TL;DR

Tokenizing a receivable does not make it eligible collateral. The token only reflects the quality of the data behind it. Banks must verify invoice authenticity, debtor confirmation, delivery evidence, payment terms, debtor risk, assignment restrictions, duplicate financing risk, and repayment history before tokenization. This article provides a bank-ready checklist and example metadata schema for receivables collateral workflows.

Why Verification Comes Before Tokenization

Most operational failures in receivables financing start before any funding decision. A bank that tokenizes an unverified invoice has not reduced risk. It has recorded bad data on a ledger.

Before tokenization, banks must verify invoice authenticity, debtor credit risk, and debtor relationship confirmation. The technology does not perform these checks automatically. The bank must build the verification layer into its workflow before the token is minted.

The eight areas below define what that layer looks like in practice.

Bank-Ready Receivables Verification Checklist

Verification Area | Bank Must Confirm | Decision Impact |

Invoice authenticity | Source system, signature, audit trail | Hard stop if unverifiable |

Debtor acceptance | Written debtor confirmation | Hard stop if not confirmed |

Goods or services completion | Delivery or service evidence | Hard stop if disputed |

Payment terms | Due date, currency, set-off rights | Adjust eligibility |

Debtor credit risk | Rating, payment behavior, sector risk | Adjust advance rate |

Assignment restrictions | Assignability and legal perfection | Hard stop if blocked |

Duplicate financing | Registry or internal deduplication check | Hard stop if duplicate |

Repayment history | Late payments, disputes, defaults | Adjust advance rate |

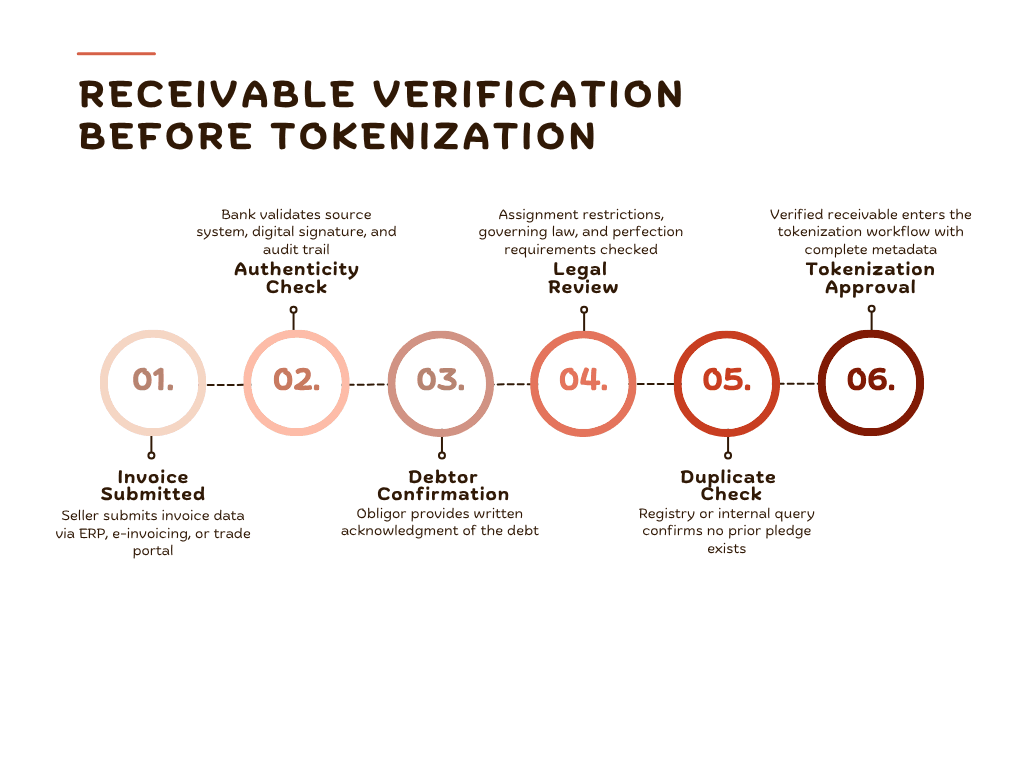

Where Verification Fits in the Tokenization Workflow

The verification process follows a clear sequence before any receivable enters the tokenization workflow:

Seller submits invoice data.

Bank validates authenticity.

Debtor confirms the obligation.

Legal team reviews assignment rights.

Bank checks duplicate financing risk.

Approved receivable enters tokenization.

This flow validates each receivable before tokenization. The detailed verification criteria for each step are defined in the checklist below.

The Eight-Point Verification Checklist

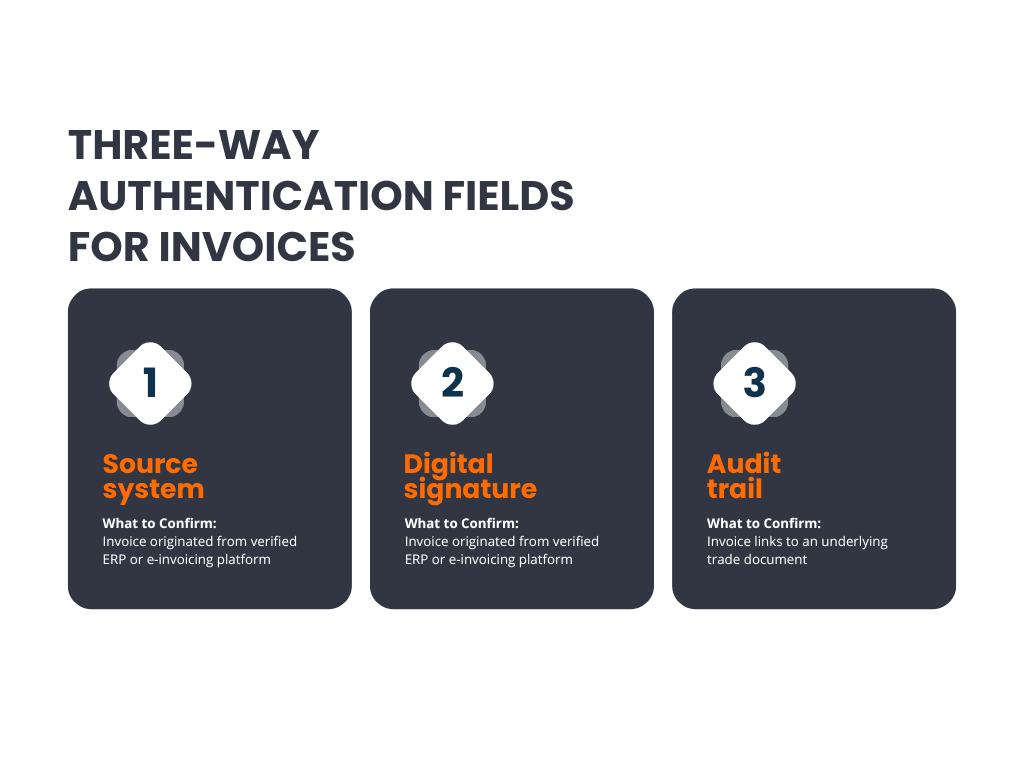

1. Invoice Authenticity

The first check confirms a real transaction. Banks verify the source system, authentication, and audit trail.

Invoice fraud is more likely to happen with invoices that are not generated by a validated ERP or e-invoicing system. A digital signature of the issuing entity is proof that the document has not been tampered with. The audit trail should link the invoice with a purchase order, delivery record or service confirmation.

2. Debtor Acceptance and Confirmation

An invoice is a claim. It is not a confirmed obligation until the debtor acknowledges it. Banks must obtain documented debtor confirmation before treating the receivable as eligible collateral.

Confirmation formats vary. The debtor may also sign a notice of assignment, confirm through a secured portal or give an irrevocable payment instruction to the lender. The format matters less than the output: a written, traceable record that the debtor accepts the debt and its terms.

This step also functions as an early fraud screen. A debtor who does not recognize the invoice signals a problem before any funds are advanced.

Read How ERP, E-Invoicing, and Debtor Confirmation Feed Tokenized Receivables Collateral for a detailed look at how these confirmation workflows connect to tokenization infrastructure.

3. Goods or Services Completion Evidence

Invoice payment usually depends on completed delivery. If the bank advances funds on an invoice prior to delivery of the goods or completion of services, the bank has a claim that the debtor can properly contest.

The bank should verify supporting trade documents here. Evidence can be a signed delivery receipt, bill of lading, warehouse receipt or a certificate of service completion. The document must be traceable, dated and match the invoice information.

4. Payment Terms, Due Date, and Currency Validation

The actual amount that the bank is financing corresponds to the invoice terms. Before tokenization, banks validate maturity, currency, discounts, penalties, and set-off rights.

Field | Validation Requirement |

Due date | Confirmed and within eligible maturity window |

Currency | Matches bank collateral policy and FX exposure limits |

Payment terms | No undisclosed offset rights or contra arrangements |

Early payment clauses | Identified and factored into advance rate calculation |

Currency mismatches can create hidden exposure at origination. Checking this field explicitly prevents downstream problems when the receivable matures.

5. Debtor Credit Risk Assessment

The quality of the receivable depends on the ability of the debtor to pay. Banks must run a credit assessment on the obligor before accepting the invoice as collateral, not after.

Inputs for this assessment include internal credit scores or ratings, external agency ratings where available, payment behavior data from trade references, and any sector-level concentration flags. A debtor with deteriorating credit reduces the eligible collateral value of every invoice in their name.

The credit assessment result should be recorded as part of the token metadata so that changes in debtor standing can trigger eligibility reviews during the monitoring phase.

6. Assignment Restrictions and Legal Enforceability

Not all receivables are legally assignable to a lender. Some contracts contain anti-assignment clauses that prohibit the seller from assigning the invoice without the consent of the buyer. Others are governed by laws that require certain formalities in the assignment.

Before tokenization, the bank must confirm that the receivable is legally assignable, that no contractual restriction blocks the pledge, and that the assignment can be perfected under the governing law of the contract.

This step is often skipped in early-stage tokenization programs. Skipping it does not eliminate the legal risk. It defers it to the point when enforcement matters most.

7. Duplicate Financing Prevention Controls

Duplicate financing occurs when the same invoice is pledged to more than one lender. It is one of the most common forms of trade finance fraud and one of the hardest to detect without a shared registry.

Before accepting an invoice, the bank must check whether it has already been tokenized, assigned, or pledged on any other platform or with any other lender. Where a central invoice registry exists, this check is a query. Where it does not, the bank must maintain its own deduplication database and cross-reference incoming invoices against it.

The token alone does not prevent duplication. A registry does.

Check Tokenized Invoice Data Model 2026: Fields Banks Need Before Collateral Approval for identifying the required data fields before collateral approval.

8. Repayment History and Performance Data

A receivable from a debtor with a good repayment history is less likely to default than a receivable from a new or inconsistent obligor. Banks should collect and review repayment history before bringing invoices into a tokenized collateral program.

The relevant data points include average days to pay on past invoices, any history of late payment or dispute, and whether the debtor has defaulted on obligations to the same seller or other creditors before.

This data feeds directly into advance rate decisions and portfolio concentration limits. It should be captured as structured metadata, not as a qualitative note.

Example Field Schema for Bank-Ready Tokenized Receivable Metadata

The table below defines the minimum data fields a bank needs to capture at origination for a receivable to meet collateral eligibility standards. This bank-ready receivables data schema supports invoice verification before tokenization and ensures receivable eligibility for digital collateral.

Group 1: Invoice Data Fields

Field Name | Source | Evidence Required | Pass/Fail Rule |

invoice_id | ERP / e-invoicing | Unique ID in source system | Must be unique |

invoice_amount | ERP | Matches source system | Must be positive |

invoice_currency | ERP | Bank collateral policy | Must be approved |

due_date | ERP | Eligible timeframe | Within policy limits |

purchase_order_ref | ERP | PO number | Must exist |

invoice_document_hash | Document system | Cryptographic hash | Must match source |

delivery_document_hash | Trade system | Cryptographic hash | Must match source |

Group 2: Legal and Debtor Data Fields

Field Name | Source | Evidence Required | Pass/Fail Rule |

issuer_entity_id | KYC registry | Verified KYC record | Must exist |

debtor_entity_id | KYC registry | Verified KYC record | Must exist |

debtor_confirmation_status | Confirmation portal | Signed confirmation | Must be true |

debtor_confirmation_timestamp | Confirmation portal | Confirmation log | Must be recent |

assignment_restriction_flag | Legal review | Legal opinion | Must be false |

notice_of_assignment_status | Legal system | Notice record | Must be completed |

governing_law | Contract system | Contract terms | Must be approved |

delivery_evidence_ref | Trade document system | Signed receipt or BOL | Must exist |

Group 3: Risk and Monitoring Data Fields

Field Name | Source | Evidence Required | Pass/Fail Rule |

duplicate_check_status | Registry query | Clean registry result | Must be true |

registry_check_timestamp | Registry system | Query log | Must be current |

debtor_credit_score | Credit system | Current credit report | Above threshold |

repayment_history_score | Trade data | Payment records | Above threshold |

dispute_status | Dispute system | Dispute log | Must be false |

pledge_status | Collateral system | Current lien state | Must be unpledged |

collection_account_ref | Banking system | Account details | Must be verified |

These fields support monitoring, substitution, audit, and regulatory reporting. These fields support the full collateral lifecycle. This tokenized receivables verification checklist ensures complete invoice verification before tokenization.

Need a bank-ready verification checklist for tokenized receivables? Schedule a receivables data assessment with our trade finance specialists at TokenMinds: https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What makes a receivable eligible for digital collateral?

A: The receivable must pass authenticity, debtor, delivery, legal, duplicate financing, and risk checks. The bank should record each result as structured metadata before tokenization.

Q: What happens if a receivable fails one verification check but passes the others?

A: It depends on which check fails. A failed duplicate financing check or a legal assignment restriction is typically a hard stop. A marginal debtor credit score may result in a reduced advance rate rather than outright rejection. Banks should define their eligibility rules before the program goes live, not case by case after invoices start arriving.

Q: How does this checklist connect to ongoing monitoring?

A: The eight verification areas at origination map directly to the monitoring triggers during the collateral lifecycle. Debtor credit deterioration, overdue payment, and disputed delivery are the most common events that require action. Capturing structured metadata at origination is what makes automated monitoring possible.

Q: What data is needed to tokenize receivables?

A: Banks need invoice, debtor, delivery, legal, duplicate financing, risk, and repayment data. Each field should have evidence and a pass/fail rule before tokenization.

References

Chainlink: "Invoice Tokenization in Trade Finance." Identifies verification, debtor credit risk, and invoice authenticity as core requirements before tokenization. https://chain.link/article/invoice-tokenization-trade-finance

ONINO: "How to Tokenize Invoices & Trade Receivables in 2026." Identifies verification, debtor relationship confirmation, and credit risk assessment as core requirements before tokenization. https://onino.io/blog/how-to-tokenize-invoices-and-trade-receivables