TL;DR

Government bonds remain the most liquid collateral asset in institutional finance. Tokenizing them does not change the asset. It changes how custody, eligibility, settlement, and reconciliation operate. Operations teams need a structured evaluation framework before committing to a pilot. This article provides one.

Why Government Bonds Are the Logical First Use Case

Government bonds sit at the center of collateral management for a reason. They carry high credit quality. They offer deep liquidity. They meet eligibility standards across most counterparties and CCPs. When operations teams consider tokenized collateral, government bonds reduce the variable count. The asset class is known. The risk profile is known. The regulatory treatment is largely established.

The BIS 2025 Annual Economic Report reinforces this logic. The BIS frames tokenized central bank reserves, commercial bank money, and government bonds as core building blocks for wholesale tokenized finance. It also notes that tokenized government bonds could support collateral management and monetary policy operations.

For operations teams, this framing matters. It signals institutional-grade intent from central banks and multilateral bodies. It also clarifies the starting question. The question is not whether tokenized government bonds will enter collateral workflows. The question is whether an operations team is ready to check the mechanics.

Readiness depends on four areas: asset custody, rule coding, trade finality, and system checks. Teams must check each area before choosing vendors or getting risk approval.

What Operations Teams Should Evaluate First

Before selecting a platform or vendor, operations teams should confirm five foundational elements:

Custody model: Does the token show legal ownership or a claim?

Eligibility logic: Can haircuts, limits, and concentration rules be encoded?

Settlement finality: Does DvP use central bank money or another cash leg?

Reconciliation: Can token records match internal books in real time?

Exception handling: Can teams resolve outages, failed transfers, and mismatches?

These five questions form the baseline for any pilot scope. Teams that answer them early avoid costly redesigns later.

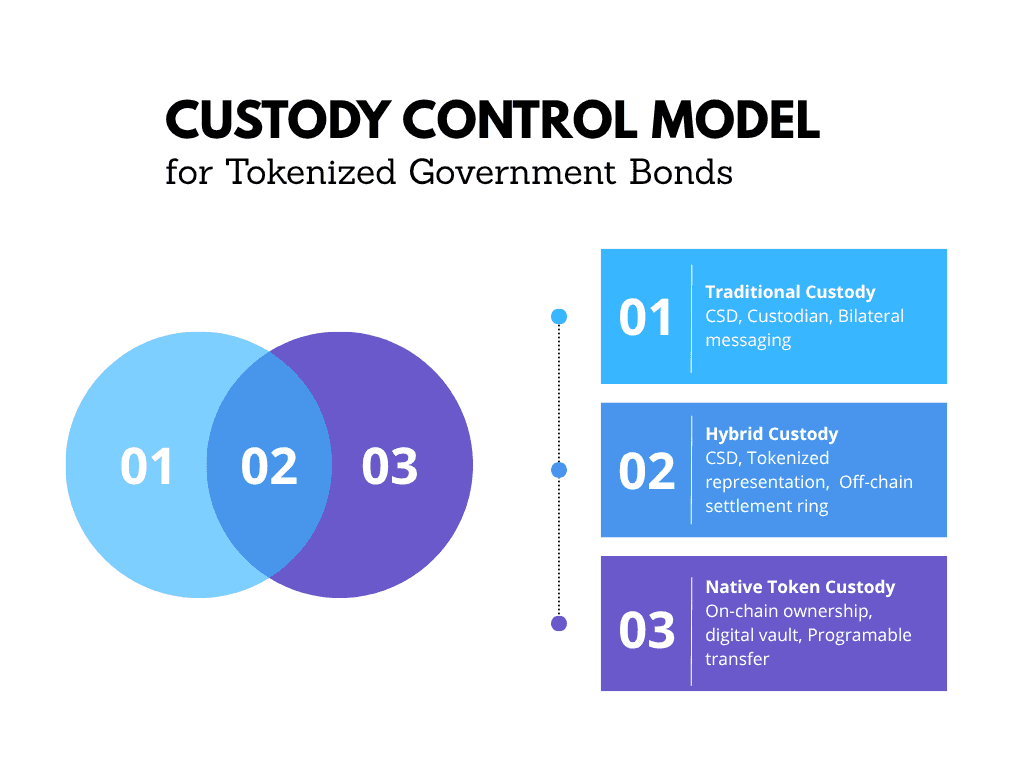

Operational Changes at the Custody Layer

Traditional government bond custody runs through a chain. A central securities depository holds the securities. A custodian holds them on behalf of a client. The client controls collateral positions through the custodian's internal systems and bilateral messaging. Each step adds latency. Each step adds counterparty dependency. Each step adds reconciliation overhead.

Tokenized government bonds shift this model. The token may represent direct legal ownership. It may also represent a claim on a bond held through a CSD or custodian. Operations teams must confirm the legal structure before treating token custody as equivalent to bond ownership. Custody control moves to the layer where the token is held. This may be a regulated digital asset custodian. It may be a bank-operated digital vault. It may be a shared DLT platform. Operations teams must check which custody model applies to their institution. They must check what controls govern it.

Custody Control Model Evaluation Matrix

Custody Model | Ownership Record | Transfer Mechanism | Key Operational Risk |

Traditional (CSD-based) | CSD register | SWIFT or bilateral messaging | Reconciliation lag, settlement fails |

Hybrid (tokenized representation) | CSD + token ledger | Off-chain link to on-chain token | Dual-record divergence, sync failures |

Native token custody | On-chain ledger | Programmable token transfer | Smart contract risk, key management |

Custodian-operated digital vault | Token ledger plus custodian records | Custodian-controlled transfer workflow | Key control risk, operational dependency, audit gaps |

Operations teams should confirm four things at the custody layer. First, who holds the private key, and what multi-person authorization governs transfers. Second, whether the custody provider carries a regulated status in the relevant jurisdiction. Third, how custody records sync with the institution's internal inventory system. Fourth, what the fallback procedure is if the token platform experiences an outage.

These are not technology questions. They are operational control questions. A well-configured custody layer answers all four before a pilot goes live.

Eligibility Encoding and Real-Time Rule Enforcement

Collateral eligibility in traditional operations relies on static rule sets. A risk team decides which securities to accept. They look at the asset type, its credit rating, haircuts, and total holding limits. Those rules live in a collateral management system. Operations staff apply them manually or through batch processing. Rule changes propagate slowly. Exceptions need human review.

Tokenized government bond platforms introduce programmable eligibility. Rules encode directly into smart contracts or eligibility engines. The platform evaluates collateral in real time against the current rule set. If a bond falls outside eligibility parameters, the platform can trigger a substitution workflow.

This creates a material operational shift. Teams must check whether their eligibility rules can translate into machine-readable logic. They must check whether that logic captures every nuance the risk committee requires.

Eligibility Rule Encoding Approaches

Encoding Approach | Rule Location | Update Mechanism | Auditability |

Static rule engine (traditional) | Collateral management system | Manual update by operations | Full, via system logs |

Platform-level smart contract | On-chain contract | Governance vote or admin key | Partial, depends on chain design |

Off-chain eligibility oracle | External rule engine, linked on-chain | API-driven update | High, with version control |

Hybrid encoded + human override | Smart contract + manual exception layer | Dual mechanism | High, with audit trail |

The hybrid model works best for operations teams right now. The hybrid model works best for many operations teams today. It preserves human oversight for exceptions while automating standard eligibility checks. It preserves human oversight for exceptions. It automates standard eligibility checks. Operations teams should confirm that the eligibility engine logs every rule evaluation. It should log every substitution trigger. It should log every override. Risk committees need that audit trail.

Check the specific economic gains from granular substitution in this workflow analysis: Tokenized Collateral Operational Gains in Securities Financing

Settlement Finality and Central Bank Money Interoperability

Settlement finality is the point at which a transfer becomes irrevocable. In traditional government bond markets, finality depends on the CSD and the RTGS system. A bond settles when the CSD confirms delivery. The central bank confirms cash payment. Traditional government bond settlement often depends on separate securities and cash settlement systems. Timing varies by market, but the workflow can still create sequencing, funding, and reconciliation dependencies.

Tokenized settlement aims to compress or cut that gap. Atomic settlement occurs when bond delivery and cash payment happen simultaneously and conditionally. This removes the window of counterparty exposure between leg one and leg two. This represents a material risk reduction for operations units. It helps control settlement risk during heavy intraday collateral cycles.

The BIS says digital central bank cash is key for large-scale networks. Digital government bonds perform best when they settle against official central bank funds. Using private stablecoins or tokens instead adds extra risk.

Settlement Finality Comparison

Settlement Model | Finality Point | Counterparty Exposure Window | Central Bank Money Used |

Traditional CSD/RTGS settlement | CSD confirmation + RTGS credit | Market-dependent | Yes, via RTGS |

DvP on private DLT | Smart contract execution | Compressed, if atomic DvP executes correctly | No, commercial bank token |

DvP with tokenized central bank reserves | Central bank token transfer | Compressed, if atomic DvP executes correctly | Yes, direct |

Hybrid settlement (on-chain bond, off-chain cash) | Sequential, not atomic | Hours to same day | Depends on cash leg |

Operations teams must classify the cash leg clearly. Tokenized commercial bank money, bank deposit tokens, stablecoins, and other private settlement assets carry different credit, legal, and liquidity risks. That risk may not appear in the institution's standard counterparty credit framework. It requires explicit risk committee classification before any pilot involves real collateral.

Review how distributed ledger rails can coexist with traditional central bank settlement infrastructure. How do you settle tokenized bonds in central bank money without replacing existing infrastructure?.

Interoperability Architecture Patterns

Institutional adoption requires flexible connectivity. A single ledger model rarely fits every custody or settlement requirement. Operations teams should evaluate four standard topology patterns.

Pattern 1: Synchronized Ledgers (Canton-style)

This pattern connects independent ledgers via shared messaging. Institutions keep their data to themselves. The network synchronizes settlement states. This reduces single point of failure risks. It allows banks to join without moving all data to a public chain. Operations teams favor this for cross-bank transactions where privacy remains critical.

Pattern 2: Permissioned Settlement Rails (Hyperledger Fabric)

Banks run the nodes in this framework. Governance rests with the participating consortium. Transactions process only with known counterparty permission. This system handles fast trade volumes and tight access controls. It works best for high-frequency asset moves between trusted banks. The IT team takes care of node health and regular certificate updates.

Pattern 3: CSD-Linked Token Mirrors

The Central Securities Depository acts as the source of truth. The digital mirror of the bond holding is created by the platform. Settlement is off-chain against the on-chain representation. This preserves the existing legal framework. This reduces regulatory friction for conservative institutions. Operations teams use this to transition slowly without abandoning legacy workflows.

Pattern 4: API-Mediated Hybrid Custody

This pattern links token platforms with traditional core banking systems. An API layer maps token movements to standard accounting entries. The internal ledger mirrors token status in real-time. Operations teams use this to bridge the gap between new tech and old reporting tools. This pattern minimizes the disruption to daily reconciliation routines.

Reconciliation Failure Modes and Playbooks

Continuous settlement creates new exception types. Old-style batch checks cannot keep up with real-time errors. Operations teams need to build new playbooks for digital workflows. These guides should show staff exactly how to fix common system breaks.

Reconciliation Exception Handling and Recovery Playbooks

Failure Scenario | Root Cause | Operational Playbook Action |

Orphaned Token Positions | Network partition or node failure isolates a token | Custodian initiates a reclaim request via the backup ledger. Platform operator freezes affected transfers. System logs the gap for audit. |

Delayed Oracle Synchronization | Price feed or data oracle lags behind the trading network | System pauses eligibility checks immediately. Manual override authorizes trades within safe limits. Teams verify data integrity before resuming. |

Off-Chain Inventory Mismatch | Internal core banking system updates slower than the token ledger | Operations halts outbound transfers. Reconciliation team runs a snapshot comparison. Finance team corrects the internal ledger entry. |

Failed Settlement Rollback | Smart contract logic fails to revert after a partial transaction | DevOps team isolates the transaction ID. The custodian executes a controlled settlement correction from the designated custody account. Risk team reviews the contract code. |

Smart Contract State Divergence | Different nodes disagree on the current asset eligibility status | Platform operator freezes affected transfers. Custodian, risk, and legal teams approve state correction. CSD or custodian records provide the fallback source of truth. |

Feasibility Checklist for Operations Teams

Tokenized Government Bond Collateral Feasibility Checklist

Evaluation Area | Key Question | Readiness Indicator |

Custody control | Who holds private keys and under what governance? | Regulated custodian, documented multi-person authorization |

Custody sync | How does token custody sync with internal inventory? | Real-time or scheduled API sync, reconciliation log |

Eligibility encoding | Can current eligibility rules translate to machine-readable logic? | Rules documented in structured format, gap analysis complete |

Eligibility auditability | Does the platform log every rule evaluation and substitution? | Full audit trail accessible to risk and compliance |

Settlement finality | Does the platform support atomic DvP? | Yes, with central bank money or approved cash equivalent |

Cash leg risk | What payment token settles the cash leg? | Central bank money or explicitly risk-classified alternative |

Reconciliation logic | How does the platform reconcile on-chain positions with internal books? | Automated reconciliation, break reporting, resolution workflow |

Interoperability readiness | Which architecture pattern fits the counterparty mix? | Topology selection approved by IT and operations. |

Exception handling | Are playbooks defined for token-specific failures? | Documented recovery procedures for all five scenarios. |

Legal ownership | Does the token represent legal ownership or a claim on ownership? | Legal opinion obtained, jurisdiction confirmed |

Regulatory classification | How does the relevant regulator classify the tokenized bond? | Regulatory guidance reviewed, internal legal sign-off |

Pilot scope | What is the minimum viable scope for a controlled pilot? | Defined counterparty set, asset subset, volume cap |

Completing this checklist early gives teams two big wins. They can bring firm requirements to vendor meetings instead of vague questions. They also give risk committees a clear blueprint to approve or tweak the project test.

Request a Tokenized Collateral Feasibility Memo

TokenMinds reviews custody models, eligibility rules, settlement options, reconciliation gaps, and pilot scope. The memo gives collateral and operations teams a clear readiness view before vendor selection or risk approval. Go to tokenminds.co to get a custom report for your team. https://tokenminds.co/contact/

Frequently Asked Questions

Q: What makes government bonds the best starting point for tokenized collateral?

A: They are high credit quality. They are highly liquid. They meet the eligibility standards set by most counterparties and CCPs. Tokenizing them isolates the operational variable. Teams evaluate how custody, settlement, and eligibility mechanics change. They do not also evaluate a new or unfamiliar asset class.

Q: Will the tokenization of a government bond change the legal ownership structure?

A: It depends on the jurisdiction and the design of the platform. Some platforms create a token that directly represents legal ownership. Others create a token that represents a claim on a bond held in a traditional CSD. Operations teams need a legal opinion specific to their jurisdiction. They need one specific to the platform structure. They need this before treating token custody as equivalent to direct legal ownership.

Q: What is the biggest operational risk in early tokenized bond collateral pilots?

A: The cash leg has a major hidden risk. Settling a digital bond with tokenized commercial bank money, bank deposit tokens, stablecoins, or another private settlement asset creates different credit, legal, and liquidity risks. Most current rules do not account for this exposure. Teams should clear this up with their risk committee before moving real collateral.

References

The BIS names three essentials for the next financial system: digital bonds, digital central bank cash, and digital bank money. These three elements drive future asset management and large trades. https://www.bis.org/publ/arpdf/ar2025e3.htm