TL;DR

Invoice factoring, supply chain finance (SCF), and tokenized receivables all provide financing against receivables, but they differ significantly in ownership, control, risk allocation, data requirements, settlement workflows, and distribution options. This article compares all three models across operational, compliance, and borrower experience dimensions, and provides a decision framework to help banks determine when to modernize factoring, expand SCF, or pilot tokenized receivables collateral.

Product Definitions

Before comparing the three models, it helps to be precise about what each one actually is.

Invoice factoring is the outright purchase of a receivable by a lender or factor. The seller transfers legal title to the invoice. The factor assumes the collection risk and advances a percentage of the face value, with the balance, less fees, being paid after the debtor has paid.

Supply chain finance (SCF) is a buyer-driven program. Under this program, the buyer approves invoices and extends an offer to suppliers to get paid early through a platform. The rate of finance is determined by the creditworthiness of the buyer, not the supplier. The lender pays for the invoices that have been approved and gets repaid by the buyer on the original due date.

Tokenized receivables collateral is not an asset sale. The seller keeps ownership of the receivable and uses it as collateral for a loan or credit facility. The token records the pledge, verification status, repayment status, and release workflow.

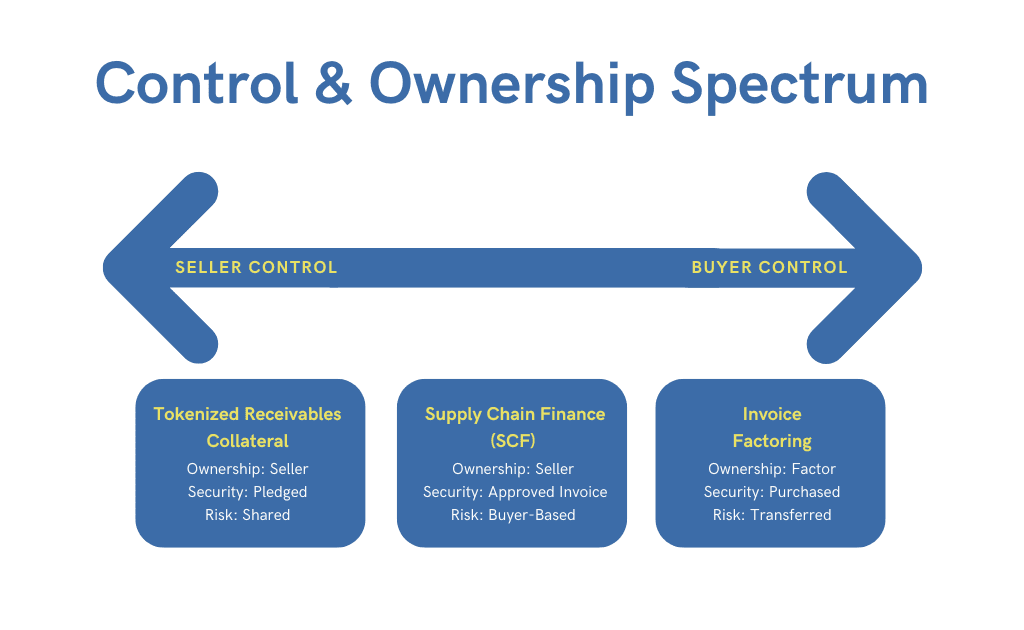

Each model sits at a different point on the control spectrum. Factoring transfers control entirely. SCF keeps control with the buyer. Tokenized collateral keeps the ownership with the seller. Meanwhile, it gives the lender a verified, legally enforceable security interest.

Control Model: Who Holds the Asset and the Risk

The control model describes what happens when something goes wrong.

In a non-recourse deal, the receivable is owned by the factor, and the factor absorbs the loss if the buyer fails to pay. But in a recourse arrangement, the factor comes back to the seller to get the money back.

In both recourse and non-recourse factoring, legal title transfers to the factor at the time of purchase.

In SCF, the buyer is the credit anchor. The lender’s exposure is to the buyer, not the supplier. The lender is at risk if the buyer defaults, regardless of whether the underlying invoice is valid or not.

In tokenized receivables collateral, the lender holds a secured right against a verified invoice before funding takes place. The seller retains ownership of the receivable, while the lender enforces against the pledged receivable if the debtor defaults. Legal enforceability depends on how well the pledge was perfected at origination.

Dimension | Invoice Factoring | Supply Chain Finance | Tokenized Collateral |

Legal title | Transfers to factor | Remains with supplier | Remains with seller |

Credit anchor | Debtor | Buyer | Debtor |

Enforcement right | Factor owns the claim | Lender has buyer obligation | Lender holds security interest |

Recourse structure | Recourse or non-recourse | Non-recourse to supplier | Depends on pledge terms |

Data Flow: ERP Integration, Verification, and Audit Trail

Data flow is where the three models diverge most sharply in operational terms.

Traditional factoring starts when the seller submits an invoice. From there, verification is manual and reconciliation happens only periodically. Audit trails exist but are mostly in proprietary systems and not very interoperable.

SCF platforms have greatly improved data connectivity. Buyers push approved invoice data directly to the platform. Suppliers access early payment on demand. The buyer is in charge of this flow of data, so it’s a relatively clean process. But it still relies on the buyer’s acceptance for verification, rather than independent confirmation.

Of the three, tokenized receivables collateral requires the most stringent data workflow. Invoice authenticity requires source confirmation. Debtor confirmation needs independent documentation. Completion of goods or services requires evidence. A duplicate financing check must be performed prior to tokenization. Each verification event must be logged with a timestamp and actor ID.

Praxent’s analysis suggests the market is moving towards API-driven, fraud-aware workflows and tokenized collateral speeds this up by incorporating verification data into the asset instead of a separate step.

For a deeper look at invoice verification and pledge workflows, read Tokenized Receivables Collateral Guide 2026: How Banks Can Finance Verified Invoices.

Settlement Mechanics: Timing, Currency, and Release

Differences in settlement have direct consequences for treasury operations and portfolio management.

The factoring settlement is typically T+1 to T+2 for the initial advance. The final settlement is when the debtor pays which may be 30 to 90 days after purchase. FX management is needed for currency mismatches between invoice and factor funding currency.

SCF settlement is linked to the buyer’s payment cycle. The lender provides an advance against approved invoices and gets repaid on the original due date. The settlement is predictable because the buyer’s payment behavior is the main variable.

Tokenized collateral settlement can be automated through payment reconciliation triggers. The debtor pays and the event is captured and reconciled against the token record. The advance is recovered and the pledge release is automatically initiated, removing manual steps and streamlining the release process while creating a clean timestamped record of every settlement event.

Dimension | Invoice Factoring | Supply Chain Finance | Tokenized Collateral |

Initial advance timing | T+1 to T+2 | On demand after buyer approval | On demand after verification and pledge |

Repayment source | Debtor | Buyer | Debtor |

Settlement predictability | Moderate | High | Moderate to high |

Release workflow | Manual | Automated at due date | Automated on payment confirmation |

FX management | Required for cross-currency | Buyer-determined | Required for cross-currency |

Distribution and Servicing: Secondary Market Options

Banks may distribute receivables positions to outside investors or other lenders, but the ease of distribution depends on documentation quality, verification standards, servicing rules, and transfer mechanics.

Factored receivables can be sold or securitized, but the process usually requires heavy documentation, legal review, and portfolio-level due diligence. Secondary market liquidity for factored portfolios exists but is not standardized.

SCF programs are increasingly structured as investor-accessible facilities. Some platforms allow multiple funders to participate in a single buyer program. This approach spreads the concentration risk across a much broader capital base.

Tokenized receivables collateral can reduce operational friction in co-lending and portfolio transfers, but legal assignment, pledge transfer, participant permissions, registry updates, and servicing responsibilities still need to be governed by the program structure.

For banks considering co-lending or portfolio distribution, read How Banks Can Safely Distribute Tokenized Receivables Pools.

Servicing also changes under tokenized collateral. In factoring, the factor usually manages collection after purchasing the invoice. In SCF, servicing is tied to the buyer's approved payment cycle. In tokenized receivables collateral, the bank must track invoice status, debtor payment, disputes, substitutions, partial repayments, defaults, and pledge release through the collateral record. This makes servicing more data-driven, but only if the bank has clear rules for exceptions and reconciliation.

Borrower Experience: Onboarding, Funding Speed, and Flexibility

The borrower experience is critical to driving product adoption and customer retention, especially in the hyper-competitive SME and mid-market lending segments.

Factoring onboarding is usually document intensive. The seller must provide trade history, debtor lists and contract terms. Approval times vary based on the factor and the size of the program. Once onboarded, the seller has limited visibility into the status of individual invoices after sale.

The SCF onboarding is buyer led. The supplier experience depends on which buyer programs they are connected to. Suppliers with large buyer programs can benefit from competitive rates and fast access to funding. But they have no say in which invoices get approved and when.

The setup costs are highest for tokenized collateral onboarding. The first step is to connect the seller’s ERP or e-invoicing system to the platform. Once the debtor confirmation workflow is active, the borrower can simply replace maturing invoices. This means they don't have to renegotiate the entire facility.

Dimension | Invoice Factoring | Supply Chain Finance | Tokenized Collateral |

Onboarding complexity | Moderate | Low for supplier | High initial setup |

Funding speed post-onboarding | Fast | Fast | Fast |

Borrower asset control | None after sale | Limited | Full ownership retained |

Reporting visibility | Limited | Buyer-controlled | Real-time, borrower-accessible |

Facility flexibility | Invoice by invoice | Buyer program limits | Pool substitution supported |

Risk and Compliance: AML, Fraud, and Legal Enforceability

All three models carry AML and KYC obligations. In each case, the burden of compliance is on the lender.

Factoring fraud risks include fake invoices, duplicate invoices, inflated invoice values, and double financing. Traditional controls rely on debtor checks and periodic portfolio reviews. Digital platforms with automated ERP integration catch fraud earlier through hash-based matching and real-time validation. However, these security measures are not yet standardized across all platforms.

SCF fraud risk is lower because buyer approval serves as the primary authenticity check. The buyer is unlikely to approve an invoice for goods or services they did not receive. International SCF programs carry additional complexity. Compliance teams must navigate complex buyer credit risk assessments and varying legal enforceability rules for cross-border payment obligations.

Tokenized collateral can improve fraud controls by requiring invoice verification, debtor confirmation, duplicate financing checks, and timestamped audit records before funding. However, legal enforceability still depends on pledge perfection, debtor notification rules, insolvency treatment, and jurisdiction-specific secured lending requirements.

Decision Framework: Where to Modernize First

Banks evaluating trade finance modernization face a sequencing question. The answer depends on four factors.

Existing portfolio composition. Banks with large factoring books should digitize that workflow first. Do this before launching a tokenized collateral program. Digital factoring builds essential data infrastructure. This includes ERP integration, invoice hashing, and debtor verification. This infrastructure directly supports tokenized collateral at the next stage.

Buyer relationship strength. Strong anchor buyer relationships give banks a major advantage. They may be better positioned to scale SCF programs before introducing seller-led tokenized collateral. SCF builds the buyer data connectivity that can feed a tokenized program later.

SME borrower demand. Prioritize tokenized receivables for SME borrowers who want to keep asset ownership. This product design fits their needs better than traditional factoring or SCF.

Internal data preparedness. Tokenized collateral requires the highest level of data infrastructure maturity. Banks lacking ERP connectivity or structured verification should build those capabilities first. Do this via a digital factoring upgrade or an SCF platform deployment. This is a prerequisite to adopting a full tokenized collateral program.

Starting Condition | Recommended First Step |

Large factoring book, limited data infrastructure | Digitize factoring with ERP integration and invoice hashing |

Strong anchor buyer relationships | Expand SCF and build buyer data connectivity |

SME borrowers wanting asset retention | Pilot tokenized receivables collateral with a defined invoice pool |

High data maturity, existing verification workflows | Launch tokenized collateral program with secondary market distribution |

Modernize Receivables Finance With TokenMinds

Banks do not need to replace factoring or SCF overnight. The better path is to identify which workflow should be modernized first, then build the data, verification, collateral, and settlement layer around it.

TokenMinds helps banks assess receivables workflows, design tokenized collateral pilots, and plan the infrastructure needed for invoice verification, pledge tracking, reconciliation, and controlled distribution.

Schedule a trade finance modernization workshop with TokenMinds. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What is the difference between invoice tokenization and factoring?

A: Factoring sells the receivable to a factor. Tokenized receivables collateral keeps ownership with the seller and records the pledged invoice as collateral for a loan.

Q: How is tokenized receivables financing different from supply chain finance?

A: SCF is usually buyer-led and depends on approved invoices from an anchor buyer. Tokenized receivables financing is seller-led and depends on verified invoices, pledge records, and lender-controlled collateral monitoring.

Q: Should banks tokenize receivables or digitize factoring first?

A: Banks with weak invoice data infrastructure should usually digitize factoring first. Banks with strong ERP connectivity, verification workflows, and collateral monitoring can move faster toward tokenized receivables pilots.

Q: Can a bank run all three products simultaneously?

A: Yes, and many do. Factoring, SCF, and tokenized collateral are all employed to serve different segments of borrowers and risk profiles. The challenge is having separate data workflows and compliance controls for each. Banks with strong platform infrastructure can run all three from one system. They just need to keep data models and permissioning distinct.

Q: Is tokenized receivables collateral more expensive to operate than factoring?

A: It takes a bigger up-front investment to get it set up. The budget has to include complex ERP integrations and custom verification workflows. It has to include the legal work for proper pledge perfection. Ongoing operational cost per invoice is lower once the workflow is automated. The cost comparison shifts in favor of tokenized collateral at scale. This is particularly true for banks processing high invoice volumes with automated reconciliation.

Q: What is the regulatory regime applicable to tokenized receivables collateral?

A: In many jurisdictions, tokenized receivables collateral may be structured under existing secured lending rules because the token can act as a record of the pledge rather than a new financial instrument. Banks should still confirm pledge perfection, debtor notification, insolvency treatment, and transferability with local counsel before going live.

References

Praxent: “Invoice Factoring Digital Trends.” Discusses the trend of digital factoring moving toward API-driven, fraud-aware workflows. https://info.praxent.com/blog/invoice-factoring-digital-trends