TL;DR: Customers pay USDC. Merchants receive fiat. The PSP orchestrates the payment flow. A regulated settlement-services provider handles custody, conversion, and on-chain settlement. No merchant-controlled wallet or private-key management. No direct PSP custody of crypto assets. Exact licensing, custody, and refund treatment depend on jurisdiction, contractual role, and fund flow.

How Can a PSP Offer Stablecoin Payments Without Holding Crypto?

This model is gaining traction because it removes crypto exposure from the merchant while preserving standard fiat settlement workflows. A customer pays in USDC at checkout. A regulated settlement-services or liquidity provider receives the stablecoin, converts it to fiat, and handles on-chain custody. The PSP orchestrates routing, reconciliation, and merchant reporting, but never takes direct control of private keys or digital assets. Merchants see only a fiat sale on their ledger. Contracts, accounting, and payout schedules can often remain unchanged, subject to merchant terms, disclosures, and jurisdictional review.

The complexity sits entirely in the infrastructure layer: FX rate locking, conversion custody, settlement pass-through, and proof of execution. That's the layer this guide breaks down.

What Makes the Model Non-Custodial?

The non-custodial structure separates payment orchestration from asset custody. The PSP acts as the instruction layer, not the balance layer. Key architectural boundaries:

The PSP never controls private keys or signs on-chain transactions.

A regulated liquidity provider temporarily holds stablecoins during the conversion window.

The merchant receives fiat only; crypto exposure is fully absorbed upstream.

Settlement and reporting pipelines remain fiat-native, preserving existing accounting workflows.

Model | PSP Holds Crypto? | Custody Exposure | Licensing Burden |

PSP-managed orchestration | No | Low (instruction routing only) | Payment/e-money framework may apply; crypto-asset classification depends on jurisdiction and fund flow |

Direct custody | Yes | High (balance sheet + key risk) | Full VASP/crypto custodian license |

Stablecoin treasury model | Yes | Full (price + counterparty risk) | Banking/VASP + reserve audit requirements |

Does This Require a Crypto License?

In most jurisdictions, a non-custodial PSP model may reduce direct crypto-custody licensing exposure, but classification depends on jurisdiction, contractual role, fund flow, and who controls the wallet or private keys. Because the PSP does not directly hold customer crypto assets or manage private keys, regulatory classification typically falls under standard e-money or payment institution frameworks. Compliance shifts from asset custody to transaction screening: AML/KYC controls are often delegated to the infrastructure provider for on-chain address screening, while the PSP retains responsibility for merchant onboarding, fiat AML checks, and Travel Rule data routing.

Many PSPs prefer this infrastructure-partner model because it preserves regulatory perimeter clarity, avoids reserve-audit requirements, and accelerates time-to-market.

The Setup: Customers Pay Crypto, Merchants See Fiat

This is the model gaining traction fast. A customer pays in USDC at checkout. The merchant receives local currency. The acquirer or PSP handles everything in between.

No merchant-controlled wallet or private-key management. No crypto exposure. No change to settlement reporting.

The complexity sits in the infrastructure layer: conversion, routing, FX locking, and proof of settlement. That's the layer this article addresses.

How Stablecoin Checkout Actually Works for Merchants

The checkout flow is simpler than most operators expect. Here's a $500 USDC transaction from initiation to merchant credit:

Operational Scenario: $500 USDC Purchase

Step | Layer | Actor | Action |

1 | Checkout | Consumer | Selects "Pay with USDC" at POS or ecommerce |

2 | Payment Request | PSP/Gateway | Generates stablecoin payment address + amount + expiry |

3 | Broadcast | Consumer wallet | Signs and submits on-chain transaction |

4 | Confirmation | Chain + PSP | Block confirmation detected (1–3 seconds on L2, ~15s on mainnet) |

5 | Conversion | Liquidity provider | USDC → USD at locked rate; slippage within defined tolerance |

6 | Settlement | Acquirer/PSP | Fiat credited to merchant account on standard T+1 or T+0 schedule |

7 | Reporting | Merchant dashboard | Transaction appears as fiat sale; no crypto line item |

The merchant sees a $500 USD sale. That's the design goal.

What Happens to Fiat Settlement When Crypto Is Involved?

Nothing changes — if the integration is built correctly.

Fiat settlement integrity depends on three things:

FX rate locking at payment initiation, not confirmation

Conversion custody: who holds the stablecoin during the conversion window

Settlement pass-through: how the acquirer credits the merchant account post-conversion

Stripe's stablecoin payment terms explicitly define the conversion timing and rate methodology, with merchants receiving local currency subject to supported-stablecoin terms, depeg-event rules, and the settlement provider's rate methodology. BVNK's enterprise infrastructure handles the full conversion-to-fiat pipeline at the institutional layer, decoupling the merchant from direct crypto operations.

The acquirer's obligation is unchanged. They owe the merchant fiat on a defined schedule.

Sample Acceptance Criteria for Production Readiness

To validate vendor fit and system performance, track these illustrative vendor evaluation thresholds before go-live:

Conversion Latency: Median 1.5–3 seconds from on-chain confirmation to fiat rate lock.

FX Slippage Tolerance: ≤0.15% deviation from quoted rate during peak volatility.

Treasury Buffer Sizing: 15–20% prefunding reserve per corridor to absorb settlement timing mismatches.

Reconciliation Error Tolerance: <0.05% mismatch rate between on-chain confirmations and GL entries.

Settlement SLA: 99.5% of fiat credits posted within agreed T+1/T+0 windows.

Merchant Acceptance Models: A Direct Comparison

Not all acceptance architectures are equivalent. The model you choose determines who owns conversion risk, how chargebacks work, and what your settlement SLA looks like.

Model | Who Converts | Merchant Exposure | Settlement Format | Chargeback Path |

PSP-Managed Conversion | PSP / Acquirer | None (fiat only) | Standard fiat T+1 | Fiat-layer refund and exception workflow; no native on-chain reversal or card-network-style dispute unless separately provided by the PSP. |

Gateway + Third-Party Liquidity | Third-party LP via gateway | Low (rate lock risk) | Fiat, post-LP settlement | LP-dependent; SLA varies |

Direct On-Chain + Manual FX | Merchant or treasury desk | High (FX + custody) | Crypto or manual fiat | No standard path |

Stablecoin-Native Settlement | None (merchant holds USDC) | Full (price stability) | Stablecoin only | Smart contract logic |

For merchant-facing acquirers: the PSP-Managed Conversion model is the only architecture that preserves your existing merchant contract terms without renegotiation. see [CM-28: Crypto Payment Gateway vs Stablecoin Payment API vs On/Off-Ramp] https://tokenminds.co/blog/crypto-payment-gateway-vs-stablecoin-api-vs-on-off-ramp

PSP vs. Direct Integration: Decision Framework

Use this to align your architecture decision with organizational risk appetite.

Go PSP-managed if:

Your merchant contracts specify fiat settlement

Your ops team has no crypto treasury infrastructure

You need PSP-defined fiat refund, credit, and exception workflows without native on-chain reversal

Regulatory classification of crypto custody is ambiguous in your jurisdiction

Go direct integration if:

You serve merchants with stablecoin treasury demand (e.g., cross-border, remittance-adjacent)

You have in-house blockchain engineering capacity

Your acquiring license permits custodial stablecoin handling

You want to offer settlement optionality as a product differentiator

Most banks and mid-market PSPs land in the first category. That's not a limitation—it's the correct fit for the operational model.

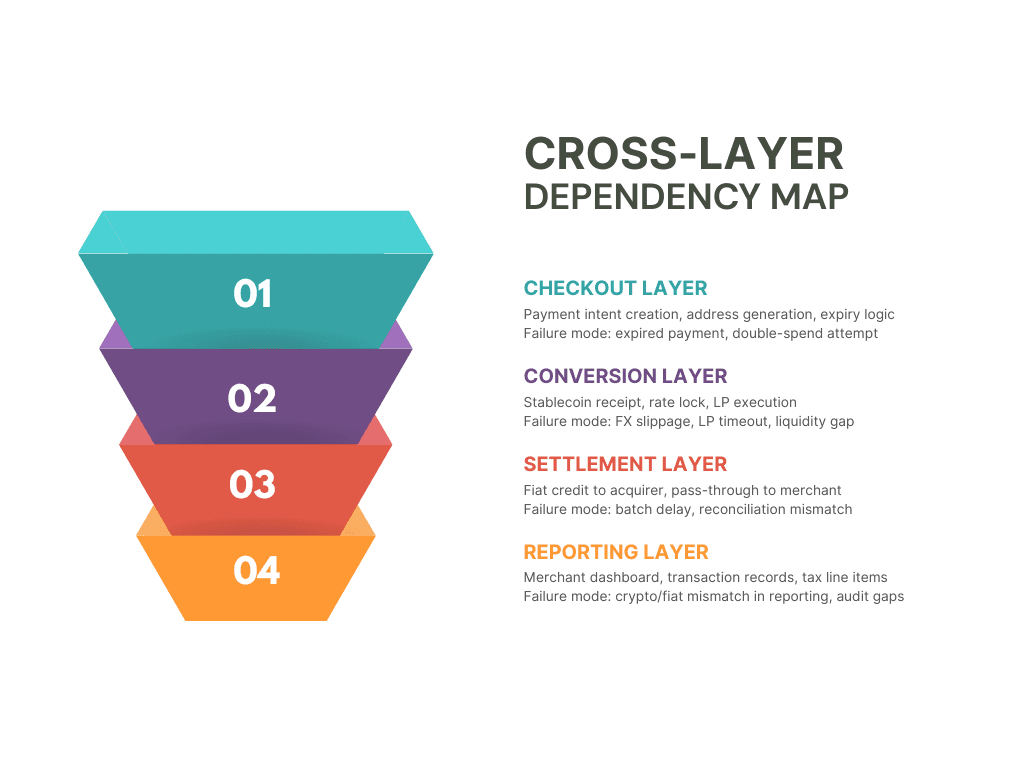

Cross-Layer Dependency Map

Every stablecoin acceptance deployment has four operational layers. A failure at any layer creates a downstream problem.

Map your vendor against each layer. Know who owns the failure.

Failure Mode Table: What Goes Wrong and Who Owns It

Failure Mode | Trigger | Owner | Merchant Impact | Mitigation |

Conversion delay | LP liquidity gap at peak volume | Liquidity provider | Delayed fiat credit | Pre-funded LP pool; SLA floor |

FX slippage beyond tolerance | Rate movement between lock and execution | PSP / LP agreement | Under-settlement | Rate lock window ≤ 30 seconds |

Block confirmation timeout | Network congestion (mainnet Ethereum) | Protocol | Payment stuck, customer not charged | L2 routing (Base, Polygon) as default |

Settlement mismatch | Batch conversion error | Acquirer / PSP | Merchant reconciliation error | Per-transaction conversion audit log |

Reporting format error | Crypto txn not mapped to fiat SKU | Integration layer | Tax/accounting discrepancy | Fiat-only reporting pipeline; suppress on-chain data |

Refund failure | No fiat reversal path post-conversion | PSP | Merchant dispute, customer churn | Pre-defined fiat refund reserve; no on-chain reversal |

Refunds are the most-underestimated failure point. Once USDC is converted to fiat, there's no on-chain reversal. Your refund logic must sit entirely in the fiat layer.

Risk and Ownership Matrix: PSP, Acquirer, and Merchant

Risk Category | PSP | Acquirer | Merchant |

Stablecoin custody risk | Settlement-services provider owns custody risk; PSP owns vendor oversight, SLA enforcement, and merchant-facing reporting | Shared | None |

FX conversion risk | Liquidity provider / settlement provider primary; PSP owns SLA and merchant-facing pricing logic | Shared (rate SLA) | None |

Settlement timing risk | PSP/acquirer primary; provider dependency through conversion and payout rails | ✓ Owns | Low (SLA-bound) |

Refund/dispute handling | PSP/acquirer policy layer; no automatic on-chain reversal | ✓ Owns | Standard liability |

Compliance / AML screening | PSP owns merchant onboarding; provider owns wallet/on-chain screening where delegated | Shared | None |

Reporting accuracy | PSP/acquirer owns merchant-facing records; merchant owns tax treatment | Shared | ✓ Owns (tax) |

On-chain audit trail | ✓ Owns | None | Optional |

Merchants carry almost no new risk in a properly structured PSP-managed model. That's the pitch—and it's accurate.

Reconciliation and Exception Handling Workflow

Production stability depends on documented escalation paths, not just happy-path flows. Use this decision tree for exception resolution:

Payment Confirmation > 90 Seconds: PSP triggers PENDING_RECONCILIATION state → Liquidity provider maintains hedge reservation for 5 minutes → Customer UI disables retry → Automated alert to treasury ops.

Underpayment/Overpayment (>2% variance): System flags AMOUNT_MISMATCH → Auto-hold fiat settlement → Route to merchant service queue → If customer does not respond within 24 hours, auto-refund or apply credit per merchant policy.

FX Rate Lock Expired Before Signing: Orchestrator triggers QUOTE_EXPIRED → Customer prompted to re-confirm at new rate → If retry fails, transaction voided → No fiat exposure incurred.

Settlement Batch Reconciliation Break: Daily GL vs. on-chain audit shows mismatch → Trace to specific webhook ID → If duplicate, auto-reverse GL entry → If missing, trigger manual LP settlement request → Log incident for vendor SLA review.

Stablecoin payments should not be described as having conventional chargebacks by default. Once the stablecoin transaction is submitted, there is typically no on-chain reversal. Refunds and disputes must be handled through a PSP-defined fiat refund, credit, or exception workflow.

This is where most integrations break down in production. The checkout-to-settlement flow is straightforward. Exceptions are not.

For the full operational playbook covering partial payments, overpayment routing, and escalation paths, see [CM-33: Reconciliation, Refunds, and Exception Handling for Crypto Payment Integrations].

If your integration vendor doesn't have documented answers to each of these, that's a qualification failure—not a product gap to solve later.

How This Compares to Crypto Gateway and On/Off-Ramp Models

Stablecoin acceptance is one part of a broader acceptance architecture decision. If you're evaluating where it fits relative to full crypto gateway deployment or fiat on/off-ramp infrastructure, see Crypto Payment Gateway vs Stablecoin Payment API vs On/Off-Ramp.

The short version: stablecoin acceptance is the lowest-friction entry point for acquirers. It requires no crypto settlement infrastructure, may reduce direct custody-licensing exposure depending on jurisdiction, fund flow, contractual role, and provider structure, and typically requires no change to merchant-facing product terms.

Settlement Proof and Audit Requirements

One operational advantage of stablecoin acceptance that traditional card rails don't offer: every conversion is provable.

A well-structured integration captures:

On-chain transaction hash at payment receipt

Conversion execution record (amount in, rate applied, amount out)

Settlement confirmation linked to transaction ID

Timestamp chain from checkout initiation to fiat credit

This creates an immutable audit trail for every merchant transaction. A PSP should require API-accessible transaction hashes, conversion records, and fiat settlement confirmations to surface settlement proof directly in merchant dashboards without building proprietary blockchain indexing. Dispute resolution becomes evidence-based, not assertion-based. Compliance, finance, and risk teams increasingly ask for this.

What to Do Next

Stablecoin acceptance is live infrastructure now. Stripe has documented commercial terms. BVNK is running enterprise-grade conversion pipelines. The integration patterns are proven.

The remaining question is fit: does your current acquiring stack support this cleanly, or does it require middleware, licensing review, or settlement infrastructure changes?

That depends on your specific architecture—and it's worth mapping before you commit to a vendor.

Request a merchant acquiring integration assessment.

Frequently Asked Questions:

Q: Does stablecoin acceptance require merchants to hold crypto?

No. In a PSP-managed model, the merchant never holds or sees crypto. They receive fiat settlement on their existing schedule. Crypto handling sits entirely within the settlement provider or acquiring infrastructure.

Q: How is FX risk managed in stablecoin-to-fiat conversion?

Rate risk is managed through rate locking at payment initiation — typically a 15–30 second window. The PSP or liquidity provider absorbs any slippage beyond the locked rate, subject to contract and SLA terms. Merchants receive the locked fiat equivalent, subject to supported-stablecoin terms and depeg-event rules.

Q: Can existing merchant contracts support stablecoin acceptance without renegotiation?

In most cases, yes. Because merchants receive fiat settlement and see only fiat transaction records, their existing contracts typically remain valid. Contract amendments are only needed if:

• Merchants request stablecoin settlement optionality, or

• Local jurisdictional rules require specific crypto-payment disclosures.

Q: What's the difference between stablecoin acceptance and crypto payment acceptance?

Stablecoin acceptance uses price-stable assets (USDC, USDT) pegged to fiat. Volatility risk is lower but carries non-zero depeg and network risk. Conversion is near-instantaneous, subject to blockchain confirmation times. Most acquirers should start with stablecoin-only acceptance.

References:

Stripe: Stablecoin Payments Terms. Source for stablecoin payment acceptance and settlement services model. https://stripe.com/legal/stablecoin-payments

BVNK: Enterprise Stablecoin Payments Infrastructure. Source for full-stack product taxonomy: accept, send, wallets, orchestration, managed and self-managed payment models. https://bvnk.com/