TL;DR

Tokenized receivables collateral is only as strong as the legal framework behind it. This article maps the key legal readiness areas banks must check before accepting tokenized receivables as collateral. It covers control, assignment, third-party effectiveness, priority, enforcement, governing law, cross-border challenges, and a practical checklist. Each section translates legal requirements into bank workflow terms.

Why Legal Readiness Cannot Be Deferred

Banks move fast on technology. Legal frameworks move slower. That gap creates real risk in tokenized collateral programs.

A token records a pledge. It does not create one. The legal security interest must be established and perfected under applicable law. Absent that, the bank has a strong track record of operations but a weak legal claim.

This is the very issue that UNCITRAL’s 2026 colloquium on digital assets and secured transactions is addressing. It’s focused on tokenized assets, priority, control, enforcement and cross-border challenges as the core unresolved issues. Banks can’t wait for full legal harmonization. They need a readiness framework now.

Can Tokenized Receivables Be Used as Collateral Legally?

Yes, tokenized receivables can be used as collateral where the bank has a valid security agreement, assignment or pledge structure, perfection method, priority position, and enforceable rights under applicable law. The token itself does not create the security interest. It supports evidence, control, auditability, and transfer tracking. The legal claim still depends on local secured transactions law, debtor notice, registry recognition, insolvency rules, and enforcement rights.

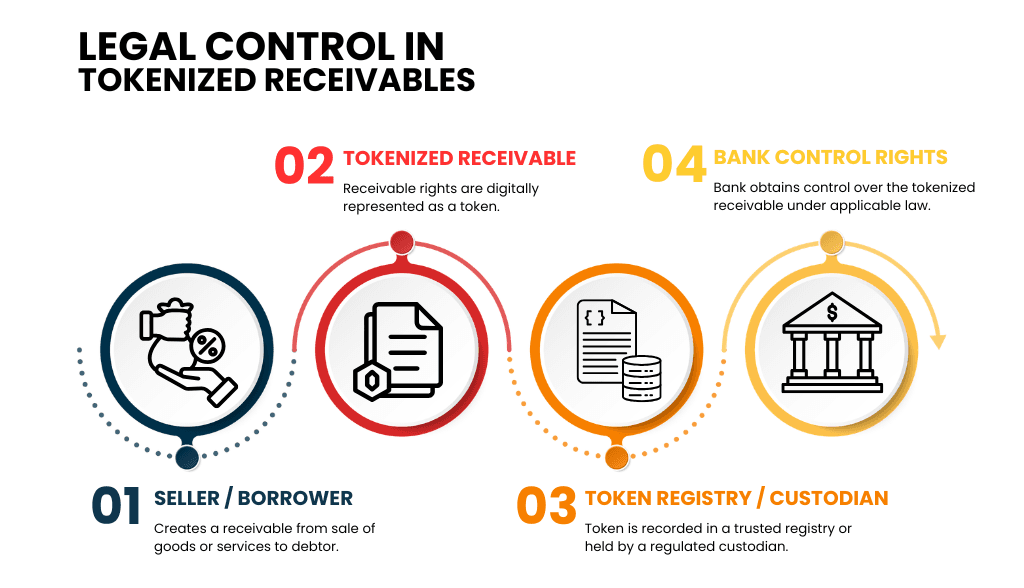

Legal Control: What It Means for Tokenized Receivables

Control is the foundational concept in secured transactions law. Recognized control can strengthen enforcement and priority. Without recognized control, perfected assignment, or another valid legal mechanism, enforcement may be delayed, challenged, or subordinated.

For traditional receivables, control means holding the right to collect payment. For tokenized receivables, control has an additional dimension. The bank must be able to control, transfer, or restrict the token without the seller's cooperation.

This is more than a pledge agreement. The bank needs either direct access to the token registry or a custodial arrangement where a trusted intermediary holds the token on the bank's behalf. A pledge that only exists in a side agreement, without registry-level control, is operationally weak.

To avoid confusion between technical and legal control, banks should assess five distinct layers:

Control Layer | What Banks Must Check |

Token-layer control | Can the bank freeze, transfer, or restrict token movement? |

Registry control | Is the control record legally recognized? |

Receivable control | Does the bank hold enforceable rights over the payment claim? |

Debtor-payment control | Has the debtor been notified or directed where to pay? |

Enforcement control | Can the bank collect, sell, or enforce after default? |

Assignment Mechanics: Notice, Consent, and Perfection

Assignment is the transfer by the seller of its rights in the receivable to the bank. Perfection is the making by the bank of the transfer effective against third parties.

The requirements for assignment vary by jurisdiction. In many common law jurisdictions, there is a requirement for written notice to the debtor for the assignment to be effective against third parties. In civil law jurisdictions, there may be specific steps for registration. Some jurisdictions require both.

Perfection steps for digital collateral are still evolving in many markets. Banks must confirm what is required in each relevant jurisdiction before the program goes live.

Jurisdiction Type (Illustrative Only) | Assignment Requirement | Perfection Step |

Common law (e.g., UK, Australia) | Written notice to debtor | Notice delivery confirmed and logged |

Civil law markets | Formal assignment, notice, date-certainty, or registration may be required | Local law review required for debtor notice, third-party effect, and insolvency priority |

UCC Article 9, US | Depends on collateral classification | UCC-1 filing is commonly required for accounts or payment intangibles; control may apply only for specific collateral categories |

Hybrid or emerging markets | Varies by local statute | Legal opinion required per jurisdiction |

*Note: Priority under UCC Article 9 generally follows the earlier of filing or perfection time. Token registry entries do not automatically override or substitute for statutory filing requirements unless expressly recognized by law.

Read How to Prevent Double Financing in Tokenized Invoice Collateral for the operational controls that support perfection and priority tracking.

Debtor Defenses and Payment-Direction Risk

Receivables collateral depends not only on the seller and lender but also on the debtor. Banks must assess five debtor-related risks before accepting tokenized receivables as collateral:

Question | Why It Matters |

Can the debtor dispute the invoice? | A tokenized claim is weaker if the underlying receivable is disputed. |

Has the debtor acknowledged the assignment? | This supports payment redirection and enforcement. |

Can the debtor set off other claims? | Set-off can reduce collateral value. |

Are anti-assignment clauses present? | These may affect transfer, enforcement, or debtor cooperation. |

Has proof of assignment been prepared? | Debtors may need evidence before paying the assignee. |

These considerations are especially relevant under frameworks like UCC Article 9, which include specific rules on debtor notification, proof of assignment, and restrictions on assignment. Banks should document debtor acknowledgment and payment instructions as part of the token metadata.

Third-Party Effectiveness: When the Pledge Binds Others

A properly perfected security interest is intended to be effective against third parties, subject to applicable secured transactions and insolvency law. These include other creditors, insolvency administrators and purchasers of the receivable.

Third-party effectiveness is the legal test that counts most in a default scenario. Should the seller become insolvent, the bank will have to prove that its pledge was perfected before the insolvency date. A pledge that was not properly perfected can be set aside by the administrator.

Third-party effectiveness for tokenized receivables usually depends on legally recognized perfection steps. These may include filing, debtor notice, registry entry, or another method accepted under local law. A private registry known only to the lender and borrower may not be enough unless the relevant law recognizes it. Second, the registration must predate any competing claims.

Timing is critical. Earlier perfection generally has priority over later perfection, subject to local law and competing-claim rules. Token timestamp records prove this, but only if the underlying registry is legally recognized in the jurisdiction concerned.

Priority Rules: Token Registry vs. Traditional Filing Systems

Priority determines who gets paid first when there are competing claims against the same asset.

Priority is generally determined by the order of perfection. Thus, a creditor who first perfects its security interest will have priority over creditors who perfect later. This rule applies to tokenized receivables collateral as it does to conventional collateral.

The complication arises when a token registry and a traditional filing system both record claims on the same receivable. Priority outcomes depend on whether the token registry has legal standing in the relevant filing system. Where it does not, the bank should file in the traditional system as well. Dual registration is redundant operationally but essential legally in many markets.

Enforcement Pathways: Remedies and Liquidation

Enforcement is the final test of collateral quality. A pledge that cannot be enforced efficiently is not bank-grade collateral.

Enforcement for tokenized receivables follows three stages. First, the bank declares an event of default under the lending agreement. Second, it invokes its rights under the security agreement and exercises its rights over the pledged receivable. Third, it collects payment from the debtor or liquidates the position.

The token record can support enforcement because it provides evidence of chain of custody, pledge timing, valuation, and subsequent activity. This evidence has value in contested enforcement proceedings.

Cross-border enforcement is even more complicated. A security interest perfected under English law may not be recognised automatically in a jurisdiction where the debtor is located, which means banks need to map out the enforcement pathway for each relevant debtor jurisdiction before accepting cross-border receivables as collateral.

Governing Law and Jurisdiction

Choice of law determines which legal system governs the pledge. It is one of the most consequential decisions in a tokenized collateral program.

Three governing law questions arise in every program. First: which law governs the receivable itself? This is usually the law of the contract between the seller and the debtor. Second: which law governs the security agreement between the bank and the seller? This is typically chosen by the parties. Third: which law governs perfection and priority against third parties?

The third question is the most complex. In many jurisdictions, perfection is determined by the law of the debtor's location, not the law chosen by the parties to the pledge agreement. Thus a bank that chooses English law for its security agreement may still have to satisfy local perfection requirements in the debtor's country.

Legal counsel should prepare a governing law matrix for each program. This matrix should map each receivable type, debtor jurisdiction and applicable perfection requirement.

Cross-Border Recognition and MLETR

UNCITRAL’s Model Law on Electronic Transferable Records (MLETR) provides a framework for the recognition of electronic trade documents. It is relevant for tokenized receivables where the underlying trade documents are electronic as well.

If a jurisdiction has MLETR alignment, it has legislation that treats electronic records the same as paper originals. MLETR adoption remains uneven. UNCITRAL's status list includes jurisdictions such as Singapore, Bahrain, Abu Dhabi Global Market, and the UK. Banks should confirm the exact domestic law position in each debtor jurisdiction before relying on electronic records, digital assignment notices, or token-based pledge records.

Where MLETR-aligned law applies, electronic transferable trade documents may have clearer legal recognition. Banks should still confirm whether digital debtor confirmations, assignment notices, and token-based pledge records are recognized under the specific domestic law.

Where MLETR alignment does not exist, banks face conflict-of-laws risk. A pledge that is valid under the governing law of the security agreement may be unenforceable in the debtor's jurisdiction.

Read MLETR, eBLs, and Warehouse Receipts: The Legal Layer Behind Tokenized Trade Collateral for a full treatment of electronic document recognition across trade finance asset classes.

Legal Readiness Checklist for Banks

The questions below define the minimum legal review a bank should complete before accepting tokenized receivables as collateral.

Legal Readiness Area | Question to Answer |

Control | Does the bank have registry-level control over the token, not just a contractual right? |

Assignment | Has a valid assignment notice been delivered to and confirmed by the debtor? |

Perfection | Has the security interest been perfected under the law of the debtor's jurisdiction? |

Third-party effectiveness | Is the pledge registered in a way that gives constructive notice to other creditors? |

Priority | Has the bank looked for prior claims in both the token registry and traditional filing systems? |

Enforcement | Has the bank mapped the enforcement pathway for each debtor jurisdiction in the program? |

Governing law | Has legal counsel produced a governing law matrix covering the receivable, security agreement, and perfection? |

MLETR alignment | Has the bank confirmed that the jurisdiction of the debtor accepts electronic trade documents? |

Insolvency risk | Has the bank confirmed that the pledge survives seller insolvency under applicable law? |

Cross-border recognition | Has the bank confirmed that its security interest is recognized in all relevant debtor jurisdictions? |

This checklist is a starting point. It does not replace legal opinion. Each program requires jurisdiction-specific advice from qualified counsel.

Build a Digital Collateral Legal-Readiness Checklist With TokenMinds

TokenMinds helps banks and fintech teams map tokenized receivables from asset data to legal control, assignment, perfection, priority, and enforcement readiness.

For teams reviewing tokenized receivables collateral, TokenMinds can support a jurisdiction-specific checklist covering registry control, debtor notice, filing requirements, custody setup, legal opinion inputs, and operational controls.

Book a consultation to prepare your digital collateral legal-readiness checklist. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: Does a token automatically create a legally enforceable security interest?

A: No. The token is the record of the pledge. To be legally enforceable, a valid security agreement is needed, proper assignment notice and perfection are required under applicable law. A well-structured token record supports each of these steps. It does not replace them.

Q: What happens to a tokenized pledge if the seller becomes insolvent?

A: Perfected security interests generally should survive a seller's insolvency, subject to local insolvency law, avoidance rules, vulnerability periods, fraud rules, and debtor defenses. The bank's claim is against the receivable and not against the seller. An insolvency administrator may still challenge a perfected pledge under local insolvency law, including avoidance rules, vulnerability periods, fraud rules, preference rules, or debtor-defense claims. Banks should check the applicable clawback period in each relevant jurisdiction.

Q: Is it necessary to adopt UNCITRAL MLETR in order to make a tokenized receivables program work legally?

A: No. MLETR alignment strengthens the legal standing of electronic documents in the program. It is not a hard requirement. Banks operating in non-MLETR jurisdictions must apply additional legal steps to establish the equivalence of electronic records. That typically needs express contractual acknowledgement and, to an extent, parallel paper documentation.

References

UNCITRAL: Digital Assets and Secured Transactions Colloquium 2026. Addresses tokenized assets, priority, control, enforcement, and cross-border challenges as core issues in secured transactions law. https://uncitral.un.org/en/platforms-st

UNCITRAL: Model Law on Electronic Transferable Records (MLETR) – Status. Lists jurisdictions with MLETR-aligned legislation including Bahrain, Singapore, Abu Dhabi Global Market, and the UK. https://uncitral.un.org/en/texts/ecommerce/modellaw/electronic_transferable_records/status

Uniform Commercial Code: Article 9 – Secured Transactions. Governs perfection and priority rules for security interests in accounts, payment intangibles, and other receivables under US law. https://www.law.cornell.edu/ucc/9