segregation of duties and dual authorization requirements. Also, they document how to handle exceptions. The problem is not the absence of controls. The problem is translation.

Wallet vendors document their platforms in product terms. They describe key shards, signing nodes, and co-signers.

Risk committees and CISOs need to know:

Who approves a transaction.

Who can override it.

Who signs it.

What happens if there’s a problem.

The vocabulary mismatch causes stalled evaluations and delayed production approvals.

This gap is operational, not technical. To close it, map the wallet vendor abilities. Do this based on the control goals in the institution risk framework.

The sections below provide that mapping. They are written for the final stage of vendor evaluation, not for architects building from scratch. For the earlier design phase, see Bank-Grade Crypto Payments Architecture: A CTO's Blueprint | TokenMinds.

Translating Wallet Architecture into Bank Control Language

Multi-party computation (MPC) is the signing architecture used by enterprise custody platforms. In bank control language, MPC helps separate duties for authorizing transactions. No single party holds a complete private key. Signing requires coordinated participation from multiple independent key holders across separate environments.

This maps directly to dual custody requirements in traditional operations. A single operator cannot unilaterally move funds, just as a single teller cannot authorize a large wire without a second approver. The analogy holds at the control level. The risk committee should evaluate it that way.

Multisig is an older blockchain model. It achieves a similar goal but uses approvals at the protocol layer instead of the infrastructure layer. It is auditable on-chain but less flexible for enterprise workflows. Most bank grade deployments favor MPC for its configurability and off-chain governance options.

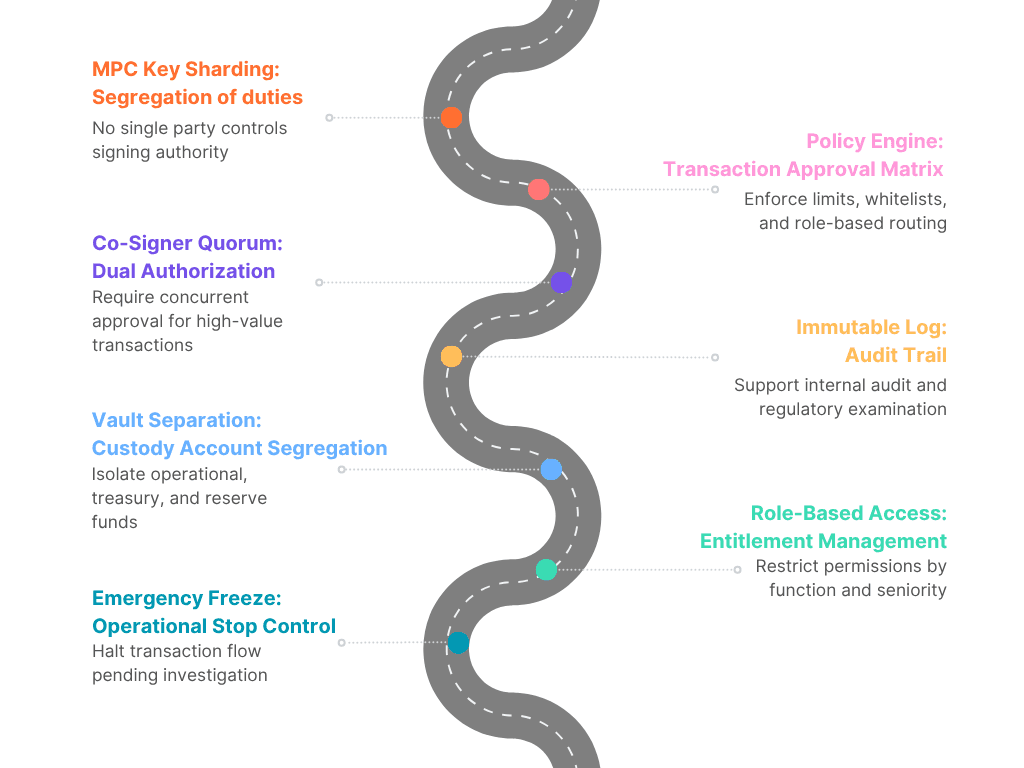

Wallet Architecture to Bank Control Mapping

The graphic maps seven wallet architecture components to bank control equivalents.

For compliance control architecture relevant to this evaluation, see Crypto Payment Compliance Checklist for Banks | TokenMinds.

Wallet Governance Model for Bank Crypto Payment Flows

A bank wallet governance model must define five control authorities.

Who owns the wallet environment. The institution retains ownership even when using a vendor platform.

Who controls signing authority. MPC key shards must remain under institutional control, not vendor control.

Who can change policies. Policy modifications require dual authorization from designated institutional approvers, not vendor staff.

Who can approve emergency actions. Emergency freeze or vault lock requires multi-person authorization from institutional risk officers.

How vendor access is restricted. Vendor support personnel may have read-only access for troubleshooting, but never signing authority or policy change rights.

These five authorities form the governance foundation. Fireblocks documents its governance controls as a distinct platform capability, explicitly separating vendor infrastructure from institutional control authority.

Policy Engine Design and Dual Approval Workflows

A policy engine is the rule layer above signing infrastructure. It decides if a transaction proceeds, who approves it, and when it is rejected.

Four control dimensions define a well-configured policy engine:

Dimension | Control Purpose | Example Rule |

Value tier | Limit transaction size by risk level | Block payments > $1M without CISO approval |

Counterparty | Enforce address whitelists | Reject sends to unverified destinations |

Time window | Restrict off-hours activity | Freeze large transactions outside 6 AM to 8 PM |

Role routing | Escalate complex payments | Route high-value payments to senior approvers |

Dual approval workflow at a glance:

Step | Actor | System Action | Control Outcome |

1 | Initiator | Submits payment request | Transaction intent recorded |

2 | Policy Engine | Evaluates rules | Auto reject or route for approval |

3 | Approver | Confirms with distinct credentials | Segregation of duties enforced |

4 | Signing Layer | Executes on-chain | Funds move only after dual sign-off |

5 | Audit Log | Records all events | Immutable evidence for audit |

Three questions for vendor sign-off:

Can policy rules be version controlled with full change history?

Do rule changes require their own dual authorization?

Are policy overrides logged with user, timestamp, and justification?

Fireblocks separates policy engine from signing layer, as detailed in its Fireblocks policy engine documentation. This supports independent control administration and rule updates without touching core cryptographic infrastructure.

Incident Response and Emergency Stop Mechanisms

Emergency stop controls are non-negotiable for any bank operating payment infrastructure. In traditional banking, these controls exist at the network level and the account level. In wallet infrastructure, they must exist at the vault-level and the policy level.

A compliant wallet platform should support at least three distinct emergency control states. A transaction freeze halts pending outbound transactions without requiring key destruction. A vault lock halts all signing activity for a specific vault. This keeps assets safe while an investigation is underway. A full operational suspension is the most severe state and should require multi-person authorization to activate and to lift.

Each state must generate an immutable event record. The log should capture who initiated the control, at what time, under what authorization, and when the control was lifted. This is the same documentation standard banks apply to any operational incident. Wallet vendors who cannot produce this log structure on request are not production ready for a regulated environment.

Incident Response Control Alignment

Incident response playbooks should map wallet control actions to existing operational risk procedures. The table below provides a framework for this alignment.

Incident Type | Wallet Control Action | Internal Risk Procedure |

Unauthorized transaction attempt | Policy engine rejection and alert | Operational risk incident log, compliance notification |

Suspected key compromise | Vault-level lock, initiate key rotation | CISO escalation, incident response team activation |

Abnormal transaction volume spike | Threshold triggered freeze | AML monitoring review, transaction reporting |

Unauthorized access to signing role | Access revocation, session termination | Identity and access management incident procedure |

Vendor system outage | Fallback signing path activation | Business continuity plan, operational escalation |

Regulatory inquiry | Audit log export, transaction history pull | Legal hold, regulatory affairs coordination |

Key rotation procedures deserve separate attention. MPC platforms rotate key material without moving funds, which avoids the operational risk of a full re-custody event. The evaluation should confirm that key rotation is automated, logged, and does not require downtime. It should also confirm that rotation events appear in the audit trail in a format the internal audit team can examine.

Evidence Banks Should Request From Wallet Vendors

Before production sign-off, banks must request concrete evidence from wallet vendors. Do not accept marketing claims. Demand documentation.

Policy rule export in machine-readable format. The bank must be able to review all active rules, version history, and change logs.

Approval workflow logs showing dual authorization in action. Export sample transactions with a full audit trail.

Sample audit trail covering at least 90 days of production or test activity. Verify immutability and export format compatibility.

Key rotation procedure documentation with step-by-step runbook. Confirm no downtime requirement and full logging.

Emergency freeze test record from the last 12 months. The vendor should have conducted and documented a controlled freeze and unfreeze exercise.

Access control matrix showing role definitions, permission levels, and segregation of duties.

SOC 2 Type II or ISO 27001 certification report.

Business continuity documentation including RTO, RPO, and failover testing results.

Fireblocks provides governance and security documentation at Fireblocks security and governance documentation. These eight evidence items form the minimum due diligence package for vendor evaluation.

Vendor Evaluation Scorecard for Governance Controls

At the final evaluation stage, check governance controls against the set pass and fail criteria. The checklist below is structured for a risk committee review, not a technical assessment. Assign ownership to the control domain leads identified in the brief before presenting findings.

Signing architecture: Does the platform use MPC across geographically separated nodes? Is no single node sufficient to sign independently? Pass requires yes to both.

Policy engine: Are transaction rules configurable by value, counterparty, time, and role? Are rule changes subject to their own authorization workflow? Pass requires yes to both.

Dual authorization: Does the platform enforce multi-person authorization at the software layer? Can the same user satisfy both initiator and approver roles? Pass requires yes to first, no to second.

Audit trail: Are all transaction events, policy changes, access events, and emergency control actions logged securely and permanently? Are logs exportable in a format compatible with the audit management system? Pass requires yes to both.

Emergency controls: Does the platform support tiered freeze and lock states? Are emergency control activations themselves subject to multi-person authorization? Pass requires yes to both.

Key management: Does the platform document key rotation procedures? Is rotation logged in the audit trail? Does rotation require downtime? Pass requires yes to first two, no to third.

Custody segregation: Can the platform enforce vault-level separation between operational, treasury, and reserve funds? Pass requires yes.

A vendor must show a passing response in all seven domains. If they can't, they aren't suitable for production deployment at a regulated institution. Partial compliance is a deferred risk, not an acceptable interim state.

TokenMinds reviews wallet governance controls before production launch. The review maps MPC, policy rules, approval workflows, audit logs, custody roles, and incident playbooks against the bank’s internal risk framework. Request a wallet governance control review at https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What is the difference between MPC and multisig for bank custody?

A: MPC distributes key material across independent nodes so that no single party holds a complete key. Signing requires coordinated computation across nodes. Multisig enforces multi-party approval at the blockchain protocol level. Both achieve a segregation of duties objective. MPC is often preferred for enterprise policy workflows in bank-grade deployments.

Q: How should a policy engine be evaluated in a bank risk context?

A: Evaluate it using the same methodology applied to any transaction approval matrix. Confirm that rules can be scoped by value, counterparty, time, and role. Confirm that rule changes require their own authorization. Confirm that all rule events are logged with user identity and timestamp. If the vendor cannot produce a rule change audit log, the control is not production grade.

Q: What audit trail requirements apply to wallet infrastructure at regulated banks?

A: The same requirements that apply to any core payment system. All transaction events, access changes, policy modifications, and emergency control activations must be logged immutably. Logs must include user identity, timestamp, and action type. They must be exportable for internal audit and regulatory examination. Retention periods should align with your existing records management policy.

References:

Fireblocks: Payments infrastructure for stablecoin transactions, including MPC, governance controls, policy engine, and enterprise-grade security capabilities. https://www.fireblocks.com/payments-solutions-revamp

Fireblocks: Policy Engine and governance controls product documentation. https://www.fireblocks.com/platforms/governance-and-policies

Fireblocks: Security platform documentation covering MPC architecture and defense in depth controls. https://www.fireblocks.com/platforms/security