TL;DR

Tokenized receivables collateral depends on clean, verified data from upstream systems. This guide maps the full integration path. It covers how invoice records move from ERP and e-invoicing networks into the tokenization layer. It defines the debtor confirmation workflow, the event sequence from issuance to release, and the API checkpoints at each stage. It also addresses exception handling and off-chain reconciliation.

Why Integration Is the Real Implementation Challenge

Most tokenized receivables programs stall at the integration layer. The token format is not the hard part. Getting clean, verified invoice data from legacy systems into a collateral workflow is.

Chainlink identifies ERP data, debtor details, and payment terms as core inputs for tokenized invoices. Those inputs do not arrive automatically. They require deliberate integration design across three source systems: the seller's ERP, the e-invoicing network, and the debtor confirmation channel.

Each system has its own data format, validation rules and update frequency. The integration layer must reconcile all three into a single bank-grade collateral record.

Stage 1: Extract and Send Data from ERP Systems

The ERP system should provide invoice data as the source of truth. This includes the invoice ID, amount, currency, due date, payment terms, and underlying trade reference.

Banks cannot accept unstructured or manually entered invoice data for collateral purposes. The data must come directly from the ERP via a secure API connection. This removes human error from the origination step.

The extraction process has three steps. First, the ERP creates the invoice. Second, an API call sends the structured record. Third, the platform validates the record against field completeness and format rules.

At this point, any invoice that is not validated is rejected. It does not go into the collateral workflow. The rejection is logged with an error code and timestamp and remediated.

ERP Data Field | Validation Rule | Rejection Trigger |

invoice_id | Unique, not previously submitted | Duplicate hash match |

invoice_amount | Positive decimal, within policy limits | Zero or negative value |

invoice_currency | Valid ISO 4217 code | Unrecognized currency code |

due_date | Future date, within eligible maturity window | Past due or outside policy range |

payment_terms_days | Integer, matches policy parameters | Outside eligible terms range |

Stage 2: Integration of E-Invoicing Network

E-invoicing networks offer an independent layer of invoice validation. They verify that the invoice has been registered in a government or network registry, outside the ERP record.

Across many markets, PEPPOL is widely used for structured e-invoice exchange, especially in Europe and parts of Asia-Pacific. In North America, EDI networks fulfill the same roles in trade corridors. Both transmit structured invoice data between buyer and seller systems with compliance logging built in.

For bank collateral purposes, e-invoicing network integration provides three things. First, it confirms the invoice was formally transmitted to the debtor. Second, it provides a network-level timestamp that supports the audit trail. Third, it enables cross-reference between the ERP record and the network record, which is a strong duplicate financing control.

Banks should require that invoices submitted for tokenization carry a network transmission reference where e-invoicing infrastructure exists in the relevant market. Invoices without a network reference are not automatically ineligible, but they require additional manual verification steps.

Read What Data Must Banks Verify Before Tokenizing Accounts Receivable? for the full verification checklist that e-invoicing data feeds into.

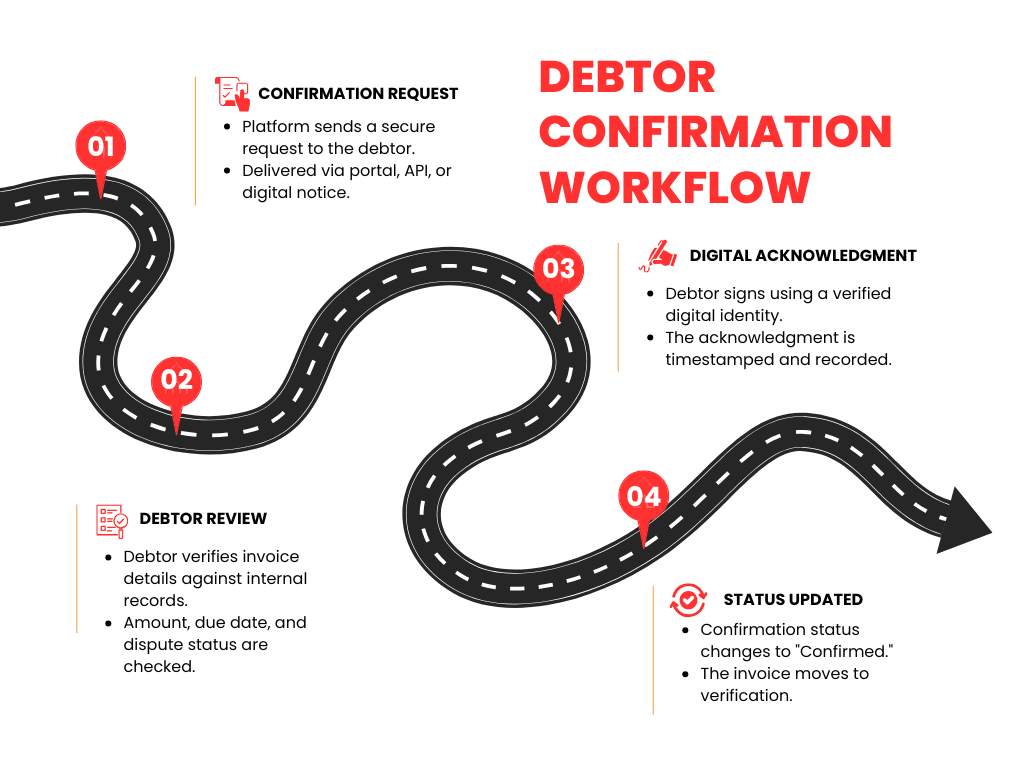

Stage 3: Debtor Confirmation Workflow

Debtor confirmation is the most operationally complex integration point. It requires a secure, documented acknowledgment from a third party outside the bank's direct control.

The confirmation workflow follows four steps:

The bank sends a secure confirmation request to the debtor via API or portal.

The debtor reviews invoice details, verifies amounts and due dates, and digitally acknowledges the obligation.

The platform logs the cryptographic confirmation with a timestamp and links it to the token record.

If the debtor rejects or disputes the invoice, it is flagged and removed from the eligible pool.

If the confirmation is not received in the time window, the invoice’s status is changed to Pending Timeout. Whether the timeout results in an automatic rejection or manual escalation is defined in the bank policy.

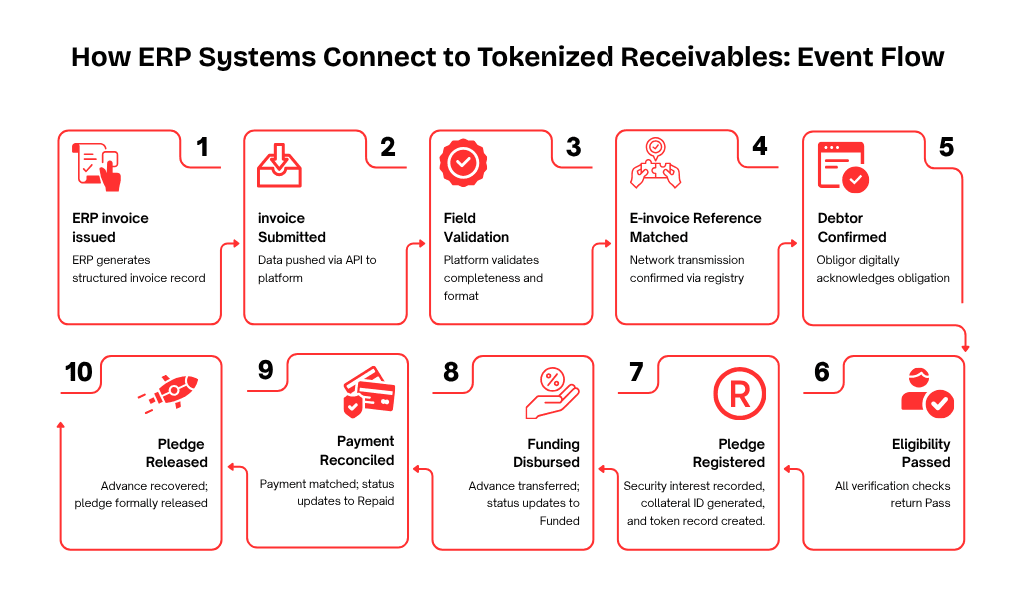

Stage 4: Event Sequencing from Issuance to Release

Every step in the collateral lifecycle is a logged event. The sequence is fixed. No stage can be skipped without triggering a system exception.

Event | Trigger | System Actor |

Invoice Issued | ERP pushes invoice record to platform | ERP integration layer |

Validation Passed | All required fields present and valid | Platform validation engine |

E-Invoicing Reference Matched | Network transmission reference confirmed | E-invoicing connector |

Debtor Confirmation Received | Cryptographic acknowledgment logged | Confirmation portal |

Eligibility Check Passed | All verification events return Pass outcome | Verification engine |

Pledge Registered | Security interest recorded in registry | Collateral operations |

Funding Disbursed | Advance amount transferred to seller | Treasury system |

Payment Received | Debtor payment confirmed and reconciled | Reconciliation engine |

Pledge Released | Advance recovered, release authorized | Collateral operations |

Each event record carries a timestamp, an actor ID, and a reference to the previous event. This creates an unbroken chain from origination to release.

Read Tokenized Invoice Data Model 2026: Fields Banks Need Before Collateral Approval for the full field-level specification behind each event record.

Stage 5: API Checklist for Bank Integration Teams

The integration architecture requires specific API endpoints at each stage. The table below defines the minimum API surface for a bank-grade tokenized receivables program.

Endpoint | Method | Purpose |

/invoices/submit | POST | Push invoice record from ERP to platform |

/invoices/{id}/status | GET | Retrieve current invoice and collateral status |

/invoices/{id}/validate | POST | Trigger field validation and duplicate check |

/confirmation/request | POST | Send confirmation request to debtor |

/confirmation/{id}/status | GET | Check debtor confirmation status |

/verification/run | POST | Trigger full verification event sequence |

/pledge/register | POST | Register security interest and generate collateral ID |

/funding/disburse | POST | Record advance disbursement against collateral |

/payments/reconcile | POST | Match incoming payment to token record |

/pledge/release | POST | Initiate pledge release after full repayment |

/audit/events/{id} | GET | Retrieve full event log for a collateral position |

These endpoints are complemented with webhook triggers. Payment events, confirmation updates and exception flags are pushed to the bank’s system in real time. The bank does not need to poll for status changes.

Bank API controls should include:

OAuth or signed API authentication

Idempotency keys for duplicate submission control

Webhook retry logic

Payload schema validation

API versioning

Immutable audit logs

Read Bank-Grade API Requirements for Tokenized Trade Collateral Platforms for the full API specification and security requirements.

Stage 6: Exception Handling

Four exception types require defined handling logic. Leaving them to manual resolution creates bottlenecks and audit gaps.

Invoice amount difference. Invoice amount in ERP does not match invoice amount on e-invoicing network record. The invoice is on hold for manual review. Both source records are flagged for reconciliation prior to the verification stage proceeding.

Rejected debtor confirmations. The debtor disputes the amount of the invoice, the due date or the underlying trade. The invoice will be excluded from the eligible pool. The seller will be informed about the reason for the rejection. A new invoice cannot be submitted for the same trade until the dispute is resolved.

Duplicate submissions. There is a platform invoice with identical hash. The second submission is rejected immediately. The originator receives an error code with the reference ID of the existing record.

Payment failures. The debtor payment is returned, reversed or only partially received and the shortfall is flagged by the reconciliation engine. The pledge is active and the bank collections workflow is triggered according to the default policy defined.

Stage 7: Reconciliation of Off-chain to On-chain

The token status must always match the real-world payment status. If a token shows Funded when the debtor has already paid, it results in a false collateral position.

Reconciliation is via payment event webhooks. The webhook fires when the debtor’s bank confirms a payment that matches the invoice reference, amount and currency. The reconciliation engine validates the match. The token status updates to Repaid. The pledge release process begins.

A payment can update the token status to Repaid only when:

The payment reference matches the invoice ID.

The payment amount covers the outstanding advance.

The payment currency matches the advance currency.

If any condition fails, the payment is logged as a partial match. The engine triggers a manual review flag. The token status does not change until the review is resolved.

Security and Access Controls

Cross-system data flows introduce data privacy and access control risks. Three controls apply across the full integration.

Role-based permissions. Each system actor, ERP connector, confirmation portal, verification engine, collateral operations, and treasury, has defined read and write permissions. No actor can update records outside its scope of responsibility.

All data in transit is encrypted. All API calls between source systems and the tokenization platform are encrypted with TLS 1.2 or higher. Invoice data, debtor details and payment records are encrypted end-to-end.

Regulatory audit logging. Every API call is logged with a timestamp, actor ID, and payload hash. Logs are immutable. Regulators and internal auditors can retrieve a complete record of every data exchange for any collateral position.

Build an ERP-to-Collateral Integration Map With TokenMinds

Tokenized receivables programs need more than smart contracts. Banks need a clear integration path from ERP records, e-invoicing references, debtor confirmation, funding events, and repayment reconciliation.

TokenMinds helps banks and fintech teams design the API flow, collateral event model, and verification architecture needed for tokenized receivables collateral.

Book a call to map your ERP-to-collateral workflow. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: How can banks confirm debtor acceptance before funding invoices?

A: Banks can send a secure confirmation request to the debtor through a portal, API, or digital notice. The debtor verifies the amount, due date, and dispute status. Funding should only proceed after the confirmation is recorded, timestamped, and linked to the invoice record.

Q: Does the ERP need to be changed to support this integration?

A: Not always. Most modern ERP systems support API-based data export, without custom development. The integration layer is between the ERP and the tokenization platform. It does the translation and validation of the format. The ERP works as it should.

Q. What if the network is down when I submit?

A. The platform queues the invoice and polls the network reference on a schedule. The invoice proceeds to the verification stage only when the network reference is complete. If the network does not come back online in the retry window, the invoice is flagged for manual review.

Q: Can a bank run this integration without a PEPPOL-connected e-invoicing network?

A: Yes it can. PEPPOL connectivity adds an independent validation layer but is not a hard requirement in all markets. Where no e-invoicing network exists, the bank must apply additional manual verification steps to compensate. The verification checklist in CM-39 defines what those steps look like.

References

Chainlink: "Invoice Tokenization in Trade Finance." Tokenized invoices are based on core inputs such as ERP data, debtor information and payment terms. https://chain.link/article/invoice-tokenization-trade-finance

OpenPeppol: "PEPPOL Bis Billing 3.0 Specifications." Defines the standard for e-invoice exchange and network validation across European and APAC markets. https://docs.peppol.eu/poacc/billing/3.0/

ISO: "ISO 4217 Currency Codes." Official standard for three-letter currency codes used in ERP and financial system integration. https://www.iso.org/iso-4217-currency-codes.html

NIST: "Transport Layer Security (TLS) Guidelines." Provides security standards for encrypting data in transit between ERP, banking, and tokenization platforms. https://csrc.nist.gov/news/2019/nist-publishes-sp-800-52-revision-2

ISO: "ISO 20022 Financial Services." Defines the global standard for electronic data interchange between financial institutions, including invoice and payment message formats. https://www.iso.org/standard/92561.html