TL;DR

Tokenizing inventory does not prove who controls it. That proof must come before the token is created. This guide maps nine verification steps from warehouse operator confirmation through title records, lien searches, insurance, valuation, inspection, segregation, and release authority. It adds three layers most guides omit: ongoing monitoring after origination, an evidence and audit-trail framework, and an exception-management decision matrix for each failure type.

What Proves Bank Control Over Inventory Collateral?

Bank control usually depends on five linked proofs:

A valid warehouse receipt,

Verified borrower title or depositor records,

Clean or subordinated lien position,

Physical inspection and segregation,

Bank-controlled release authority.

A token should only be created after these controls are approved and linked to the collateral record.

Why Ownership Verification Comes Before Tokenization

A token records a claim. It does not create one. If the underlying ownership or control is flawed, the token records a flawed claim precisely.

A warehouse receipt does not only describe stored goods. It identifies the warehouse operator, the holder, the goods, the quantity, and the storage location. For banks, that makes the receipt the starting point for control verification, pledge design, and release authority.

UNCITRAL-UNIDROIT Model Law treats warehouse receipts as records issued by warehouse operators. They acknowledge goods held for a named holder. Depending on the receipt type and governing law, the holder may have enforceable rights in the goods or in the receipt. The bank must verify borrower holder status, pledge rights, and prior claims before tokenization.

These verifications must happen before any token is minted.

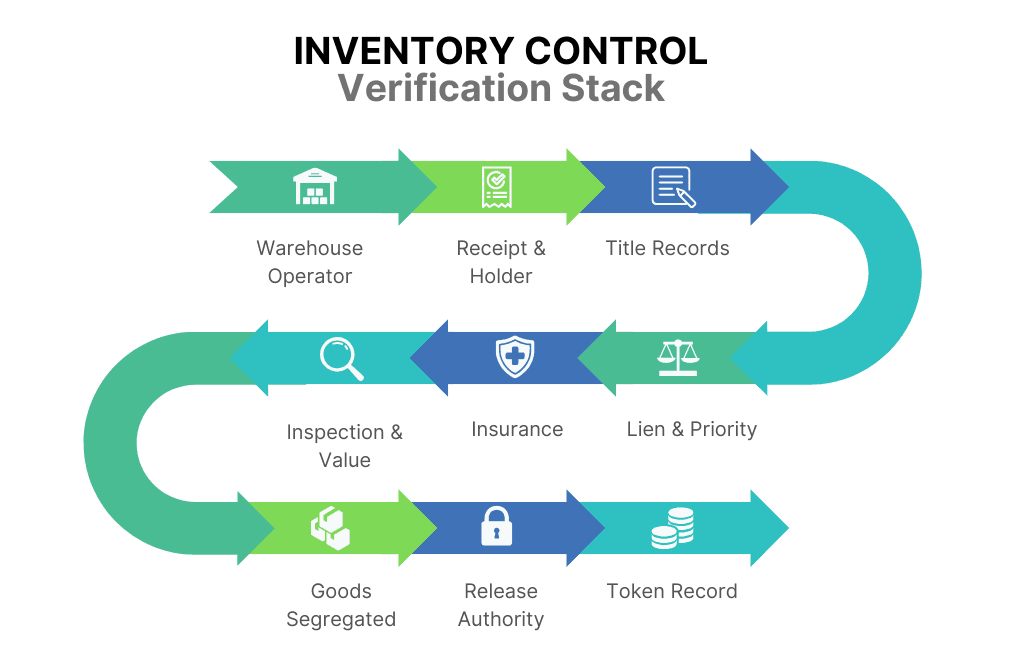

The Nine-Step Verification Checklist

Step | Control Objective | Required Evidence | Hard Stop |

1. Warehouse operator confirmation | Confirm the goods are held by a valid operator | License, receipt number, location, quantity, date | Any missing receipt field |

2. Depositor title verification | Confirm the borrower can pledge the goods | Invoice, transport record, customs record | Description mismatch |

3. Receipt holder status | Confirm the borrower controls the receipt | Certified receipt copy, warehouse statement | Prior pledge or transfer |

4. Lien search and priority checks | Confirm bank priority | Registry search result | Unreleased prior lien |

5. Check insurance coverage | Confirm full replacement value coverage | Insurance certificate, loss payee designation | Lapse or missing loss payee |

6. Valuation and condition reporting | Confirm current market value and condition | Condition report, price reference | Stale report (>30 days perishables, >90 days durables) |

7. Physical inspection | Confirm goods exist and match receipt | Independent inspector count/weigh report | Quantity short or location mismatch |

8. Separation of inventory | Confirm pledged goods are segregated | Written operator confirmation | Co-mingled inventory |

9. Release authority and dual-control | Confirm bank controls release | Tripartite agreement, dual-control policy | Operator accepts non-bank instructions |

Step 1: Warehouse operator confirmation. The operator must have a current warehouse license. The receipt must identify the operator’s name and license number, depositor’s identity, description of goods, quantity, storage location, date issued, and a unique receipt number. Any missing field is a hard stop.

Step 2: Depositor title verification. Depositing goods does not prove ownership. The bank must match the receipt description against the purchase invoice, transport document, and any customs records. Quantity, grade, and condition must align across all documents. A description mismatch is a hard stop.

Step 3: Receipt holder status. The bank must be satisfied that the borrower is the current bona fide holder of the receipt. The documentation required is a certified copy of the receipt showing the borrower as holder, a written statement from the warehouse operator that there is no prior pledge or transfer recorded, and a signed statement from the borrower that the receipt is unencumbered.

Step 4: Lien search and priority checks. Prior liens defeat the bank's collateral position. The search scope depends on jurisdiction.

Lien Search Type | Jurisdiction | What It Covers |

UCC-1 financing statement | United States | All personal property including inventory |

Personal property security registries | Australia, New Zealand, Canada, where applicable | Inventory and other personal property |

Civil law security, pledge, or asset registry | Where applicable | Registered security interests |

Warehouse receipt registry | Select markets | Pledges against specific receipts |

An unresolved prior lien is a hard stop. The bank must not proceed until a formal release is confirmed in the registry.

Step 5: Check insurance coverage. The policy must cover full replacement value. The bank must be named as loss payee. Fire, flood, theft, and commodity-specific risks must be covered. A lapse in policy or loss payee designation is a hard stop.

Step 6: Valuation and condition reporting. Commodity inventory links to a recognized price reference updated at a frequency matching asset volatility. A condition report from an independent inspector must be current. Any report over 30 days old for perishables or 90 days for durables is stale and requires a new inspection.

Step 7: Physical inspection. The goods are to be physically counted or weighed by an independent inspector. Confirm that the storage location matches receipt. A quantity short or location mismatch is a hard stop.

Step 8: Separation of inventory. The pledged goods must be physically separated from non-pledged goods. The warehouse operator confirms segregation in writing at each pledge registration. Co-mingled inventory is a hard stop.

Step 9: Release authority and dual-control. The warehouse operator accepts release instructions only from the bank. Releases above a defined value threshold require two separate bank officers. The warehouse operator must confirm that the token status shows Release Approved before physically releasing any goods. After release, the token record should be updated to Released with a warehouse confirmation timestamp.

Ongoing Collateral Monitoring After Origination

Verification at origination is not sufficient. Inventory value, condition, and legal status change over time. Banks must run four monitoring controls continuously.

Monthly warehouse confirmations. Each month the warehouse operator signs a confirmation stating the quantity on hand as of that date, the condition of storage and that there have been no unauthorized movements. Any discrepancy against the token record triggers an immediate exception.

Periodic re-inspections. Independent inspections occur on a schedule tied to asset classes. Perishable goods require inspection every 30 days. Durable commodities require inspection every 90 days. If the inspection result falls below the eligibility threshold, a margin call or partial release suspension is activated.

Automatic insurance renewal checks. The monitoring system tracks policy expiry dates. An alert fires 30 days before renewal. If insurance is not confirmed renewed by the expiry date, new advances against the affected receipts are suspended immediately.

Event-driven lien re-searches. A lien re-search is triggered by four events: borrower financial distress signals, a new financing statement filed against the borrower, a court judgment against the borrower, or a change in the borrower's corporate structure. The re-search result is logged in the collateral record with a timestamp.

Monitoring Control | Frequency | Trigger for Exception |

Warehouse confirmation | Monthly | Quantity discrepancy or unauthorized movement |

Physical re-inspection | 30 or 90 days by asset class | Condition below eligibility threshold |

Insurance renewal check | 30 days before expiry | Policy not renewed by expiry date |

Lien re-search | Event-driven | New filing, judgment, or restructuring |

Evidence and Audit-Trail Framework

The verification process generates a set of required artifacts. Each artifact has a defined owner, retention period, and approval status. Banks that do not retain these documents in a structured way cannot support regulatory review or enforcement proceedings.

Artifact | Owner | Retention Period | Approval Required |

Warehouse license confirmation | Bank operations | Duration of program plus 7 years | Relationship manager |

Original warehouse receipt or authoritative electronic receipt record | Bank collateral team | Duration of pledge plus 7 years | Collateral officer |

Depositor title documents | Bank credit team | Duration of program plus 7 years | Credit officer |

Lien search result | Bank legal | At each search date plus 7 years | Legal counsel |

Insurance certificate | Bank operations | Per policy period plus 7 years | Operations lead |

Condition report | Bank collateral team | Per inspection date plus 7 years | Independent inspector |

Warehouse monthly confirmation | Bank operations | Monthly plus 7 years | Warehouse operator |

Release authorization record | Bank collateral team | Per release event plus 7 years | Two authorized officers |

Retention periods should be adjusted for local regulation, bank policy, and litigation hold requirements.

Each artifact is linked to the token record as a document reference. The link should be immutable or recorded in an append-only audit trail. Status changes to the token record trigger automatic document completeness checks. A status transition to Pledged is blocked if any mandatory artifact is missing or expired.

This creates the bridge between physical verification and digital collateral management. Every token status change has a complete evidence chain behind it. That chain is auditable, exportable, and available for regulatory review on demand.

For the next workflow step, read Digital Warehouse Receipts for Bank Collateral: How the Workflow Works.

Exception-Management Decision Matrix

Hard stops are identified at each verification step. Banks also need defined remediation paths. The matrix below covers the most common exception types.

Exception Type | Severity | Immediate Action | Remediation Path |

Minor document mismatch | Low | Flag for review, hold token at Pending | Borrower provides corrected document within 5 days |

Description mismatch between receipt and title documents | High | Hard stop, suspend verification | Independent reconciliation, new receipt issued if confirmed |

Insurance deficiency | High | Suspend new advances against affected receipts | Insurance reinstated and confirmed within 5 business days |

Prior perfected lien identified | Critical | Hard stop, legal review initiated | Formal subordination or release from prior filer, confirmed in registry |

Stale condition report | Medium | Exclude receipt from advance calculation | New inspection completed and report accepted |

Segregation failure | High | Suspend affected receipts, notify warehouse operator | Written operator confirmation of re-segregation |

Failed monthly warehouse confirmation | High | Freeze token, trigger inspection | On-site inspection within 10 business days |

Lien re-search reveals new filing | High | Pause new advances, legal review | Priority confirmed or subordination obtained |

Remediation timelines are not suggestions. A borrower that fails to meet the remediation deadline triggers the next severity level. A minor mismatch that is not resolved in five days escalates to a high-severity exception. A high-severity exception that is not resolved in the defined window triggers a default event review.

For document comparison, read Warehouse Receipts vs Bills of Lading vs Inventory Tokens: Which Document Controls the Collateral?

Verify Inventory Control Before Tokenization With TokenMinds

Banks should not tokenize inventory until ownership, lien status, warehouse control, insurance, valuation, inspection, segregation, and release authority are verified.

TokenMinds helps asset-based lending and risk teams design pre-tokenization control workflows, evidence frameworks, monitoring rules, and exception paths for inventory-backed collateral programs.

Request a bank-grade inventory control verification checklist tailored to your lending workflow. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: How can banks verify inventory ownership before lending?

A: Banks verify inventory ownership by matching warehouse receipts against depositor records, purchase invoices, transport documents, customs records, lien searches, insurance certificates, inspection reports, and warehouse operator confirmations.

Q: What proves control over tokenized inventory collateral?

A: Control is proven through valid receipt holder status, clean lien priority, physical segregation, bank-controlled release authority, and a complete evidence chain linked to the token record.

Q: How do warehouse receipts verify stored goods?

A: Warehouse receipts identify the operator, holder, goods, quantity, location, issue date, and receipt number. Banks still need inspection, title checks, and lien searches before treating the receipt as collateral evidence.

Q: Can a bank accept a warehouse receipt without a physical inspection?

A: No. The receipt describes what should be there. Only a physical inspection confirms what is actually there. Skipping inspection creates direct fraud exposure. The bank may take a lien against goods that do not exist or are below the stated quality. Physical inspection at origination is a hard requirement.

Q: What happens if a lien search reveals a prior filing that covers inventory generally but not the particular goods pledged?

A: The bank must secure a written subordination from the prior filer. It must specifically cover the goods in question. A general release of the financing statement is stronger but not always available. Legal counsel must confirm the subordination is enforceable in the relevant jurisdiction before the verification step is marked complete.

Q: How does the evidence framework relate to the digital collateral record?

A: Each artifact is stored as a document reference linked to the token. The link is created at the time the artifact is accepted. It cannot be removed. A token status transition is blocked if any mandatory artifact is missing, expired, or flagged as under review. This means the digital record always reflects the actual state of the physical verification evidence behind it.

References

UNCITRAL-UNIDROIT: Model Law on Warehouse Receipts. Treats warehouse receipts as records issued by warehouse operators acknowledging goods held for a named holder, providing the legal basis for control and pledge design. https://uncitral.un.org/en/mlwr