TL;DR

Tokenized deposits generally suit domestic, bank-controlled settlement. Regulated stablecoins can extend cross-border reach but add issuer, redemption, custody, and reconciliation dependencies. Wholesale central bank money offers sovereign settlement within approved programs. Banks should compare legal discharge, liquidity, network reach, programmability, and collateral-release controls before choosing a model.

Three Settlement Assets for Banks to Know

The IMF discusses three different settlement asset types. Each has different risks and operational requirements.

Tokenized deposits: Digital versions of standard commercial bank deposits. They are a direct bank liability. Deposit insurance applies where local regulation permits. They run on private, bank-controlled ledger systems.

Stablecoins: Fiat-collateralized stablecoins are tokens backed by reserves of fiat currency. Each token represents a redemption claim against the issuer, supported by reserve assets, with redemption depending on the issuer’s liquidity position and operational capacity. This article focuses specifically on regulated fiat-backed payment stablecoins intended for settlement, issued by authorized banks or nonbank entities under jurisdiction-specific frameworks. Algorithmic, crypto-collateralized, and other asset-referenced tokens fall outside this comparison.

Wholesale Central Bank Money: Digital money issued directly by a central bank. It represents a direct claim on the central bank. HKMA EnsembleTX and BIS Project Agorá explore how tokenized commercial bank deposits can interact with central bank settlement infrastructure. Neither represents a standalone wholesale CBDC deployment.

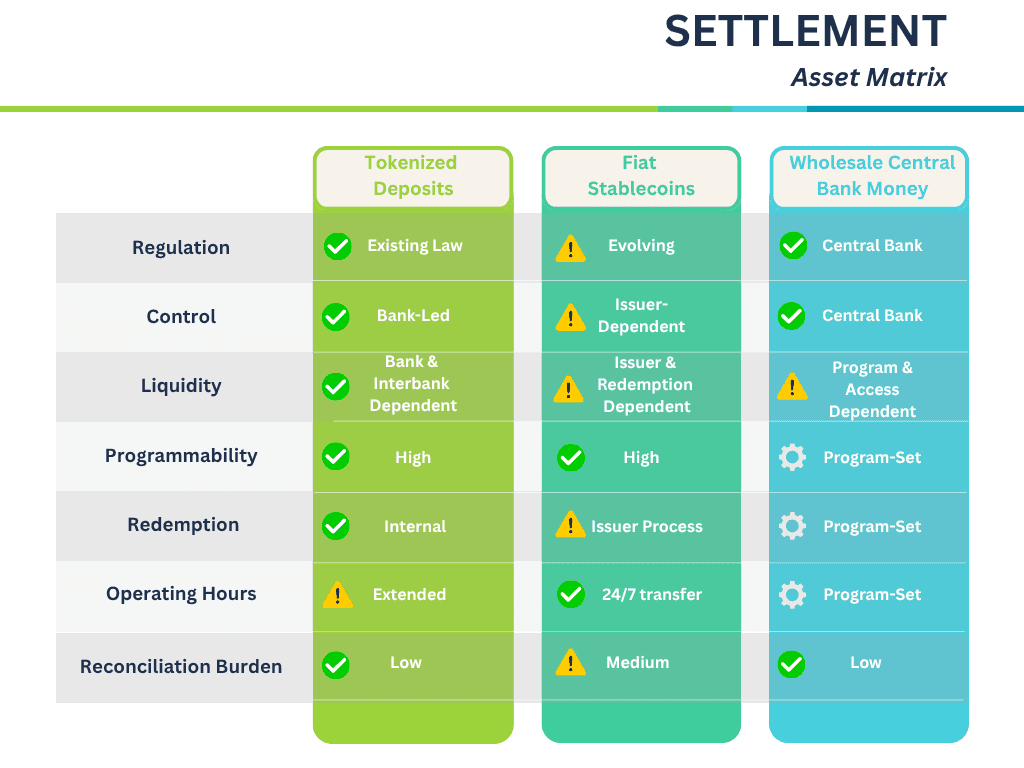

Master Comparison Table

Dimension | Tokenized Deposit | Fiat-Backed Stablecoin | Wholesale CBDC |

Issuer | Commercial bank | Authorized bank or nonbank issuer, depending on jurisdiction | Central bank |

Regulatory framework | Existing banking law | Varies by jurisdiction | Central bank program |

Deposit insurance | Applicable where permitted by jurisdiction | None | Not applicable |

Legal form and claim | Deposit claim on commercial bank | Redemption claim against issuer, supported by reserves | Direct claim on central bank; accounting treatment requires specialist validation |

Liquidity profile | Bank and interbank liquidity dependent | Reserve and redemption dependent | Program and central bank access dependent |

Settlement speed | Immediate on own system | Depends on issuer and network | Program-defined or near-real-time |

Automation support | High on private ledger | High; network-dependent | Program-defined |

Operating hours | Potentially extended or continuous, subject to infrastructure | 24/7 transfer; redemption hours vary | Program-defined |

Reconciliation burden | Low (internal) | Medium (bridge layer needed) | Low where available |

Audit trail quality | Full internal record | Bridge layer required | Authoritative central bank settlement record; collateral linkage remains program-specific. |

Regulatory Fit

Tokenized deposits fall within existing banking regulation. However, licensing, capital, and liquidity requirements depend on jurisdiction and product structure.

For fiat-backed stablecoins, the bank needs to determine the legal status of the issuer. The EU's MiCA framework applies to stablecoin issuers there. Singapore has finalized the design of its single-currency stablecoin framework. Licensing and implementation requirements depend on the applicable legislation, issuer structure, and regulated payment activities. Banks should verify the current MAS requirements before launch. The United States established a federal payment stablecoin framework under the GENIUS Act in 2025. Detailed capital, liquidity, licensing, custody, and compliance requirements remain subject to implementing regulations.

Wholesale central bank money has the clearest sovereign issuer status where an approved program is available. Access is restricted to licensed institutions in approved programs.

How Settlement Assets Affect the Receivables Collateral Lifecycle

Settlement asset choice affects five stages of the collateral lifecycle.

Pledge created. Settlement asset choice has no direct effect here. Pledge registration is independent of the funding method.

Advance funding. With tokenized deposits, the advance is an internal transfer. With stablecoins, the bank must source or issue them first. This may add time to the funding cycle depending on issuer processes and network conditions.

Debtor pays. With tokenized deposits, payment receipt and the accounting entry happen together. With stablecoins, the bank must determine whether stablecoin receipt constitutes repayment or whether redemption into bank money is required before recognizing repayment.

Collateral released. Stablecoin receipt and stablecoin redemption should be treated as separate events. A bank may define verified stablecoin receipt as the repayment event or require redemption into bank money before releasing collateral. The correct approach depends on legal discharge terms, accounting policy, issuer risk, custody controls, and treasury requirements.

Audit record closed. With tokenized deposits, the full record sits in one system. With stablecoins, the audit record must capture receipt, network finality, compliance clearance, and any later redemption. If verified receipt is the contractual repayment event, the loan and collateral records may close at receipt while redemption remains a separate treasury event. If redemption is required for repayment, the records remain open until conversion into bank money.

Illustrative Settlement and Accounting Events

This accounting-event mapping is illustrative. Final recognition, derecognition, balance-sheet classification, liquidity treatment, and pledge-release entries depend on legal ownership, contractual discharge terms, applicable accounting standards, custody arrangements, and bank policy. Banking accounting specialists should review these entries before implementation.

Lifecycle Stage | Tokenized Deposit Entry | Fiat-Backed Stablecoin Entry |

Advance funded | Dr: Loans / Cr: Internal funding account | Dr: Loans / Cr: Stablecoin holding account |

Repayment received | Dr: Settlement account / Cr: Loans | Receipt-final model: recognize the stablecoin asset and loan repayment at verified receipt. Redemption-final model: record receipt in an approved holding or suspense account until conversion into bank money, then recognize repayment. |

Redemption confirmed | No additional entry needed | Dr: Bank account / Cr: Stablecoin holding account |

Holdback created | Dr: Escrow account / Cr: Internal funding | Dr: Escrow account / Cr: Stablecoin holding account |

Escrow released | Dr: Bank account / Cr: Escrow account | Dr: Bank account / Cr: Escrow account (post-redemption) |

Pledge released | Collateral and pledge records closed according to the approved contractual discharge and release policy. | Collateral and pledge records closed according to the approved contractual discharge and release policy. |

If verified stablecoin receipt is the contractual repayment event, the loan may be derecognized at receipt while the bank records a separate stablecoin asset until redemption. If the bank requires conversion into bank money before recognizing repayment, the loan remains outstanding until redemption. The accounting entries and collateral-release rules must follow the selected model consistently.

Misclassifying the holdback entry also affects liquidity ratio calculations during the dispute period.

Insolvency and Resolution Scenarios

Stablecoin issuer enters resolution. If the issuer enters resolution after receipt, the effect depends on the selected settlement model. Where receipt has already discharged the loan, the bank may retain a separate impaired stablecoin asset. Where redemption is required before repayment recognition, the loan and collateral records remain open until the position is resolved. Stablecoin holder protection depends on the jurisdiction and issuer structure.

Some regulatory frameworks provide reserve segregation, redemption rights, wind-down requirements, or priority claims. Banks must assess the selected issuer’s reserve custody, legal claim, redemption process, and insolvency waterfall before accepting its stablecoin for settlement. Banks should set a maximum waiting period before reclassifying the balance. Five to ten business days is an illustrative starting point; final limits should be approved by treasury, risk, legal, compliance, and operations teams based on the selected issuer, network, jurisdiction, and settlement model.

Banks issuing tokenized deposits enter resolution. Tokenized deposits may receive deposit protection where they remain legally equivalent to conventional deposits. Coverage depends on depositor eligibility, account structure, statutory limits, and local resolution law.

Debtor becomes insolvent while receivables are pledged. The lending agreement must define the legally effective settlement trigger. This may be verified receipt, network finality, compliance clearance, or redemption into bank money, depending on the selected operating model. Without this clause, an administrator may argue the advance is still outstanding. The bank needs this protection before the program goes live.

Collateral Agent and Release Timing Controls

In programs with multiple lenders, a collateral agent manages settlement on their behalf. Where a program accepts one stablecoin, participating lenders share exposure to that issuer and its redemption infrastructure. Multi-issuer programs introduce additional interoperability, valuation, compliance, and reconciliation requirements. The collateral agent should disclose issuer concentration and redemption dependencies to all participating lenders.

Banks should define risk-based release windows based on network finality, compliance clearance, operating hours, legal notice procedures, redemption requirements, and dispute risk. Two-to-four-hour domestic and 24-hour cross-border windows may be tested as illustrative pilot parameters. The waiting period must be adjustable without rebuilding the system. Because automated release may execute before a legal dispute notice reaches the system, the design should include configurable delays, manual holds, exception overrides, and dispute flags.

Decision Framework

Starting Condition | Recommended Settlement Asset |

Domestic program, own ledger system | Tokenized deposit |

Cross-border, no local deposit infrastructure | Compare regulated stablecoins and interoperable tokenized deposits. Stablecoins may lead where bank-deposit rails are unavailable. |

Multi-bank program, shared network | Compare interoperable tokenized deposits and regulated stablecoins based on network design, issuer model, interbank settlement, and liquidity access. |

Interbank settlement, central bank program available | Wholesale CBDC |

Stablecoin regulation unclear in operating market | Tokenized deposit as default |

Pilot-selection scoring

Score each settlement asset separately against these weighted factors. Each asset receives a score from 1 to 5 against each factor. The bank can then compare the weighted totals.

Evaluation Factor | Weight |

Legal and regulatory eligibility | 25% |

Settlement finality and legal discharge | 20% |

Liquidity and redemption capacity | 20% |

Counterparty and network reach | 15% |

Bank control and core-system integration | 10% |

Reconciliation and programmability | 10% |

Score each settlement asset from 1 to 5 for every factor:

1:poor fit or major unresolved dependency

3: conditional fit requiring additional controls

5: strong fit under the proposed operating model

Multiply each score by its weight and compare the total results. Legal and regulatory eligibility should remain a mandatory gate. An asset that is not legally eligible should be excluded regardless of its weighted score.

KPI | Tokenized Deposit Target | Stablecoin Target |

Collateral release time | Under 1 hour | Under 4 hours |

Reconciliation exception rate | Below 1% | Below 3% |

Settlement break rate | Below 0.5% | Below 2% |

Manual steps per 100 transactions | Under 1 | Under 5 |

*All numeric targets are illustrative pilot thresholds. Final limits should be approved by treasury, risk, legal, compliance, and operations teams based on the selected issuer, network, jurisdiction, and settlement model.

Wholesale CBDC targets are program-defined and are excluded from this KPI comparison until access, operating hours, and settlement rules are confirmed.

Read Central bank money vs tokenized deposits vs stablecoins for securities settlement for comparing digital settlement options.

Read Bank-grade crypto payments architecture: wallets, custody, liquidity, compliance, and core-banking integration for designing a secure and compliant crypto payments architecture

Assess the Right Settlement Model With TokenMinds

Banks should not select a settlement asset based only on transaction speed or network availability. The model must also support legal discharge, liquidity management, reconciliation, accounting, collateral release, and operational resilience.

TokenMinds helps banks compare tokenized deposits, regulated stablecoins, and central bank settlement options against their jurisdiction, ledger architecture, trade finance workflow, and risk requirements.

Request a tokenized settlement model assessment for your receivables collateral program. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: Should receivables settlement use stablecoins or tokenized deposits?

A: Tokenized deposits generally suit domestic, bank-controlled programs. Regulated stablecoins may suit cross-border programs without local deposit infrastructure. Interoperable tokenized deposits may also support shared bank networks. The scoring framework above helps determine the stronger fit.

Q: Are tokenized deposits safer than stablecoins for settlement?

A: Stablecoin holder protection depends on the issuer and jurisdiction. Some frameworks provide reserve safeguarding, redemption rights, wind-down requirements, or priority treatment. Banks should assess the selected issuer’s legal claim, reserve structure, and insolvency waterfall. Tokenized deposits may offer a clearer regulatory and accounting position when they remain legally equivalent to conventional bank deposits, though they still carry issuing-bank credit risk where balances are uninsured.

Q: What is the role of wholesale CBDC in terms of receivables settlement?

A: Wholesale central bank money removes commercial issuer credit risk because it represents a direct claim on the central bank. However, access, settlement finality, liquidity, operating hours, and system integration remain program-specific. Its practical limitation is that most banks can only use it through approved central bank initiatives.

Q: Do stablecoins provide final, irrevocable settlement?

A: Network finality does not by itself determine legal discharge. Banks must define whether verified receipt, compliance clearance, or redemption triggers repayment and pledge release. Accounting and reporting should follow the selected model.

Q: How do tokenized deposits affect the bank's balance sheet?

A: Prudential and liquidity treatment may follow conventional deposit rules where the token remains legally equivalent to a standard bank deposit. Final treatment depends on jurisdiction, product structure, and supervisory policy. No temporary holding account is created for standard internal transfers.

Q: Can you use stablecoins in multi-lender programs?

A: Where a program accepts one stablecoin, all lenders share exposure to that issuer. Multi-issuer models can reduce concentration but add interoperability, compliance, valuation, and reconciliation requirements. Banks should limit their exposure to any single stablecoin issuer. The 25%–30% concentration limit is illustrative; final limits should be approved based on issuer risk assessment, jurisdiction, and bank risk appetite. The collateral agent must disclose this concentration to all lenders before the program begins.

Q: How do tokenized deposits support trade finance settlement?

A: Tokenized deposits can connect loan funding, debtor repayment, reconciliation, and collateral release within a bank-controlled environment. Their value depends on whether the bank can integrate the ledger with trade finance systems, liquidity controls, and interbank settlement infrastructure.

References

IMF: "Tokenized Finance" (2026). Segregates tokenised deposits, stablecoins and wholesale CBDC into separate categories of settlement assets with different regulatory, liquidity and operational profiles.

BIS: Project Agorá. Explores tokenized bank deposits as programmable settlement instruments for cross-border payments.

HKMA: Project Ensemble. Demonstrates tokenized deposit and digital asset use cases with interbank settlement.

Uniform Commercial Code: Article 9 – Secured Transactions. Governs perfection and priority rules for security interests in accounts, payment intangibles, and other receivables under US law.

European Commission / EBA: Markets in Crypto-Assets (MiCA) Regulation. Provides framework for stablecoin issuance and redemption rights.

Monetary Authority of Singapore (MAS): Framework for Stablecoins. Sets out the framework for qualifying single-currency stablecoins.