TL;DR

Double financing is one of the oldest fraud patterns in trade finance. Tokenization reduces the risk but does not eliminate it automatically. This article matches six risk areas with bank-grade safety steps. It covers finding double invoices, checking if debtors are real, and building safe asset registries. It also looks at tracking off-chain cash moves and handling canceled invoices. Each section defines the control mechanism, not just the problem.

Why Double Financing Survives Into Tokenized Programs

Double financing occurs when one seller pledges one invoice twice. It has existed in paper-based trade finance for decades. The assumption that tokenization solves it entirely is wrong.

A token represents a claim. If two platforms each mint a token for the same underlying invoice, two lenders each hold what looks like a valid collateral instrument. Neither token is technically fraudulent. The fraud is in the origination, not the token itself.

Chainlink identifies invoice authenticity and debtor credit verification as core requirements before tokenization. The security framework below expands on that foundation. It targets six operational risk zones where double financing threats truly exist.

Read What Data Must Banks Verify Before Tokenizing Accounts Receivable? for the full origination verification checklist that feeds into the controls below.

Double Financing Risk Control Map

Risk | Control | Evidence Needed | Block or Flag Action |

Duplicate invoice | Hash and ERP matching | Invoice number, debtor, amount, due date | Block minting |

False debtor approval | Digital debtor confirmation | Signed acknowledgment | Reject request |

Duplicate pledge | Pledge registry | Current pledge status | Stop second pledge |

Payment drift | Payment reconciliation | Bank or payment event | Mark settled |

Invoice cancellation | Versioning and alerts | Amendment record | Freeze or review token |

Undisclosed assignment | Legal and registry checks | Seller declaration, security filing | Exclude invoice |

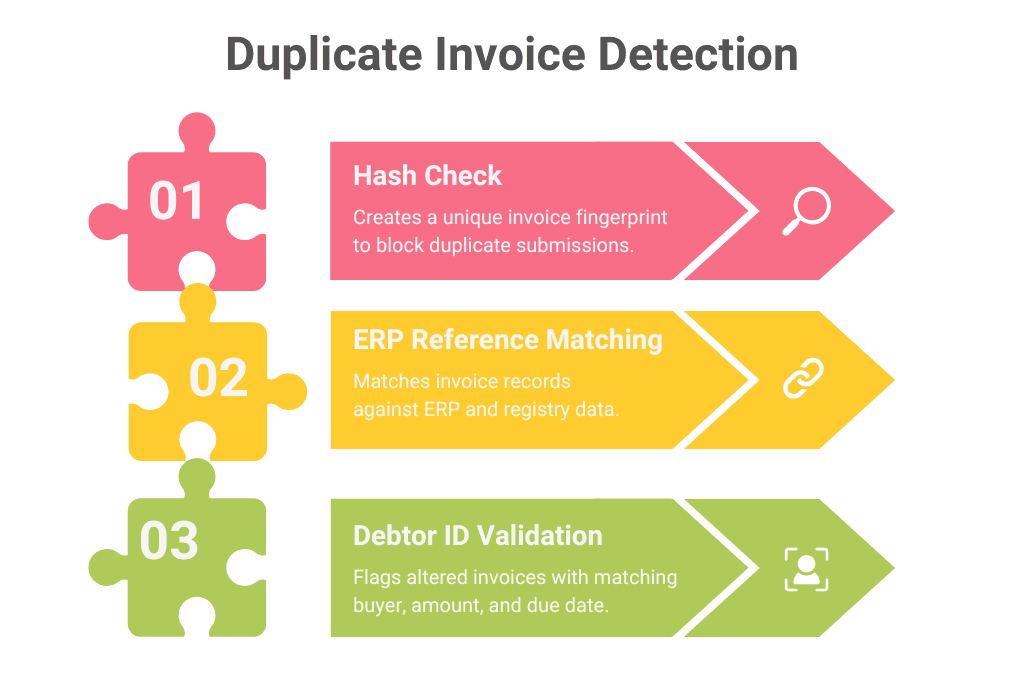

Control 1: Duplicate Invoice Detection

The first line of defense is uniqueness verification at the point of origination. Before any token can be minted, the bank needs to ensure that the invoice is not already registered, pledged or financed elsewhere.

There are three mechanisms to facilitate this check.

Hash-based uniqueness. A digital fingerprint is generated from the invoice number, buyer, seller, amount and due date. This unique code helps in detecting fraud immediately. If someone tries to submit the same invoice twice, the system detects it. Banks should store this code on day one and block any matching files that come up later.

ERP reference matching. Verification systems match unique ERP numbers to a central database. Banks using ERP data can match these reference codes against past entries. This step lets them block new uploads before a duplicate gets through.

Debtor ID validation. Combining the invoice amount, due date, and buyer ID creates a backup safety check. If two invoices from the same seller share the exact same buyer, invoice amount, and due date, they are high-risk duplicates. Even if the numbers on the invoices are different.

Control 2: Debtor Confirmation

The second control point is debtor confirmation. Use of forged or undisclosed debtor acknowledgment is a common practice in fraudulent financing schemes. Banks must treat confirmation as an active step of verification, not simply a matter of form.

Three elements support confirmation integrity.

Cryptographic acknowledgement. The debtor signs the confirmation with either a private key or a verified digital identity. This generates a timestamped, tamper-evident record that becomes harder to alter after signing. The confirmation record is stored as part of the token metadata.

Multi-party attestation. The debtor needs to approve invoices for higher amounts from multiple sources. To avoid fraud, the debt must be verified and approved by both the accounting department and a treasury officer, which makes it harder to fake approval.

Timestamped consent. The confirmation timestamp is logged at the moment of signing, not at the moment of submission. Any gap between the two is flagged for review. This prevents backdated confirmations that might be used to support a duplicate pledge.

Invoices without debtor verification must be stopped. If the confirmation lacks a valid digital signature, the bank must promptly reject the tokenization request. The debtor’s acknowledgment is the primary evidence of the underlying obligation’s existence.

Banks should reject or escalate confirmations when:

The approval comes from an unverified email address.

The debtor entity name differs from the contract.

The signer lacks approval authority.

The confirmation timestamp appears backdated.

The invoice lacks purchase order or delivery evidence.

The debtor approval only comes through the seller.

Control 3: Pledge Registry Design

A pledge registry is the single source of truth for which receivables have been tokenized and to which lender they are currently pledged. Without a registry, two lenders may hold competing invoice claims.

Effective registry design requires three properties.

Status locking. Once an invoice is registered and pledged, the registry locks its status. If someone else tries to register the same invoice it causes a conflict. The lender attempting the second registration is notified and the token cannot be minted until the conflict is resolved.

Event sequencing. All status updates are ordered in a strict sequence of registration, pledge, funding, payment and release. This timeline becomes tamper-evident. It prevents fraud on past collateral records and gives auditors a clear chain of custody.

Cross-platform visibility. A registry that only covers one platform doesn’t solve the problem. Shared registries provide the strongest protection against cross-platform duplicates. Without these shared networks, banks must sign two-way data deals with rival lenders. This is a practical way to track and block invoices that have already been funded elsewhere.

Shared registries should not expose full invoice data to every participant. Banks can use hashed invoice identifiers, permissioned access, and selective disclosure. This allows duplicate checks without revealing sensitive commercial terms.

The registry isn’t a replacement for legal formality. Listing a pledge on a token platform doesn’t make it legally safe overnight. Banks still have to go through the legal steps to secure their rights in each country where they do business.

Control 4: Off-Chain Payment Reconciliation

The status of a token and the status of the real-world payment can diverge. A debtor may pay the seller directly rather than through the platform. The seller takes the payment and does not report it. The token remains an outstanding token while the underlying obligation is settled.

And this status drift has two dangers. First, a lender may continue holding a collateral position against a receivable that no longer exists. Second, a seller acting in bad faith may use the unreported payment as an opportunity to re-pledge the already-settled invoice.

Three mechanisms address this:

Webhook triggers. The token status is automatically updated through payment events from the debtor’s bank or payment platform. When payment is confirmed, the token status changes from outstanding to settled and the pledge is flagged for release review. Payment updates should come from the debtor bank, payment processor, or buyer-approved system. Seller-only ERP data should not be the only reconciliation source.

Payment status sync. Banks must regularly check the token registry against the seller’s ERP system. If the token says a invoice is unpaid but the ERP system shows the payment was received, teams must look into the mistake right away.

Release automation. Once payment is confirmed and reconciled, the pledge release is initiated automatically. Manual release processes cause delays which extend the window for fraud. Automated release tied to confirmed payment events reduces that window.

Reconciliation Mechanism | Risk It Addresses |

Webhook triggers | Unreported direct payment from debtor |

Payment status sync | Ledger discrepancy between token and ERP |

Release automation | Manual delay creating re-pledge window |

Control 5: Cancel and Modify Invoices

Invoices are not immutable. A vendor may cancel an invoice, send a credit note or change the price after a token has been issued. Without strict rules, the digital token will still reflect the old terms. It no longer matches the actual obligation.

Versioning. When an invoice is changed, a new version record is created. The old version is archived, not deleted. The token shows the latest version and refers to the full history of amendments. This will mean the bank cannot take collateral on old terms.

Audit trail. Any cancellation or amendment is recorded with a timestamp, the identity of the party making the change and the reason code. The audit trail should be tamper-evident. If a cancellation is disputed, the record shows the exact time it was initiated and by whom.

Counterparty notification. When an invoice is canceled or changed, the bank and the buyer get an instant alert. This stops a seller from cancelling a pledged invoice without notice and taking the original paperwork to a different lender for a second financing facility.

Control 6: Undisclosed Assignment Prevention

The final control covers prior or undisclosed assignment. A seller may have already assigned the receivable to another creditor under a separate agreement, without disclosing this to the bank at origination.

Three steps address this.

First, the bank requires a seller declaration at origination that there is no prior assignment, pledge or encumbrance attaching to the receivable. This declaration is recorded as part of the token metadata.

Second, the bank checks any available creditor registry or public security interest filing system for prior claims against the seller's receivables. Coverage varies by jurisdiction, but the check should be performed where data is available.

Third, the token metadata includes an assignment restriction flag. If the underlying contract contains an anti-assignment clause, the flag is set at origination and the invoice is excluded from the eligible collateral pool until legal counsel confirms the restriction can be waived or overridden.

Control Architecture: What a Bank Implementation Looks Like

Combining these six defenses creates a layered system where each step catches whatever slips past the previous one:

Layer | Control | Failure Mode Addressed |

Origination | Hash-based uniqueness, ERP reference match | Duplicate invoice submission |

Confirmation | Cryptographic debtor acknowledgment | Forged or undisclosed consent |

Registration | Pledge registry with status locking | Competing claims from multiple lenders |

Lifecycle | Off-chain payment reconciliation | Status drift between token and real-world payment |

Amendment | Versioning and counterparty notification | Post-tokenization invoice manipulation |

Legal assignment | Seller declaration, registry checks, assignment flags | Prior assignment or enforceability conflict |

No single control is sufficient on its own. A strong duplicate detection system does not help if debtor confirmation can be forged. A robust registry does not help if payment status is never reconciled. The architecture works because each layer addresses a distinct failure mode.

Design an Invoice Fraud-Control Sprint With TokenMinds

Tokenized receivables need more than token issuance. Banks need controls for duplicate invoices, debtor confirmation, pledge status, payment reconciliation, and legal assignment checks.

TokenMinds helps finance teams map these risks into a practical control design before pilot deployment.

Book an invoice fraud-control sprint with TokenMinds. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: Does tokenizing an invoice automatically prevent it from being financed elsewhere?

A: No. Tokenization records a claim on one platform. It does not prevent another platform from minting a separate token for the same invoice. Prevention requires a shared registry that both platforms query before minting. Without that registry, duplicate tokens are possible and the bank holding the second token may have no collateral.

Q: What is the most common double financing pattern banks should watch for?

A: The most common pattern is a seller submitting the same invoice to two different receivables finance platforms simultaneously, particularly where the platforms do not share a registry or data feed. The seller receives two advances against one payment. If the debtor pays, only one lender will be paid.

Q: In practice, how is the off-chain reconciliation of payments done?

A: The bank or platform subscribes to payment event data from the debtor bank, payment processor, or buyer-approved system. Seller ERP data can support reconciliation, but it should not be the only trigger. Once payment matches the invoice amount, currency, and reference, the token status updates. The lender receives notice, and the pledge release process begins.

References

Chainlink: "Invoice Tokenization in Trade Finance." Identifies invoice authenticity and debtor credit verification as core pre-tokenization requirements. https://chain.link/article/invoice-tokenization-trade-finance