TL;DR

Tokenized collateral does more than place assets on a blockchain. It restructures settlement timing. It automates eligibility screening. It significantly reduces bilateral reconciliation workload. Bilateral reconciliation drives operational costs in securities financing. Institutions map tokenization to specific workflow levers. Levers include speed of substitution, reduction of disputes and velocity of collateral. Institutions are able to measure gains from this mapping. The ROI argument depends on operational specificity. The ROI argument does not depend on vendor narratives.

The Operational Value of Tokenized Collateral

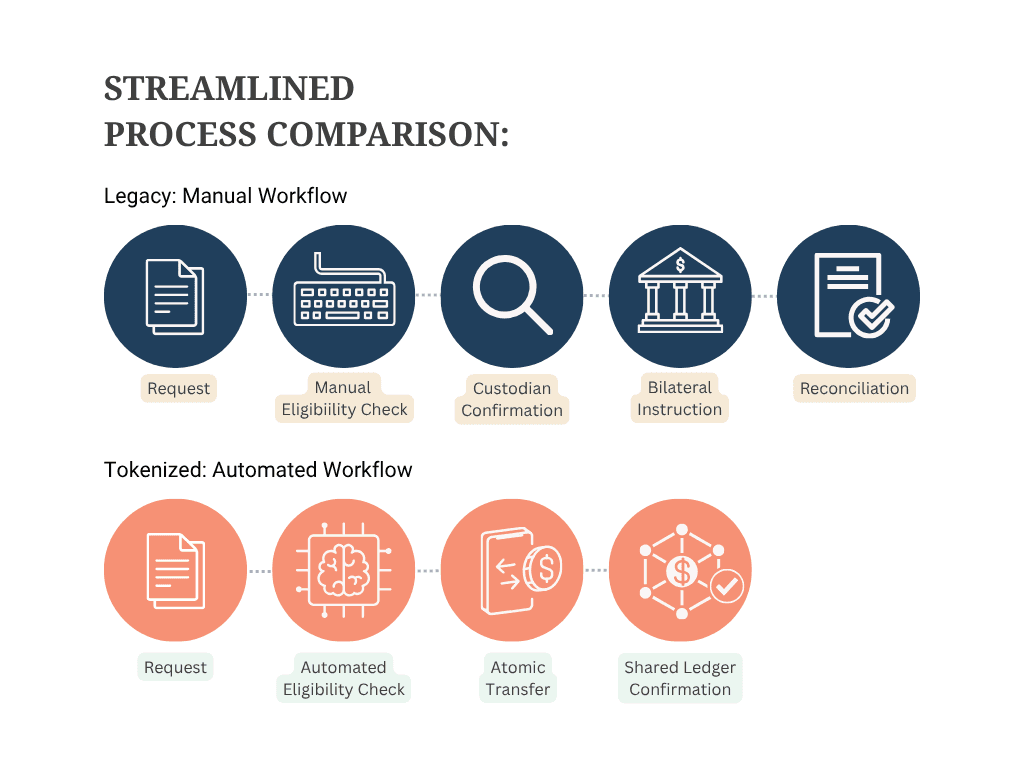

Collateral management connects three major areas: credit risk, cash management, and trade operations. Conventional securities financing runs each function on separate infrastructure. Custodians hold inventory in siloed systems. Eligibility checks are performed manually or in batch processes. Substitutions involve bilateral coordination across counterparties. Disputes trigger email threads and reconciliation breaks. These breaks can persist for days.

The cumulative friction is measurable. Operations teams look at fail rates and unresolved disputes to track performance. They also monitor asset swaps and capital buffers. These buffers are an insurance against uncertainty in settlement. These metrics represent direct costs. They also represent regulatory capital inefficiencies.

Tokenized collateral addresses each friction point at the process level. It does not simply convert assets to digital form. It restructures the workflow mechanics that generate operational cost.

The core mechanism is programmability. Smart contracts put trading rules directly into the asset layer. This automatically controls things like margin limits and asset swaps. Collateral conditions change. The system acts. It does not wait for a batch cycle. It does not wait for a phone call.

DTCC confirms that its Collateral AppChain platform is designed to modernize collateral mobility and improve capital efficiency, with Chainlink supporting orchestration, data, and automation. DTCC demonstrated this infrastructure approach in April 2025. The platform uses permissioned blockchain infrastructure. It enables near real-time collateral transfers. It enables automated operations through smart contracts. Dan Doney, tech chief at DTCC, says moving collateral is the 'killer app' for institutional blockchain. The platform aims for higher collateral velocity. It aims for capital efficiency. It aims for convergence between traditional and digital asset markets. A production launch is targeted for Q4 2026. Chainlink integrates as the data and orchestration layer. It automates eligibility, margining, and settlement across global markets.

This positions the operational conversation around concrete infrastructure. It does not position it around concept. Institutions evaluating tokenized collateral now have a market proof point. The post-trade industry's primary infrastructure provider built this proof point.

Institutions should map gains against five operational levers for internal benchmarking. These levers include:

Asset swap speed

Matching errors

Dispute resolution time

Automated rules

Intraday collateral movement

Each lever connects to measurable KPIs.

Operational Levers and KPI Mapping

Operational Lever | Legacy KPI Baseline | Tokenized Target | Primary Driver |

Substitution speed | 24 to 48 hours | Minutes to hours | Smart contract automation |

Reconciliation breaks | Multiple per week | Materially lower | Single shared ledger |

Dispute resolution time | 3 to 7 days average | Same-day or automated | Immutable transaction record |

Eligibility check cycle | End-of-day batch | Real-time continuous | On-chain rule encoding |

Intraday collateral velocity | One to two cycles per day | Multiple intraday cycles | 24/7 rail availability |

Where Substitution Time Actually Drops

Substitution is one of the most operationally intensive activities in securities financing. A counterparty requests a substitution. The operations team checks eligibility against the schedule. It confirms availability with the custodian. It sends instructions bilaterally. It waits for confirmation. It reconciles the transaction. Conventional workflows take 24 to 48 hours for this chain of actions. Standard market conditions allow this timeline. Stress conditions extend it.

The delay is not just inconvenient. It creates margin exposure windows. Institutions hold capital buffers during those windows. The buffers cover the risk of an unsettled substitution. A large book multiplies those buffers. Those buffers represent meaningful capital inefficiency.

Tokenized collateral compresses this timeline. It removes the manual handoffs. The smart contract holds the eligibility rules. A substitution triggers. The contract checks eligibility in real time. The replacement asset is eligible. The contract executes the transfer atomically. Both legs settle simultaneously. Record-based reconciliation can be significantly reduced. Both counterparties share the same ledger state.

This is not a marginal improvement. Reducing substitution time from two days to minutes changes the capital calculation. Firms may reduce buffers tied to operational delay. The margin requirement aligns to actual exposure. It does not align to processing delay.

Substitution Timing Breakdown

Stage | Legacy Time Estimate | Tokenized Time Estimate | Step Eliminated? |

Request receipt and logging | 1 to 4 hours | Seconds | No |

Manual eligibility screening | 2 to 6 hours | Automated, real-time | Yes |

Custodian instruction and confirmation | 4 to 12 hours | Integrated confirmation through the tokenized workflow | Manual step reduced |

Bilateral settlement instruction | Same-day to T+1 | Atomic settlement | Yes |

Post-trade reconciliation | 4 to 24 hours | Automated shared-state confirmation | Yes |

Total cycle | 24 to 48 hours | Minutes to 2 hours | Partial |

How Dispute Resolution and Reconciliation Change

Reconciliation breaks generate a large share of post-trade operational cost in securities financing. Each break requires investigation. Operations staff compare records across internal systems, custodian statements, and counterparty confirmations. They identify the source of the discrepancy. They are escalated internally or bilaterally. Teams resolve and re-reconcile.

Fragmented record-keeping causes most breaks. Each participant maintains its own ledger. Those ledgers update on different schedules. They use different identifiers. They reflect different cut-off times. Discrepancies are structurally inevitable.

Tokenized collateral can also reduce operational fails linked to delayed matching, late eligibility checks, and incomplete settlement instructions. It does not remove market or valuation disputes. It can reduce fails caused by fragmented records and manual handoffs.

Operations teams that currently dedicate headcount to reconciliation can redeploy that capacity. More precisely, firms can use the same headcount to manage a larger book. This improves operational leverage without adding staff.

Read how shared settlement infrastructure resolves intraday funding gaps and collateral mobility bottlenecks: On-Chain Repo for Intraday Funding and Collateral Mobility.

Legacy vs. Tokenized Dispute Workflow

Dispute Stage | Legacy Workflow | Tokenized Workflow |

Root cause identification | Cross-system record comparison, 1 to 3 days | Shared ledger audit, same day |

Escalation | Bilateral email and phone coordination | Not required for record disputes |

Resolution documentation | Manual sign-off across systems | Automated ledger confirmation |

Recurrence risk | High, same structural fragmentation persists | Low, shared record eliminates reoccurrence |

Average resolution time | 3 to 7 business days | Same day to 48 hours (valuation disputes only) |

Real-Time Eligibility and Intraday Mobility

Eligibility management is a persistent source of operational risk. Conventional workflows maintain eligibility schedules in static files or spreadsheet-based tools. Operations teams check those files manually against incoming collateral. Markets move. Eligibility classifications can lag. An asset cleared eligibility at the start of the day. It may breach a concentration limit or credit threshold by afternoon. Batch processing means that breach is not caught until the next cycle.

Smart contract-based eligibility encoding addresses this at the workflow level. The eligibility rules live on-chain. They apply continuously. The system monitors all assets in the collateral pool against current rules in real time. Approved market data can feed the eligibility engine. The system can apply approved updates to risk limits, credit caps, and haircut schedules. The system flags ineligible assets immediately. It can trigger substitution automatically.

Legacy workflows struggle to process rapid asset movements at scale. This new live layer makes it possible. Firms can deploy collateral in the morning. They can recall it for another purpose by midday. They can redeploy it before the day closes. The DTCC's Collateral AppChain explicitly targets this capability. The project aims to support faster collateral movement and broader collateral mobility.

Moving assets during the day matters most to firms with large, mixed asset pools. A repo desk, a stock lending team, and a clearing relationship all pull from this same pool of assets. Legacy infrastructure queues that inventory. Real-time mobility makes the same asset work harder across the book.

Explore how continuous margin calls and compressed settlement windows redesign daily collateral operations. How tokenized collateral changes margin calls, substitutions, and settlement windows.

The regulatory infrastructure for this approach is solidifying. In December 2025, the CFTC issued guidance. It reiterated that its regulations are technology-neutral. It affirmed the analytical framework around tokenized collateral in derivatives markets. That guidance supports the broader institutional discussion around tokenized collateral. It applies most directly to derivatives markets, so securities financing teams should treat it as adjacent regulatory context.

Modeling Your Own Efficiency Gains

Measurable gains from tokenized collateral depend on a firm's unique books and baseline costs. Standard vendor claims often obscure these individual differences. Sales pitches about average industry savings usually ignore these specific factors.

A rigorous internal model starts with three data inputs. First, the current substitution turnaround time across the book, measured in hours. Second, the average number of reconciliation breaks per week and the average resolution time per break. Third, firms must hold a capital buffer to cover multi-day settlement risks. Organizations can use these data points to calculate the exact cost of their current workflow.

They calculate it in operational hours and capital terms. The substitution gain translates directly to a reduction in the exposure window. It also reduces the associated capital buffer. The reconciliation gain translates to staff capacity redeployed or absorbed into book growth. The eligibility automation gain translates to reduced break frequency. It also reduces dispute-related cost.

Institutions at the evaluation stage should build this model before selecting technology partners. The model determines which gains are material for their specific operation. It also sets the KPI baseline. Post-implementation performance can be measured against that baseline.

How Should Firms Estimate Tokenized Collateral ROI?

A structured ROI model connects specific operational friction to tangible capital and labor savings. Firms should map their baseline inputs against expected tokenized gains to estimate the link to financial outcomes.

Tokenized Collateral ROI Model

KPI Category | Input Metric | Gain Lever | Measurable Outcome |

Substitution speed | Current average hours per substitution | Smart contract automation | Reduction in buffer capital requirement |

Reconciliation breaks | Weekly break count and resolution hours | Shared ledger | Staff hours recovered per week |

Dispute aging | Average dispute resolution days | Immutable shared record | Reduction in dispute-related exposure |

Eligibility exception rate | Daily exception volume | Real-time on-chain screening | Reduction in manual exception handling |

Intraday collateral cycles | Current cycles per day | 24/7 rail access | Increase in asset utilization rate |

Map your operational gains against a structured KPI model for collateral transformation programs. KPI model for a tokenized collateral transformation program.

Review Tokenized Inventory Collateral Guide 2026: Warehouse Receipts, Lender Control, and Audit Trails for managing warehouse receipts, lender control, and audit trails in tokenized inventory collateral.

TokenMinds helps collateral teams build custom performance models for their trading workflows. The same levers can be mapped against each institution's baseline workflow. Request a securities financing workflow workshop to map your current baseline. Identify the highest-impact gains. Build a prioritized transformation roadmap.

Frequently Asked Questions

Q: What is the most measurable operational gain from tokenized collateral in securities financing?

A: Substitution speed reduction produces the most measurable near-term gain. Compressing substitution from 24 to 48 hours down to minutes reduces the exposure window. That window drives capital buffer requirements. Institutions with large substitution volumes see direct capital savings. They see these savings before any change to their reconciliation or eligibility infrastructure.

Q: How does a shared ledger reduce reconciliation breaks in practice?

A: Matching errors happen when two trading partners have different transaction records. A shared ledger significantly reduces those differences by providing a single authoritative transaction source. Both parties read that record in real time. Breaks arising from record fragmentation can fall sharply. The operations workload shifts to narrower valuation and eligibility disputes. Those disputes are faster to resolve. They are lower in frequency.

Q: Does tokenized collateral require replacing existing custody infrastructure

A: No. New tools like DTCC's Collateral AppChain connect directly to legacy custody systems. They do not replace existing custody infrastructure. The tokenization layer is an overlay to the existing settlement systems. It translates entitlements into on-chain tokens for the specific transaction. This setup preserves existing custody and settlement controls within the larger settlement network. Firms study these connection setups whenever they redesign their daily workflows.

References

DTCC: Announcement of the digital collateral management platform and AppChain infrastructure, April 2025. https://www.dtcc.com/news/2025/april/02/dtcc-announces-new-platform-for-tokenized-real-time-collateral-management

DTCC: Official May 2026 announcement confirming Collateral AppChain as shared collateral infrastructure with a Q4 2026 production launch target. https://www.dtcc.com/news/2026/may/12/dtcc-collaborates-with-chainlink-to-advance-24-7-collateral-management

Traders Magazine: DTCC Digital Launchpad announcement and collateral platform demonstration details. https://www.tradersmagazine.com/departments/brokerage/dtcc-announces-new-platform-for-tokenized-real-time-collateral-management/

CFTC: Official December 2025 release confirming technology-neutral regulatory stance for tokenized assets used as collateral in futures and swaps markets. https://www.cftc.gov/csl/25-39/download

IMF Notes No. 26/01: Analysis of tokenized settlement, automated margining, and cross-border collateral mobility in tokenized financial systems, April 2026. https://www.imf.org/-/media/files/publications/imf-notes/2026/english/insea2026001.pdf

SEC No-Action Letter, DTCC: Narrow mechanics reference clarifying that Tokenized Entitlements do not receive collateral or settlement value for DTC's Net Debit Cap or Collateral Monitor calculations. https://www.sec.gov/files/tm/no-action/dtc-nal-121125.pdf