TL;DR

Digital warehouse receipts turn paper-based collateral records into electronic or hybrid workflows, depending on legal recognition. The harder question is operational. This guide maps issuance, control, pledge, transfer, and release. It adds jurisdictional branching logic, collateral substitution workflows, an event-driven audit model, role accountability mapping, and a phased adoption path.

Why the Workflow Matters More Than the Format

UNIDROIT notes that warehouse receipt systems help borrowers access credit. These systems can use electronic platforms and other digital mechanisms. The format change is not the point.

What matters is whether each step still works. Issuance must be reliable. Control must be enforceable. The workflow must adapt to the legal environment where the goods sit.

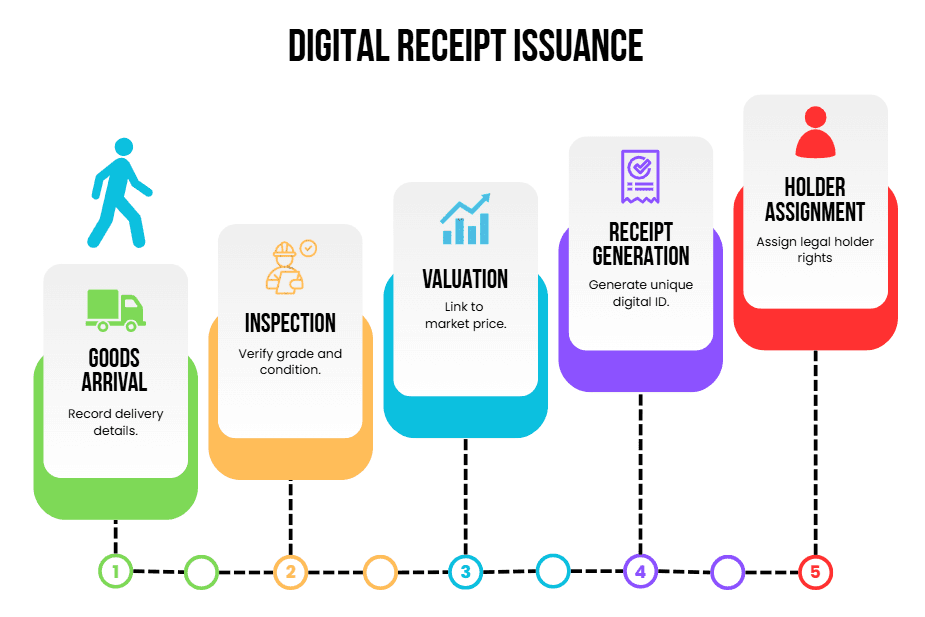

Stage 1: Issuance Workflow

The issuance sequence includes 5 steps. Goods receipt records the date, quantity and source of delivery. Inspection checks quantity, grade and condition against delivery documents. Valuation links the goods to a known price reference. Receipt generation creates the digital record and assigns a unique ID. Holder assignment names the depositor as the party who can claim or transfer the goods.

A receipt missing inspection or valuation is incomplete. Banks should not accept it as eligible collateral.

Jurisdictional Branching: Two Workflows, Not One

Most guides describe a single digital workflow. That assumes every jurisdiction recognizes electronic warehouse receipts equally. Many do not.

Branch A: Electronic receipts are legally recognized.

The receipt exists only in digital form. Pledge status changes are made directly in the system. The status lock is the primary control. No controlling paper receipt needs to be tracked in parallel. Supporting documents may still be retained for audit, inspection, or compliance.

Branch B: Electronic receipts are not yet recognized.

The paper receipt remains the legally controlling document. A digital record is a parallel tracking layer, not a substitute. A bank must hold or control the physical paper receipt, often through a custodian. Status changes in the digital system must be matched by physical endorsement of the paper document. Any mismatch between the two records is a blocking issue.

Question | If Yes | If No |

Does local law recognize electronic warehouse receipts? | Use Branch A: digital pledge workflow | Use Branch B: hybrid paper and digital process |

Does the warehouse operate across two jurisdictions? | Confirm recognition in both | Apply the stricter jurisdiction's rules to the full pledge |

Banks running multi-country programs must confirm recognition status for each storage location before deciding which branch applies. A program that assumes Branch A everywhere will fail in jurisdictions still on Branch B.

Read How Banks Verify Inventory Ownership and Control Before Tokenization for the verification steps that apply before either branch begins.

Stage 2: Control Versus Ownership

Control and ownership are not the same thing. This distinction matters most during enforcement.

Legal title generally stays with the borrower during the pledge. The bank holds a security interest over the goods or receipt.

Security interest is the bank’s legal claim if the borrower defaults. The security interest comes from the pledge agreement and any registry filing.

Operational control is the practical ability to stop the goods from moving. This should be defined in the warehouse agreement.

The bank may have a security interest but not operational control if the warehouse continues to operate under the borrower’s instructions. Three components establish operational control: the authority to instruct written into the warehouse agreement, a status lock preventing transfer once pledged, and a tripartite agreement between the bank, the borrower, and the warehouse.

Warehouse Obligations in the Digital Receipt Workflow

A digital warehouse receipt only works if the warehouse follows clear obligations. The platform record does not replace operational responsibility.

Warehouse Obligation | Why It Matters |

Confirm goods received | Prevents receipts for goods not in storage |

Record quantity, grade, and condition | Supports valuation and eligibility checks |

Block release after pledge | Protects lender control |

Notify exceptions | Flags damage, shortage, disputes, or insurance gaps |

Support inspection access | Allows independent verification |

Reconcile stock and receipt records | Prevents mismatch between goods and documents |

Follow bank release instructions | Ensures pledged goods do not move without approval |

Lender Rights Under a Pledged Digital Receipt

The lender does not need to own the goods. It needs enforceable rights over the pledged receipt.

Common lender rights include:

The right to block transfer or release,

The right to receive warehouse notices,

The right to inspect or request inspection,

The right to require margin top-ups,

The right to approve substitution,

The right to direct release after repayment,

The right to enforce after default.

These rights should appear in the pledge agreement, warehouse agreement, platform permissions, and registry process.

Stage 3: Pledge Mechanics

The pledge instrument should link the receipt ID, borrower, lender, facility, warehouse operator, secured goods, and enforcement rights.

Transition | Trigger | Who Confirms or Records |

Unpledged to Pledged | Verification passed, advance approved | Bank collateral team |

Pledged to Funded | Advance disbursed | Treasury system |

Funded to Repaid | Payment confirmed | Reconciliation system |

Repaid to Released | Bank authorization, operator confirmation | Bank and warehouse jointly |

Each transition is recorded with a timestamp and an actor ID. Pledge registration is not a one-time event.

Transfer Workflow

A digital warehouse receipt should not transfer freely once pledged. The system must check receipt status before every transfer request.

Transfer State | Required Control |

Unpledged receipt | Holder can request transfer |

Pledged receipt | Transfer blocked unless lender approves |

Substituted receipt | Transfer allowed only after replacement pledge |

Released receipt | Transfer allowed after bank release confirmation |

Disputed receipt | Transfer blocked until the exception clears |

Collateral Substitution and Partial Release

Inventory pools evolve during the lifetime of a loan. Borrowers sell goods and substitute them with new stock. The workflow must be able to handle these transactions without at any moment weakening the bank’s position.

Substitution sequence

The borrower delivers substitute goods to the warehouse. The operator creates a top-up record for the delivery.

An independent inspector reviews the new items against the eligibility policy.

The valuation step prices the new goods at the current market reference price. The warehouse issues a new receipt for the replacement goods, including a note of the substitution request. The bank confirms the new receipt, the pledge is recorded, and the status of the new receipt is Pledged. The bank releases the original receipt only after the new pledge has been verified. The original receipt status is changed to Released.

Step | Action | Control Check |

1. Top-up delivery | New goods arrive at the warehouse. | Linked to existing facility ID |

2. Inspection | An independent inspector verifies new goods | Must meet eligibility policy |

3. Valuation | New goods priced at current reference | Recorded against substitution request |

4. New receipt issued | Digital receipt created for replacement goods | Cross-referenced to original receipt |

5. New pledge registered | New receipt status set to Pledged | Bank authorization recorded |

6. Original receipt released | Original receipt status set to Released | Only after step 5 confirmed |

The order of steps 5 and 6 is the critical control point. Releasing the original receipt before the new pledge is confirmed creates a gap where the bank holds less collateral than the advance requires.

Partial release

When the borrower repays part of the advance, the release quantity is calculated against the current verified collateral value, not the original value. If prices have fallen, fewer goods are released per unit of repayment.

Event-Driven Audit Ledger

A list of logged events is useful. A chain of cross-referenced events is stronger evidence for regulatory review.

Each event in the collateral lifecycle should reference the event that triggered it. This creates a traceable chain rather than a flat list.

Event | References | Why the Link Matters |

Inspection completed | Goods receipt record | Confirms inspection matches a real delivery |

Valuation recorded | Inspection result | Shows valuation used confirmed quantity and condition |

Pledge registered | Verification checklist, valuation | Shows pledge was based on confirmed, valued goods |

Margin call issued | Updated valuation, original pledge value | Shows the basis for the value drop |

Insurance update logged | Policy renewal date, prior certificate | Confirms continuous coverage with no gap |

Substitution registered | New receipt, original receipt | Links replacement to the position it replaces |

Release authorized | Repayment confirmation, final valuation | Shows the release matches what was actually owed |

A regulator reviewing a margin call can trace it back to the valuation event, and from there to the inspection that confirmed the underlying quantity. A flat event log without these references requires manual reconstruction. A linked chain does not.

Operational Role Matrix

Multiple parties participate in the workflow beyond the bank, borrower, and warehouse operator. The table below maps accountability across the main stages.

Activity | Responsible | Accountable | Consulted | Informed |

Issuance and inspection | Independent surveyor | Warehouse operator | Bank collateral team | Borrower |

Pledge registration | Bank collateral officer | Bank credit risk lead | Legal counsel | Warehouse operator |

Ongoing monitoring | Collateral manager | Bank risk officer | Independent surveyor | Borrower |

Insurance verification | Bank operations | Bank operations lead | Insurer | Borrower |

Substitution approval | Bank collateral team | Bank credit risk lead | Independent surveyor | Warehouse operator |

Enforcement on default | Bank legal counsel | Bank credit risk lead | Registry operator | Borrower, warehouse operator |

External audit review | External auditor | Bank head of internal audit | Bank collateral team | Bank board risk committee |

This matrix prevents a common gap. Without it, monitoring often has no clearly accountable party, and exceptions sit unresolved between teams.

Implementation Maturity Path

Banks rarely deploy a full digital warehouse receipt workflow at once. A phased rollout keeps legal, operational, and collateral risk under control.

Phase 1 digitizes receipt records. The bank moves receipt data into a shared system. Paper may still remain the controlling legal document.

Phase 2 adds pledge control. The bank introduces status locks, tripartite agreements, and pledge transition logs. This phase tests whether control works in daily operations.

Phase 3 automates monitoring. The system schedules valuation updates, eligibility checks, and margin alerts. Exceptions move to credit, collateral, or operations teams.

Phase 4 completes the audit model. Events become linked across issuance, valuation, pledge, substitution, and release. Regulatory exports can then support review without manual reconstruction.

For how this workflow connects to broader legal recognition of electronic documents, read MLETR, eBLs, and Warehouse Receipts: The Legal Layer Behind Tokenized Trade Collateral.

The Most Common Failure: Double-Pledged Receipts

A borrower could present the same receipt to two different lenders. This happens when a receipt exists outside a shared registry.

The status lock from Stage 2 is the primary defense. It only works if the warehouse operator checks status before confirming any new pledge request.

Build a Digital Warehouse Receipt Workflow With TokenMinds

Banks do not need to replace paper-based collateral workflows overnight. The better path is to map the current receipt process, confirm legal recognition, define pledge controls, and test the workflow through a controlled pilot.

TokenMinds helps commodity finance and trade operations teams design digital warehouse receipt workflows across issuance, holder control, pledge registration, substitution, release, audit trails, and jurisdictional branching.

Book a digital warehouse receipt pilot workshop with TokenMinds. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What happens if a warehouse operates across two jurisdictions with different legal recognition rules?

A: The bank should apply the stricter jurisdiction's rules to the full pledge. If goods are stored in a location that does not accept electronic receipts, the hybrid paper and digital process applies to those goods even if the other location would qualify for a full digital workflow.

Q: Why is the order of steps important in the collateral substitution?

A: The new pledge must be confirmed before releasing the original receipt. If the order is reversed, there is a gap where the bank's collateral value is temporarily below the outstanding advance. This gap is a real exposure, even if it lasts only minutes.

Q: Who is accountable if ongoing monitoring is missed?

A: Under the role matrix above, the bank's risk officer is accountable for monitoring, even though the collateral manager is responsible for performing it. This is important because accountability cannot be outsourced even if the task is outsourced to an external party.

Q: Can electronic warehouse receipts be pledged as collateral?

A: Yes, if local law recognizes electronic warehouse receipts and the bank can enforce pledge control. In jurisdictions without full recognition, the paper receipt may remain the controlling document, while the digital record supports tracking, monitoring, and audit.

Q: How does a warehouse receipt lending workflow operate?

A: It starts with goods receipt, inspection, valuation, and digital receipt issuance. The bank then verifies control, records the pledge, locks transfer status, monitors collateral value, and authorizes release or enforcement based on repayment or default.

References

UNIDROIT: Model Law on Warehouse Receipts. Notes that warehouse receipt systems facilitate access to credit and may include electronic platforms, distributed ledger systems, and other mechanisms. https://www.unidroit.org/studies/model-law-on-warehouse-receipts/