Featured Answer: A bank-grade crypto payments architecture spans six layers. These include channel initiation, payment orchestration, wallet custody, compliance, liquidity, core banking, and reporting. The biggest failure point is not the blockchain. It is the gap between the compliance engine, FX timing, and core banking posting logic.

EXECUTIVE SUMMARY:

Most banks underestimate crypto payment integration. The channel API is simple. The real work happens in the middle layers. You must manage wallet governance, KYT placement, FX timing, idempotent ledger entries, and reconciliation. This article maps the full reference architecture. It shows what each layer owns and where complexity concentrates. CTOs and enterprise architects can use this to plan vendor and internal design conversations.

Why Crypto Payments Cost More Than You Think

Banks often scope only the channel layer. They assess a vendor API and assume the build is straightforward. Then complexity appears three layers down. A stablecoin payment must become a general ledger entry. This is an architecture problem, not a vendor problem.

Ripple now processes over $100 billion in payment volume. Fireblocks secures more than $10 trillion in digital asset transactions. The tools exist. Internal integration work remains the main hurdle. A reference architecture surfaces the right questions early.

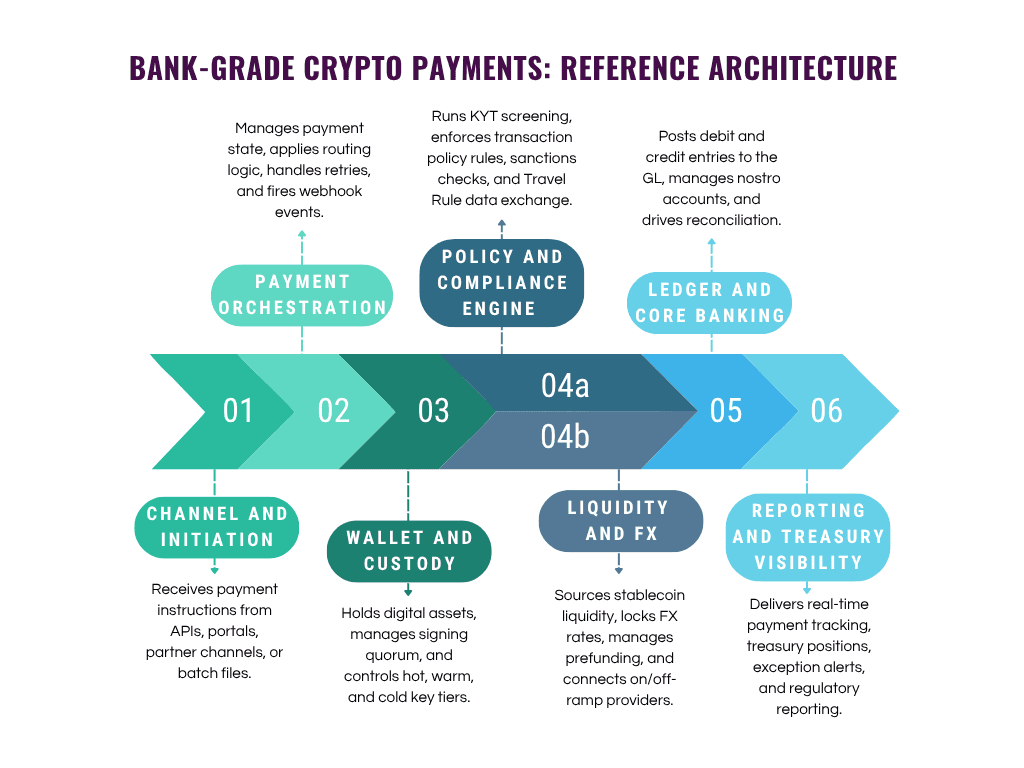

The Architecture at a Glance

A production stack runs across six layers. Compliance and liquidity operate in parallel. They must finish before a payment proceeds, but they touch different systems and run on different timelines.

*Architecture diagram: Six-layer reference stack from channel initiation to treasury reporting. KYT placement and core banking adapters drive most complexity.

Four Pre-Build Decisions Every Architect Must Lock Before Integration

Lock these choices before you map technical requirements. They set control boundaries for every downstream layer.

1. Custody Model Selection

Choose MPC, third-party custody, or hybrid. This sets your liability perimeter. MPC allows bank-controlled key shares and signing policy, depending on deployment model. Third-party custody offloads management but requires strict SLAs and audit rights.

2. KYT Placement Strategy

Run analytics pre-signing or post-signing. Pre-signing blocks risky transactions before broadcast. Post-signing increases throughput but forces manual remediation if a flagged payment leaves the wallet.

3. FX Execution Model

Use prefunded liquidity or on-demand conversion. Prefunding removes FX latency but adds inventory management. On-demand conversion requires sub-second rate locks and reliable provider uptime.

4. Core Banking Integration Pattern

Choose real-time event streams or batch reconciliation. Real-time streams need idempotent API design to handle duplicate webhooks. Batch processing aligns with traditional cycles but delays ledger updates.

Cross-Layer Dependency Model

Latency in one layer impacts the next. Architects must map these chains.

KYT delays can expire FX locks. The system must re-quote or trigger fallback routing.

FX delays push fiat credits past same-day posting windows. This creates reconciliation breaks.

Wallet congestion exhausts corridor liquidity. Treasury teams receive automated alerts to rebalance hot wallets.

Where the Build Complexity Actually Lives

Not every layer demands equal effort. Three integration points consistently cause scope creep or post-launch failures.

KYT node placement

Analytics must run between orchestration and signing. Slow KYT adds payment latency. Teams often miss this constraint until UAT.

FX timing and prefunding

Locking rates requires prefunding or credit lines. Buffer sizes vary by corridor. Poor planning causes FX losses or failed settlements.

Core banking integration

This bridges on-chain state and internal ledgers. Webhook retries can cause duplicate posts. Idempotent design prevents double entries. Banks own this integration.

Failure Modes and Recovery Paths

Architects must design for failure, not just happy-path flows.

Failure State | Detection Mechanism | Recovery Path | Owner |

KYT Timeout | Analytics provider alert | Queue transaction for manual review; hold signing; alert fraud ops. | Compliance / Orchestration |

Liquidity Unavailable | Heartbeat failure / API timeout | Route to secondary provider; trigger fallback FX logic. | Treasury / Orchestration |

On-Chain Congestion | Block delay exceeds SLA | Extend quote validity; notify user; rebalance fees. | Infrastructure / Wallet |

Duplicate Webhook | Idempotency key mismatch | Reject duplicate GL post; log event; return 200 OK. | Core Banking Adapter |

Operational Scenario: LATAM Payout

Consider a $5M USDC payout to a LATAM corridor.

Treasury instructs the payment.

KYT clears in 2 seconds. Address is clean.

FX provider locks a rate for 30 seconds.

MPC wallet signs in 0.8 seconds.

Chain confirms in 12 seconds.

Off-ramp credits the local bank.

Real-time stream posts to the core ledger.

Total time stays under 15 seconds. The FX risk window remains minimal. If KYT exceeds 30 seconds, the system triggers a re-quote or fallback route.

Layer by Layer: What Each Component Owns

The table maps functional ownership, integration points, and complexity hotspots. The final column highlights required architect decisions.

Layer | What it owns | Key integration points | Where complexity concentrates |

1. Channel and Initiation | Receives payment instruction via API, portal, partner channel, or batch file | API gateway authentication, rate limiting, input validation, idempotency key assignment | Low. Standard API design. Complexity rises if batch file formats vary by corridor. |

2. Payment Orchestration | Routes the payment, manages state, handles retries and failures, fires events | Quote engine integration, routing rules, webhook delivery, failure taxonomy | Medium. State machine design across async flows is where most build teams underestimate effort. |

3. Wallet and Custody | Holds and moves digital assets; manages signing quorum and key lifecycle | MPC key share distribution, hot/cold tier logic, wallet segregation per client or flow type | High. Custody model determines what is possible downstream. Decisions made here are hard to reverse. |

4a. Policy and Compliance Engine | Enforces transaction policy rules, screens addresses, runs KYT, handles Travel Rule data | KYT node placement relative to signing, sanctions list update frequency, IVMS 101 counterparty data exchange | High. KYT placement is the most consequential architectural decision in this layer. See Section 2. |

4b. Liquidity and FX | Sources stablecoin liquidity, converts currencies, manages prefunding and settlement timing | FX rate lock timing, prefunding buffer sizing per corridor, on/off-ramp provider SLAs | Medium to high. Corridor-by-corridor variance in settlement windows creates operational unpredictability. |

5. Ledger and Core Banking | Posts debit and credit entries to the GL, manages nostro and vostro accounts, drives reconciliation | Core banking API adapter design, idempotent write guarantees, reconciliation logic between on-chain state and GL | Very high. This is the layer the bank always owns. Adapter complexity varies significantly by core banking system. |

6. Reporting and Treasury | Provides real-time payment tracking, treasury position visibility, exception alerts, and regulatory reporting | Data pipeline from on-chain events to reporting layer, latency requirements, regulatory report format | Low to medium. Often delivered via vendor dashboard initially; custom reporting adds complexity later. |

How Stablecoin Payment APIs Connect to Core Banking

The adapter layer is the critical bridge between on-chain payment events and the bank's system of record. It translates blockchain-native data (transaction hashes, block confirmations, wallet addresses) into the bank's canonical payment event model and GL posting instructions.

Reference event flow:

Payment initiated → KYT cleared → wallet signs → on-chain confirmation → orchestration event → GL posting → reconciliation → exception handling.

Key design patterns:

Idempotency keys: Every payment instruction carries a unique idempotency key. If a webhook retry delivers the same confirmation twice, the adapter recognizes the duplicate and prevents a second GL post.

Canonical event model: The adapter maps vendor-specific event schemas into a bank-standard payment status taxonomy: `initiated` `kyc_cleared` `signed` `on_chain_confirmed` `gl_posted` `reconciled` `exception`.

GL posting logic: On-chain finality triggers a debit to the bank's stablecoin custody account and a credit to the beneficiary's account (or nostro/vostro for cross-border). Posting occurs on the same business day as confirmation, with weekend/holiday logic defined upfront.

Reconciliation: Daily reconciliation matches on-chain transaction hashes to internal payment references and GL entries. Exceptions (mismatches, missing confirmations, failed posts) route to a documented escalation path.

Webhook retry logic: The adapter implements exponential backoff for failed webhook deliveries, with a dead-letter queue for events that exceed retry thresholds.

The table below summarizes integration decision ownership:

Integration decision | Bank-owned? | Vendor-supported? | Design risk |

KYT before signing | Yes | Usually | Latency and false positives |

Wallet signing policy | Shared | Yes | Governance and key-control model |

FX rate lock timing | Shared | Yes | Prefunding and corridor exposure |

GL posting logic | Yes | Partly | Duplicate posting / reconciliation failure |

Failure playbook | Yes | Partly | Operational continuity |

*This table is a starting point for vendor RFPs and internal architecture reviews.

Vendor Coverage vs. What the Bank Still Owns

Vendors cover substantial ground. Coverage does not equal ownership.

Banks always retain compliance sign-off. Humans must review KYT flags. The core banking adapter remains bank-owned. Reconciliation logic maps on-chain states to ledger entries. Banks must write and test the failure playbook before go-live.

For the full vendor category taxonomy that informs layer selection, see Crypto Payment Integration for Banks: Vendor Landscape & Decision Framework. For the operational workflow that feeds into this architecture, see Stablecoin Payout Integration for Bank Cross-Border Payments. For the security controls and wallet governance framework that protects this architecture, see Wallet Security Controls for Bank Crypto Payment Flows.

The architecture is not the hard part. Sequencing is. Get custody right before compliance. Get compliance right before core banking. Document failure paths before production. This reference model starts the conversation. It does not replace it.

Planning a bank-grade crypto payments build?

TokenMinds can help your team map wallet infrastructure, custody controls, KYT placement, liquidity/FX sequencing, core banking adapters, and reconciliation requirements before scope is locked.

Request an architecture blueprint workshop.

Frequently Asked Questions:

Q: How do stablecoin payment APIs connect to core banking systems?

They connect through an adapter layer. The adapter translates on-chain events into GL posting instructions. It must handle idempotent writes, map payment states to internal taxonomies, and reconcile balances against ledger entries. Banks own this work. It usually drives the longest build timeline.

Q: Where does KYT fit in a bank crypto payments architecture?

KYT sits between the payment orchestrator and the wallet signing node. Analytics must screen addresses before broadcast. Post-broadcast screening creates compliance gaps. Most vendors support pre-signing KYT. Banks must ensure the KYT node stays fast enough to avoid payment delays.

Q: What does a bank still own when using a full-stack vendor?

Four items remain bank-owned. You keep compliance sign-off authority. You design the core banking adapter. You build reconciliation logic. You write the failure and exception playbook. Vendors provide tooling and dashboards. They cannot own internal decision processes or assume regulatory accountability.

References:

Ripple: Ripple Redefines Payments with End-to-End Stablecoin Platform and Global Customer Momentum (March 3, 2026). Source for $100B+ processed volume, full-stack platform expansion including managed custody, virtual accounts, and fiat/stablecoin settlement coverage. https://ripple.com/ripple-press/ripple-redefines-payments-with-end-to-end-stablecoin-platform-and-global-customer-momentum/

Ripple: Cross-Border Stablecoin Payments. Source for unified collect/hold/exchange/payout platform framing and institutional use cases. https://ripple.com/solutions/cross-border-payments/

Fireblocks: Payments Solutions Revamp. Source for stablecoin orchestration, fiat/crypto accounts, on/off-ramps, compliance, and secure operations. https://www.fireblocks.com/payments-solutions-revamp

Fireblocks: Powering the Next Era of Digital Value (May 2025). Source for $10T+ in secured digital asset transactions, policy engine and wallet tagging product, and programmable infrastructure layer framing. https://www.fireblocks.com/blog/fireblocks-security-innovations-digital-asset-infrastructure

DXC Technology: DXC Partners with Ripple to Empower Global Banks with Scalable Digital Asset Custody and Payments (January 21, 2026). Source for core banking integration framing: programmable payments, tokenization, and custody bridging legacy systems with on-chain finance without disrupting mission-critical core banking. https://dxc.com/newsroom/01212026-dxc-partners-with-ripple-to-empower-global-banks-with-scalable-digital-asset-custody-and-payments

PYMNTS: AMINA Bank Integrates Ripple Payments to Facilitate Cross-Border Stablecoin Transactions (December 2025). Source for practitioner framing of the fiat-blockchain rail integration challenge from a regulated bank perspective. https://www.pymnts.com/cryptocurrency/2025/amina-bank-integrates-ripple-payments-to-facilitate-cross-border-stablecoin-transactions/

Federal Reserve FEDS Note: Payment Stablecoins and Cross-Border Payments (March 30, 2026). Source for framing of cross-border payment friction and the structural case for stablecoin rails in institutional payments. https://www.federalreserve.gov/econres/notes/feds-notes/payment-stablecoins-and-cross-border-payments-benefits-and-implications-for-monetary-policy-20260330.html