EXECUTIVE SUMMARY:

Stablecoin payments are no longer a proof of concept — they now move $200 billion every month on the Fireblocks Network alone. Banks that want to participate are discovering the same obstacle: the vendor market is fragmented, the categories overlap, and picking the wrong layer first is expensive to unwind. This article maps the seven vendor categories every bank must evaluate, identifies where integration risk actually sits, and offers a practical decision framework for institutions ready to move from strategy to execution.

The Integration Problem Is Already Here

The question has shifted. Banks are no longer asking whether stablecoin payments deserve serious attention. The debate now is about execution. Specifically, how to build the right infrastructure stack without creating new operational risk in the process.

The vendor market has not made this easy. Dozens of providers have entered the space. Each solves a different piece of the puzzle: some handle the movement of value, others manage compliance, others focus on custody, liquidity, or merchant-side acceptance. Few providers cover the full stack without introducing integration seams. And yet banks are routinely sold a single-vendor narrative that obscures how complex the actual integration challenge is.

Financial institutions enabling stablecoin payments are running into the same core problems. High integration complexity. Fragmented liquidity. Inconsistent compliance frameworks that create regulatory exposure and operational chaos. Before any vendor evaluation begins, banks need a clear map of the infrastructure layers involved.

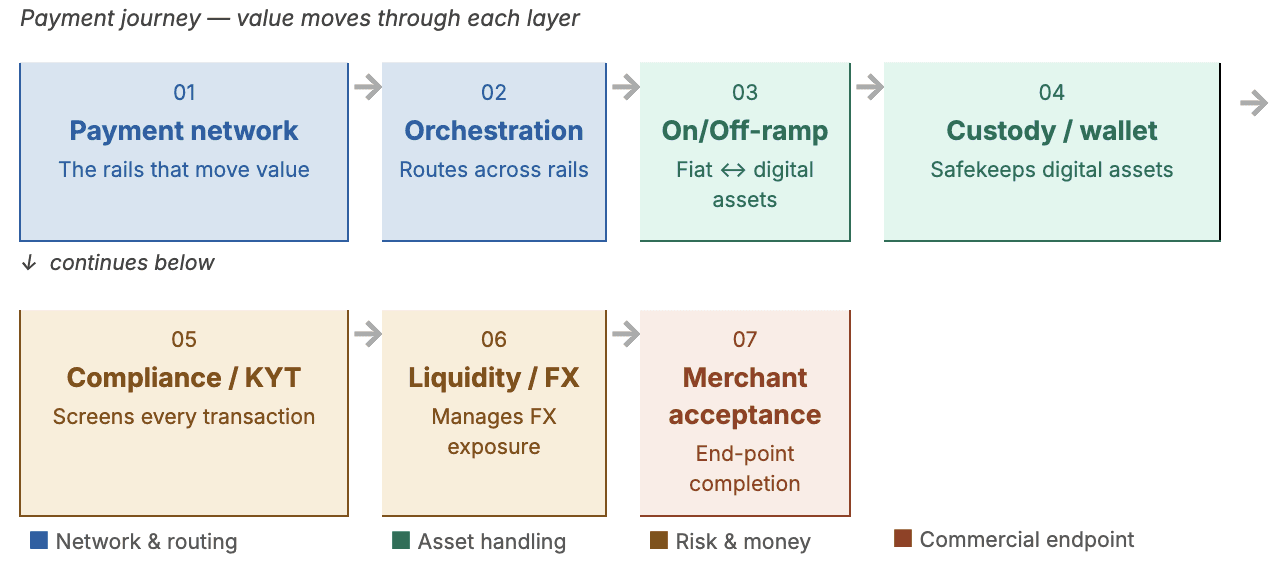

Seven Categories. One Stack.

Crypto payment integration is not a single purchase. It is an architecture decision involving up to seven distinct vendor categories, each with its own risk profile, regulatory implication, and operational dependency. Getting the map right before choosing vendors is what separates institutions that build scalable infrastructure from those that face expensive rework later.

Vendor Landscape by Layer

This is not a ranking of vendors. It is a map of the vendor categories banks need to evaluate before building a shortlist.

Layer | What the bank is buying | Representative vendor type | Key diligence questions | Integration risk |

Payment network | Counterparty reach and settlement rails | Stablecoin payment network | Which corridors, currencies, counterparties, and settlement assets are supported? | Medium |

Orchestration | Routing and provider coordination | Payment orchestration / connectivity layer | Can it route across multiple rails, ramps, and liquidity sources? | High |

On/off-ramp | Fiat-to-stablecoin conversion | Institutional ramp / payout partner | What licenses, jurisdictions, spreads, and settlement SLAs apply? | High |

Custody/wallet | Asset control and wallet operations | Bank-grade custody / wallet infrastructure | How are keys, approvals, segregation, and controls handled? | High |

Compliance/KYT | Transaction monitoring and regulatory controls | KYT / travel-rule / sanctions vendor | Is compliance native, integrated, or bolted on? | Very high |

Liquidity/FX | Conversion and market access | FX / liquidity provider | Who provides liquidity, at what spread, and under what counterparty exposure? | High |

Merchant acceptance | End-user or merchant-side completion | Crypto merchant acceptance / acquiring layer | How are refunds, reconciliation, reporting, and settlement handled? | Medium-high |

1. Payment Network

The foundational rails that move value between counterparties. This is where stablecoin transactions actually travel. The key evaluation criterion is network reach: how many corridors, currencies, and counterparties are accessible from a single connection. Circle Payments Network, for instance, is a network for banks, PSPs, VASPs, and enterprises that enables 24/7 stablecoin-based settlement between participating financial institutions, with Circle Technology Services acting as the network operator and technology service provider. Its public materials emphasize compliance-first architecture, partner vetting, single-API expansion, and one-to-many global integration. Settlement currently uses USDC and EURC across Ethereum, Polygon, Solana, and EVM-compatible chains.

2. Orchestration Layer

The middleware that coordinates payment flows across multiple rails, providers, and blockchains. Routing decisions happen here; which rail to use, which liquidity source to tap, how to handle exceptions. Without a strong orchestration layer, banks manage point-to-point connections manually. That scales poorly and breaks under volume.

Fireblocks built its Network for Payments specifically to address this. The goal is to let institutions orchestrate global payment flows; cross-border treasury, payouts, remittance, and merchant settlements with complete control across fiat and blockchain rails from a single integration point.

3. On/Off-Ramp

Converting between fiat and digital assets at institutional grade. On/off-ramp quality varies significantly. Spread, settlement speed, counterparty creditworthiness, and jurisdiction coverage are all critical variables. Banks need ramp providers who can handle institutional volume reliably, not just retail conversion at scale.

4. Custody or Wallet Layer

Institutional-grade safekeeping of digital assets. For banks, this cannot be afterthought infrastructure. The custody layer determines how private keys are managed, how assets are segregated, and how operational workflows are controlled. Regulatory expectations around digital asset custody are tightening in most jurisdictions. Vendor selection here is as much a compliance decision as a technical one.

5. Compliance / KYT

Know Your Transaction monitoring for every payment in the stack. Non-negotiable for any regulated institution. The Fireblocks Network embeds compliance directly into the transaction layer — handling AML/KYT checks, sanctions screening, beneficiary data verification, and travel-rule requirements across jurisdictions. Banks should evaluate whether compliance is native to the platform or bolted on as a third-party integration. Native or tightly integrated compliance is easier to govern. Bolted-on controls can work, but banks should diligence the audit trail, data handoff, exception workflow, and accountability model carefully.

See KYT Frameworks for Institutional Stablecoin Flows.

6. Liquidity / FX

Managing cross-currency exposure and settlement liquidity in real time. Stablecoin payments that cross currency boundaries require FX conversion somewhere in the chain. The question is where, at what cost, and with which counterparty. Banks with existing FX desks will want to understand how a crypto payments stack interfaces with their current liquidity management. Those without that capability need a vendor who provides it reliably.

7. Merchant Acceptance

Enabling end-point acceptance of crypto payments at scale. For banks serving merchant clients, this layer determines whether stablecoin payment flows can actually complete at the point of commerce. Merchant acceptance infrastructure needs to handle reconciliation, refunds, currency conversion, and reporting — all integrating cleanly with existing merchant acquiring systems.

Where Integration Actually Breaks Down

Few providers credibly cover all seven categories without introducing integration seams. In many bank implementations, the practical question is not whether to use one provider or many, but which layers should be owned internally, which should be vendor-provided, and where handoffs need explicit controls. The real integration risk is not within any single layer — it is at the seams between layers, where data standards diverge, compliance logic conflicts, and operational processes fail to connect.

Circle Payments Network addresses part of this through a one-to-many model: a single API and agreement that unlocks global fiat payouts without requiring bilateral arrangements with each local partner. This reduces integration overhead at the network layer significantly. It does not, however, eliminate the need for careful architecture across the full stack.

Common seam failures:

Compliance-data mismatch: KYT flags a transaction but settlement proceeds anyway.

Settlement-status mismatch: One layer reports “final” while another still shows “pending”.

Reconciliation gaps: Transaction metadata lost between orchestration and accounting systems.

Liquidity failure: FX provider cannot source currency at quoted spread under volume.

Refund handling: Merchant acceptance layer cannot reverse a settled stablecoin payment.

Travel-rule handoff: Beneficiary data format incompatible between sending and receiving jurisdictions.

The practical implication is straightforward. Banks that treat crypto payment integration as a single vendor selection increase the risk of costly rework as volumes, corridors, counterparties, and compliance obligations expand. Banks that approach it as an architecture exercise — mapping all seven categories first, understanding where gaps exist, choosing vendors deliberately — build something that actually scales.

Decision Framework: Vendor Shortlisting Criteria

The four executive filters below help narrow the field. For procurement-grade evaluation, layer in this scorecard:

Criterion | Why It Matters | Red Flag |

Licensing & jurisdictional coverage | Determines where the vendor can legally operate and which counterparties they can serve | Vague on regulatory status; no public licensing disclosures |

Sanctions, AML/KYT, travel-rule controls | Non-negotiable for regulated institutions; gaps create enforcement risk | Compliance is "partner-integrated" with no native audit trail |

API maturity & implementation burden | Affects time-to-value and ongoing maintenance cost | No sandbox, limited documentation, or custom integration required for basic flows |

Supported chains, assets, fiat currencies, corridors | Defines the operational scope of your payment flows | Narrow asset support that forces workarounds for common use cases |

Settlement finality & reconciliation model | Impacts accounting, reporting, and dispute resolution | Unclear settlement status semantics or manual reconciliation required |

Liquidity depth & FX spread transparency | Affects total cost of ownership and pricing predictability | Opaque pricing; spreads widen materially under volume |

Custody/key-management model | Core to operational security and regulatory compliance | Keys held by vendor without segregation or bank-controlled approvals |

Data lineage, audit logs, reporting | Required for internal controls and external audit | Logs are incomplete, non-exportable, or lack timestamp granularity |

SLAs, uptime, incident response, business continuity | Operational resilience under production load | No public uptime history; incident communication process undefined |

Exit plan, vendor lock-in, portability | Protects against stranded infrastructure | Data or configuration cannot be exported; migration path undocumented |

Four Questions Before You Select Any Vendor

Which layer is your actual gap?

Start with an honest assessment of what you already have. Banks with strong FX infrastructure and existing custody arrangements face different gaps than those starting from scratch. Don't pay for layers you already own.

What is your regulatory perimeter?

Jurisdiction determines which compliance vendors are viable, which blockchains are permissible, and what licensing your counterparties must hold. Circle Payments Network requires all participants to meet eligibility requirements tailored to each jurisdiction's oversight, and apply that same standard to every vendor in your stack.

What is your counterparty profile?

Wholesale institutional flows and retail consumer payments require different on/off-ramp and liquidity infrastructure. Define your primary use case before evaluating vendors, not after.

What is your build vs. buy tolerance?

Some layers can be built internally by banks with large engineering teams. Most cannot, and should not be. The total cost of ownership for a custom build typically exceeds vendor cost within two years.

Market Direction and Regulatory Durability

Vendor consolidation is coming. The seven-layer map described here will compress as larger players acquire specialists and build broader stacks. Recent moves in the market signal this clearly, infrastructure providers are expanding from narrow functions toward more complete operating layers for digital assets.

Regulatory clarity will reshape the compliance layer. In the EU, MiCA’s rules for asset-referenced tokens and e-money tokens (Titles III and IV) raise the bar for issuance, authorization, reserve management, and supervision. In the U.S., the GENIUS Act establishes a federal framework for payment stablecoin issuers, with implementation continuing through rulemaking by the relevant federal banking regulators. Banks making vendor selections now should weight regulatory durability as a criterion, not just current functionality. See Regulatory Durability as a Vendor Selection Criterion.

Infrastructure readiness varies by layer. Core infrastructure layers such as custody, compliance, and payment networks are mature enough to build on today. Merchant acceptance and cross-border FX liquidity are still developing in several corridors. Build with modularity in mind. Choose vendors at the mature layers while preserving flexibility at the edges.

Getting the Architecture Right First

The stablecoin payments market is not waiting. More than 300 payment companies are already live on the Fireblocks Network, processing over $200 billion in stablecoin payments monthly. The institutions moving fastest are not necessarily those with the largest budgets. They are the ones who mapped the problem correctly before selecting vendors.

The seven-category framework here is a starting point, not a checklist. Every institution's stack will look different depending on existing infrastructure, regulatory geography, and client profile. What matters is knowing which layers you need, which you already have, and where the real integration risk sits before signing any contracts.

The architecture question isn't which vendors exist. It's which layers your institution must own, which it can integrate, and where integration risk concentrates.

Ready to evaluate providers? The Crypto Payments Vendor Landscape Briefing breaks down the seven categories by integration risk, regulatory perimeter, and total cost of ownership – so you can shortlist vendors before committing to architecture.

Frequently Asked Questions

Q: What crypto payment integration vendors should banks evaluate?

Banks should evaluate vendors across seven infrastructure layers: payment network, orchestration, on/off-ramp, custody or wallet infrastructure, compliance/KYT, liquidity/FX, and merchant acceptance. The right shortlist depends on the bank's target use case, regulatory perimeter, existing custody and FX capabilities, and tolerance for build-versus-buy complexity.

Q: How should a bank choose a stablecoin payment infrastructure provider?

A bank should start by identifying which layer of the stack it actually needs to fill. From there, it should evaluate vendors on licensing, corridor coverage, settlement model, API maturity, compliance controls, custody model, liquidity access, operational resilience, and integration risk. The vendor scorecard above provides a procurement-grade framework.

Q: What is the difference between a crypto payment network and an orchestration layer?

A payment network provides the rails and counterparties through which value moves (e.g., Circle Payments Network). An orchestration layer coordinates routing across rails, providers, blockchains, liquidity sources, and exception workflows (e.g., Fireblocks Network for Payments). Some providers may combine elements of both, but banks should evaluate the functions separately to avoid integration gaps.

References:

Fireblocks — The Fireblocks Network for Payments (September 2025)

https://www.fireblocks.com/blog/the-fireblocks-network-for-payments-is-here

Circle — Circle Payments Network (CPN) Overview