Key Takeaways:

Solana's rise to 154,942 retail RWA wallet holders signals a structural shift in where everyday investors are choosing to hold tokenized assets, driven by near-zero fees, fast settlement, and growing product availability on the network.

Issuers and asset managers can reach this market by implementing a four-layer infrastructure stack covering token issuance on Solana, wallet compliance screening on every transfer, DeFi-connected secondary market access, and automated distribution and regulatory reporting at retail scale.

For years, one question sat at the back of every retail RWA product discussion. Which blockchain will everyday investors actually use?

The answer came on March 7, 2026. Analytics platform RWA.xyz reported that Solana crossed 154,942 wallets holding tokenized real-world assets. Ethereum stood at 153,592. It was the first time in history that any blockchain had beaten Ethereum in RWA wallet holder count.

The milestone did not come from institutions. It came from retail. A wave of everyday investors, drawn by Solana's near-zero transaction fees, had piled into fractional tokenized equity products starting in mid-2025. Solana's RWA holder count went from roughly 126,000 in January 2026 to more than 154,000 in six weeks.

Ethereum still leads on total value. It holds $15.5 billion in tokenized RWAs against Solana's $1.8 billion. Institutional products anchored to BlackRock, Fidelity, and other major names keep Ethereum's dollar figures dominant. But wallet holder count tells a different story. Retail investors are choosing Solana. They are already there, holding tokenized assets, and the number keeps growing.

That gap between Ethereum's capital and Solana's users is exactly where the product opportunity sits, as outlined in this asset tokenization framework.

What is Retail RWA

Retail RWAs are tokenized versions of real-world assets issued on the Solana blockchain and distributed to individual investors in fractional units. These assets can include private credit, real estate, treasury products, or commodities. Because Solana transactions cost fractions of a cent and settle in seconds, it enables retail investors to participate in markets traditionally reserved for institutions.

Why Solana Is the Right Chain for Retail RWA Products

Retail participation in tokenized assets is not the same problem as institutional adoption. Institutions need legal certainty, counterparty controls, and settlement finality at scale. Retail investors need access, low cost, and a simple onboarding path. Solana solves the retail side of that equation better than any chain today.

Transaction fees are near zero

The average Solana transaction costs a fraction of a cent. On Ethereum, gas fees during peak periods can exceed the value of a small retail position. That cost alone locks out the investors most likely to engage with fractional RWA products. Solana removes that barrier entirely.

Settlement is fast

Solana finalizes transactions in seconds. Retail investors expect the same responsiveness they get from a stock trading app. A tokenized asset that settles in seconds fits that expectation. T+2 settlement does not.

The retail user base is already there

Solana's 154,942 RWA wallet holders are not a projection. They exist today. Any new product issued on Solana enters a market with an established, active retail holder base from day one.

Regulatory momentum is building

Six spot Solana ETFs were approved in October 2025. Western Union chose Solana for its stablecoin remittance platform, serving 150 million customers across 200 countries. Galaxy Research projects Solana's tokenized capital markets will reach $2 billion in 2026. The network has moved well beyond its earlier reputation and into mainstream retail finance.

What Retail RWA Distribution Actually Changes

To understand what this means in practice, consider a single example. A mid-market asset manager wants to offer a tokenized private credit note to retail investors on Solana. The note pays a fixed return backed by a pool of trade finance receivables. Minimum ticket on the traditional version is $50,000. The retail investor base the manager wants to reach holds $500 to $5,000 to invest.

Tokenization makes that product accessible. But technology is not the hardest part. What changes operationally when retail investors are the end buyer is what most issuers have not fully worked through yet.

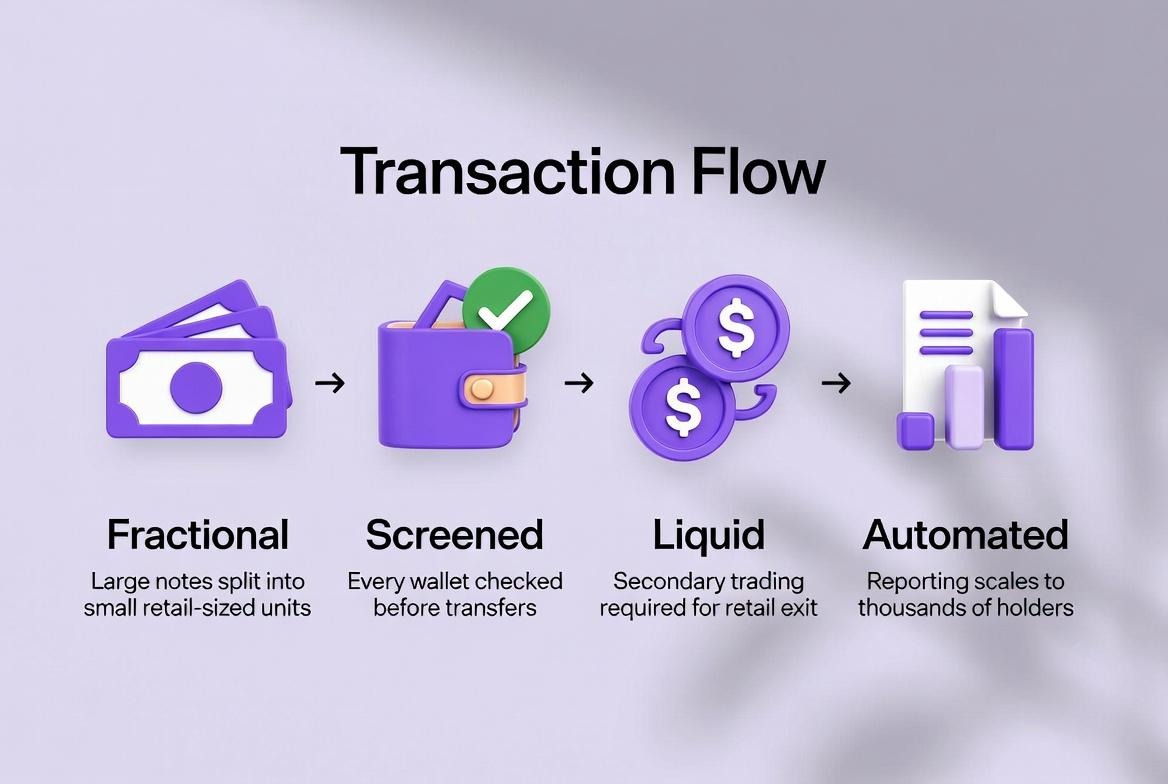

1. Fractionalization becomes essential

The $50,000 note can be split into 50,000 units at $1 each, or 5,000 units at $10 each, without changing the legal rights of any holder. Every unit carries the same economic exposure, the same payment entitlement, and the same legal claim on the underlying receivables. The manager reaches a market that could not access this product at all before tokenization.

2. KYC must happen at the wallet level, not just at account opening

When the manager issues the note to retail buyers on Solana, every wallet that receives or sends the token must be screened before the transfer settles. One-time onboarding checks are not enough. A wallet that passed KYC on day one could appear on a sanctions list on day 90. The compliance engine must check every transfer, not just the first one, and the result must attach automatically to the transaction record before settlement releases.

3. Secondary market access is not optional

A retail investor who buys a $10 unit of a private credit note needs a way to sell it before maturity. Without a compliant secondary market, the product is just an illiquid position with a Solana address. Approved trading venues must be connected from the day the product launches, with the same KYC and AML controls that applied at issuance enforced on every subsequent transfer.

4. Reporting must work at retail scale

The asset manager in this example has one compliance team. If the product has 5,000 holders and generates 15,000 transfers in the first month, manual monitoring is not a strategy. Every transaction, distribution event, and compliance flag must be captured, logged, and reported automatically.

What Launching a Retail RWA Product on Solana Requires

Issuing the token is only the first step. The four systems below are what turn a tokenized asset into a product that retail investors can buy, hold, trade, and trust, and that regulators can audit.

Compliant issuance on Solana: The token must give holders the same legal rights as the underlying asset. For the asset manager's private credit note, that means every unit holder has the same entitlement to payments, the same rights in default, and the same legal standing as a holder of the paper version.

The issuance platform must produce a written legal opinion confirming that equivalence before the product goes live. Without it, the token does not qualify for regulatory recognition as a financial product regardless of which blockchain it runs on.

Retail KYC and wallet compliance screening: Every wallet that sends or receives the token must be screened before settlement releases. Standard AML tools screen bank accounts and SWIFT codes. They do not screen Solana wallet addresses.

The moment an issuer processes an on-chain transfer without wallet-level screening, they are operating outside their compliance boundary. Screening must gate settlement automatically. The result must attach to the transaction record with a timestamp and a named compliance owner before any transfer completes.

Fractional distribution and secondary market access: Fractionalization must be built into the token structure at issuance, not added afterward. And once retail holders own the token, they need a way to trade it. That means connecting the product to an approved secondary trading venue that enforces the same compliance controls as the primary issuance.

Every resale, every wallet-to-wallet transfer, every DeFi interaction must run through the same KYC and AML gate as the original purchase.

Compliance monitoring and automated reporting: Real-time transaction monitoring is the baseline standard for any retail financial product. The 5,000 holders and 15,000 monthly transfers in this example cannot be reviewed manually. Monitoring tools must flag unusual activity, apply transfer limits, generate distribution records, and produce regulatory reports automatically.

The output must sync to internal systems without manual formatting or reconciliation.

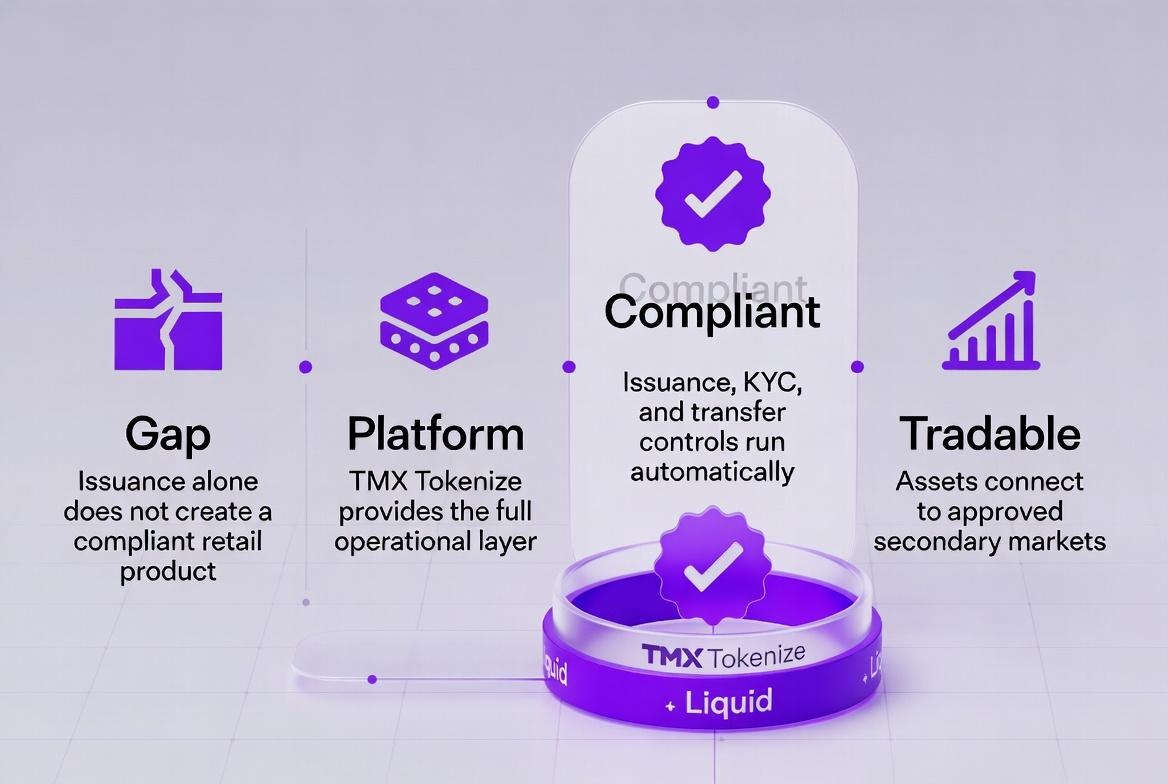

How TMX Tokenize Provides the Operational Layer

The operational gap most issuers face is not a Solana problem. The chain works. The retail demand is real. What is missing is the layer between issuing a token and running a compliant product that retail investors can actually buy, hold, and trade.

TMX Tokenize by TokenMinds is built to close that gap. It is an all-in-one tokenization platform that handles compliant issuance, retail KYC, secondary market access, and compliance monitoring inside a single system. Coming back to the asset manager launching the private credit note on Solana: here is what each part of the operational layer looks like when TMX Tokenize handles it.

1. Multi-chain compliant issuance including Solana

TMX Tokenize supports compliant asset issuance across Ethereum, BNB Chain, Stellar, Algorand, and Midnight, with Solana's token standards and transfer logic fully integrated. Legal equivalence is built into the issuance workflow. The manager's private credit note launches with the legal opinion, the smart contract transfer restrictions, and the compliance documentation already in place.

2. Automated KYC and AML compliance at the wallet level

Every wallet that interacts with a TMX-issued token is screened automatically before settlement releases. The platform enforces identity verification, sanctions screening, and AML checks on every transfer, not just the first one. Every screening result is logged with a timestamp, a compliance rule reference, and a named owner, and attached to the transaction record automatically. The 5,000 retail holders in this example are covered without a compliance analyst reviewing each one manually.

3. Trust levels and transfer controls

TMX Tokenize lets issuers set transaction limits by user trust tier, restrict access by IP or country, and enforce transfer rules at the smart contract level. The private credit note can be restricted to verified retail investors in approved jurisdictions. Those restrictions are enforced on-chain on every transfer automatically, not through a manual approval queue.

4. DeFi-ready secondary market access

TMX Tokenize connects issued assets to approved DeFi venues for trading and price discovery. Retail holders of the private credit note can buy and sell on-chain through compliant venues without leaving the compliance boundary of the original issuance. The same KYC and AML controls that applied at the primary sale apply to every secondary transfer through those venues.

5. Institutional liquidity through the Canton Network

For issuers that want institutional demand alongside retail distribution, TMX Tokenize connects directly to the Canton Network. The network hosts over $6 trillion in assets and more than $300 billion in daily transaction volume. Goldman Sachs, HSBC, DTCC, and the European Investment Bank all participate. The asset manager's private credit note can reach institutional buyers through Canton at the same time it reaches retail buyers on Solana.

TMX Tokenize is available as a fully branded white-label solution. The asset manager deploys the platform under their own name, logo, and domain without rebuilding the compliance and issuance infrastructure from scratch. The operational layer is already built. The brand is theirs.

What This Looks Like in Practice

The asset manager launches the tokenized private credit note on Solana through TMX Tokenize. The token gives every holder the same legal rights as the paper version of the note. A legal opinion confirming that equivalence is produced before the product goes live. Without that opinion, the token is a digital file, not a financial product.

Retail investors buy the token through a compliant front-end. Before any transfer settles, the buyer's wallet is screened automatically for KYC, AML, and sanctions risk. The transfer is not released until screening passes. The compliance result attaches to the transaction record with a timestamp and a named compliance owner.

Settlement on Solana happens in seconds. The token and the payment move at the same time. There is no T+2 window. There is no counterparty exposure sitting open between trade and settlement.

Transfer restrictions are enforced at the smart contract level. Only wallets that have passed the compliance gate can receive the token. Compliance is not a checkpoint the investor passes once at signup. It is enforced on every single on-chain movement of that token, for every holder, for the entire life of the product.

On the quarterly payment date, the smart contract calculates each holder's share based on their token balance and sends the distribution directly to their Solana wallet. No payment file to prepare. No manual processing. No errors from mismatched ledger records. 5,000 distributions go out in one automated execution.

The audit trail is complete and exportable without anyone assembling it by hand. Every transfer, every compliance check, every distribution event has a transaction hash, a block timestamp, and a wallet address. The compliance team gets automated monitoring flags. The manager gets structured reports. Regulators get a clean audit trail. Nobody is reviewing 15,000 transactions manually.

That is what a retail RWA product looks like when the operational layer is built correctly on Solana.

The Retail RWA on Solana Readiness Index

Most issuers and asset managers do not know how ready their current setup is to launch a retail RWA product on Solana. This index scores readiness across four areas. Each area is scored 1 to 4. A score of 1 means nothing is in place. A score of 4 means fully ready. Total out of 16.

Area | 1 - Not Started | 2 - Basic | 3 - In Progress | 4 - Fully Ready |

Compliant Issuance on Solana | No tokenization setup. Traditional distribution only. | Sandbox tests done. No legal equivalence confirmed. | Live on one chain. Legal opinion in progress. | Tokens confer identical legal rights. Live on Solana. Legal opinion complete. |

Retail KYC and Wallet Screening | No wallet screening. Legacy AML tools only. | Manual KYC. Wallet screening runs after settlement. | KYC gates settlement. Results not logged automatically. | Automated KYC and AML gates every transfer. Logs attached with timestamp and owner per transaction. |

Fractional Distribution and Secondary Access | No fractional structure. No secondary market. | Assets issued but illiquid. No trading venue. | DeFi venue connected. Liquidity limited. | Fractional tokens live in approved venues with real-time price discovery and retail access. |

Compliance Monitoring and Reporting | No on-chain monitoring. Manual audits only. | Basic reporting. High exception backlog. | Auto-monitoring for standard transfers. Exceptions are still manual. | Real-time monitoring and fraud detection. Full regulatory reporting automated across all holders. |

Score guide:

4 to 6: You cannot safely launch a retail RWA product on Solana yet. On-chain activity creates unmanaged compliance exposure.

7 to 10: Partial coverage. KYC or distribution gaps will surface under regulatory review.

11 to 13: Well-placed. Remaining gaps are optimization, not structural risk.

14 to 16: Fully ready. Your setup meets the operational standard a live retail RWA launch requires.

Where most issuers start:

Area | Score | Why |

Compliant Issuance on Solana | 1 | No tokenization infrastructure in production. Legal equivalence not confirmed. |

Retail KYC and Wallet Screening | 1 | Retail wallet addresses sit entirely outside existing AML screening scope. |

Fractional Distribution and Secondary Access | 2 | Products exist but no approved secondary trading venue connected at launch. |

Compliance Monitoring and Reporting | 1 | No on-chain monitoring. Compliance relies on manual review after the fact. |

Total | 5/16 | Not ready to launch a retail RWA product on Solana without infrastructure changes. |

The gap between 5 and 16 is not a technology gap. Solana works. The retail demand is real. What most issuers are missing is the operational layer that turns a token into a compliant product. TMX Tokenize provides that layer.

Retail RWA Infrastructure by Chain

Solana leads in retail wallet holders, but it is not the only chain where RWA products are being built. Each major chain has a distinct strength and a real limitation. Issuers choosing a chain for a retail RWA product need to understand both.

Chain | Strength | Limitation |

Solana | Near-zero fees, 154,942 retail RWA wallet holders, fast finality | Institutional infrastructure still emerging compared to Ethereum |

Ethereum | Deepest institutional RWA liquidity, $15.5B in tokenized assets, strongest legal precedent | Gas costs during peak periods exceed the economics of small retail positions |

Stellar | Built for payment-focused RWAs, low cost, strong in remittance and stablecoin distribution | Smaller DeFi ecosystem limits secondary market options for retail holders |

Algorand | Strong compliance tooling, used by financial institutions in regulated markets | Smaller retail user base and limited secondary market liquidity |

Avalanche | Institutional subnet tokenization, customizable compliance environments | Retail user base significantly smaller than Solana or Ethereum |

BNB Chain | Large retail user base, low fees, broad DeFi connectivity | Perceived centralization raises questions for regulated product issuers |

Solana is the strongest chain for retail distribution right now because of where the users already are. Ethereum remains dominant for institutional capital. The most sophisticated issuers are not choosing one or the other. They are issuing on Solana for retail reach and connecting to Ethereum-adjacent institutional infrastructure, such as the Canton Network, for liquidity depth. TMX Tokenize supports issuance across all chains in this table, which means issuers do not have to make a permanent choice at launch.

How a Compliant Transfer Actually Executes on Solana

The technical stack described earlier has a specific sequence every time a token moves. Understanding that sequence is what makes the compliance architecture concrete rather than theoretical.

Here is what happens from the moment a retail investor submits a trade request to the moment the token arrives in their wallet.

Step 1. Trade request submitted. The investor initiates a transfer through the product front-end or a connected secondary venue. The request hits the smart contract with the sending wallet address, the receiving wallet address, and the token amount.

Step 2. KYC registry check. The transfer hook queries the on-chain KYC registry. It checks whether the receiving wallet address has a valid, current verification status. If the wallet has never been verified, the transfer is blocked immediately. If verification has lapsed or been revoked, the transfer is blocked. Only wallets with active verified status pass this step.

Step 3. Sanctions oracle query. The transfer hook simultaneously queries the sanctions screening oracle with both wallet addresses. The oracle checks against live OFAC, EU, and UN sanctions lists. This check runs on every transfer, not just at onboarding. A wallet that was clean at initial KYC but appears on a new sanctions list will be caught here. If either wallet returns a hit, the transfer is blocked and the event is logged automatically.

Step 4. Jurisdiction and rule validation. The execution contract checks product-specific transfer rules. This includes jurisdiction restrictions, holding period lockups, maximum wallet concentration limits, and trust tier transfer caps. A retail investor in a restricted country fails here even if their wallet passed KYC and sanctions screening. The rules are enforced at the contract level, not through a manual compliance review.

Step 5. Transfer executes. If all four checks pass, the token transfer executes atomically on Solana. The token leaves the sending wallet and arrives in the receiving wallet in the same transaction. There is no partial settlement. The transfer either completes fully or does not happen at all.

Step 6. Audit log written. The completed transaction is logged automatically with the transaction hash, block timestamp, sending wallet, receiving wallet, token amount, KYC registry result, sanctions oracle result, and jurisdiction rule outcome. This record is immutable and exportable. It forms the audit trail that compliance teams submit to regulators without any manual assembly.

The entire sequence from trade request to settled transfer and logged audit record takes seconds on Solana. In a traditional settlement process, steps two through six involve manual checks, custodian notices, and reconciliation work that can take two days. The compliance outcome is the same. The time and operational cost are not.

How Retail and Institutional Liquidity Connect

Retail tokens issued on Solana and institutional instruments on the Canton Network are not separate products. They are two access points to the same underlying asset.

Retail tokens are issued on Solana with full transfer hook compliance. A corresponding instrument is issued on Canton for institutional counterparties. Oracle feeds synchronize pricing between both markets in real time. When liquidity is thin on the retail side, institutional participants can provide depth through Canton. When institutional demand rises, the issuance layer directs new supply to whichever market needs it.

The compliance boundary holds on both sides. Retail transfers enforce KYC and sanctions checks on Solana. Institutional transfers enforce Canton's own counterparty controls. Same asset, same price feed, two compliant access points.

Conclusion

Solana has already won the retail RWA holder race. More wallets hold tokenized real-world assets on Solana than on any other blockchain as of March 7, 2026. The users are there. The fees are low. The network is fast. The regulatory momentum is building.

The asset manager trying to reach retail investors with a tokenized private credit note does not have a demand problem. Solana's 154,942 active RWA holders represent a retail base that already buys and holds tokenized assets. The problem is the operational gap between issuing a token and running a compliant product that retail investors can actually buy, hold, and trade.

What is left is operational. Retail RWA products need compliant issuance that establishes legal equivalence, KYC automation that gates every transfer at the wallet level, secondary market access that enforces compliance at the point of every resale, and real-time monitoring that generates clean regulatory reports at retail volume.

The issuers that build this operational layer now will launch into an ecosystem that is already primed for them. Those that wait will spend 2026 watching competitors capture the retail base that is already on Solana, already holding tokenized assets, and already looking for the next product to buy.

TMX Tokenize by TokenMinds provides the full operational stack, compliant issuance, automated KYC, DeFi distribution, and real-time compliance monitoring, for issuers ready to launch retail RWA products on Solana today.

FAQ

What are retail RWA products on Solana?

Retail RWA products on Solana are tokenized real-world assets, such as private credit notes, real estate fractions, or commodities, issued on the Solana blockchain and sold to individual investors in small denominations. Solana's low fees and fast settlement make it the most practical chain for retail-scale distribution of tokenized assets.

Why does retail RWA tokenization require wallet-level KYC?

Retail investors hold assets in blockchain wallets. Standard AML tools screen bank accounts and payment identifiers, not wallet addresses. Without wallet-level screening that runs on every transfer, an issuer cannot verify that a tokenized asset is moving between compliant parties. Wallet screening must gate settlement automatically on every transfer, not just at account opening.

What is the minimum viable operational setup to launch on Solana?

An issuer needs four things: a compliant issuance platform that confirms legal equivalence, an automated KYC and AML layer that screens wallets before every settlement, a secondary trading venue that applies the same compliance controls as the primary issuance, and real-time transaction monitoring that produces automated compliance reports at retail volume.

What is TMX Tokenize?

TMX Tokenize is a tokenization platform built by TokenMinds that helps issuers and asset managers launch, manage, and distribute tokenized assets across multiple blockchains including Solana. It connects compliant issuance with automated KYC, DeFi-ready secondary market access, and real-time compliance monitoring so issuers can run retail RWA products inside existing regulatory frameworks without rebuilding their core infrastructure.

How does TMX Tokenize connect to institutional liquidity?

TMX Tokenize connects directly to the Canton Network, which hosts over $6 trillion in tokenized assets and more than $300 billion in daily transaction volume. Participants include Goldman Sachs, HSBC, DTCC, and the European Investment Bank. Issuers can reach institutional buyers through Canton and retail buyers through Solana from the same platform simultaneously.