TL;DR

Banks can use tokenized receivables as collateral. Most guides stop at definitions. The real question is how the full lifecycle works in practice. This guide maps each stage: invoice capture, debtor confirmation, pledge, funding, repayment, release, and audit trail. It also covers operational benchmarks and the continuous monitoring framework banks need to run the program at scale.

Why Banks Are Looking at Receivables as Collateral

Trade finance is one of the oldest forms of bank lending. A supplier ships goods. An invoice follows. The buyer owes money in 30, 60, or 90 days. That obligation has always had financial value.

Tokenization does not change what a receivable is. It changes how the bank verifies it, controls it, and uses it in a structured collateral workflow. The BIS points to platforms like Credix and AmFi as early examples of tokenized receivables being used to access credit lines, with SME credit access as a central benefit.

The value for banks is not just speed. It is the ability to build a reliable collateral record that can be audited, transferred, and enforced with precision.

What Is Tokenized Receivables Financing?

Tokenized receivables financing turns verified invoices into digital collateral records. Banks can use those records to confirm invoice data, debtor acceptance, pledge status, payment events, and release history. The token is not the collateral by itself. The verified receivable, legal pledge, and audit trail create the bank-grade collateral position.

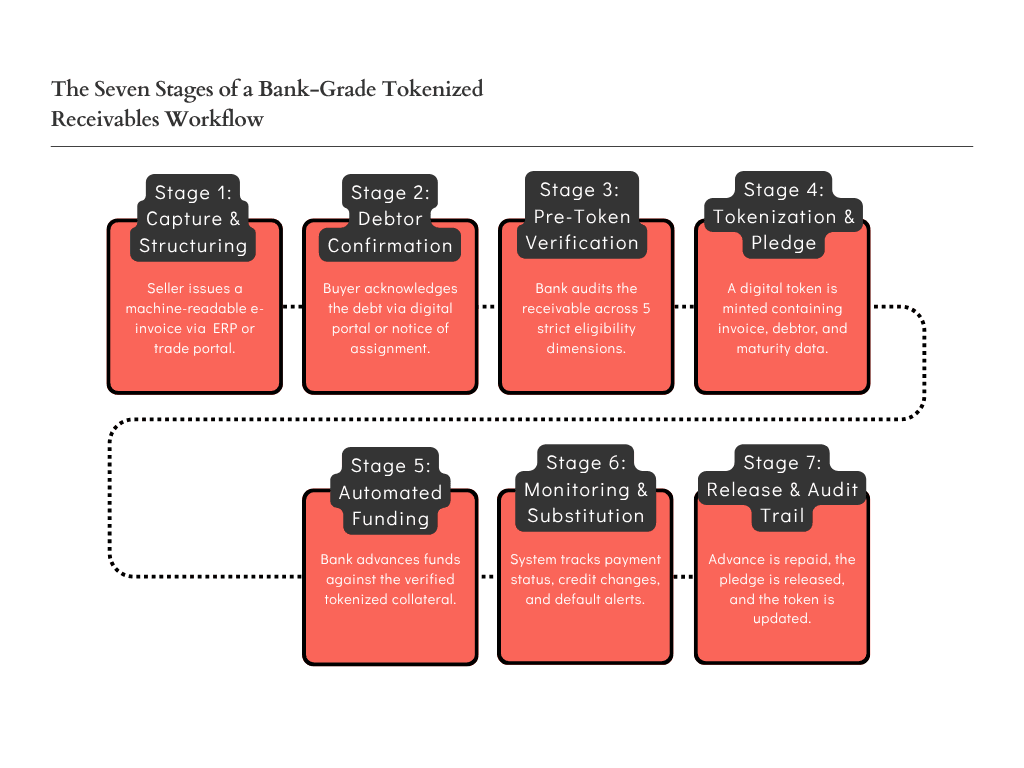

The Seven Stages of a Bank-Grade Tokenized Receivables Workflow

Most explanations of invoice tokenization focus on the minting step. That step matters. But it is one part of a longer process. For a bank to treat a tokenized receivable as eligible collateral, the institution needs confidence at every stage. Here is how that lifecycle runs.

Stage 1: Invoice data capture and structuring

The invoice is the starting point. The seller issues it through an ERP system, e-invoicing platform, or trade finance portal. The record should include buyer name, invoice number, amount, due date, payment terms, and trade details.

For bank collateral, the data has to be complete and machine-readable. Verification risk increases when data is fragmented or entered manually. Banks that scale need structured data feeds, not scanned PDFs.

Stage 2: Debtor acceptance and confirmation

An invoice is not confirmed collateral until the debtor acknowledges it. Debtor confirmation is a critical control point. Without it, the bank holds a claim the buyer may dispute or reject.

Confirmation can take several forms. The debtor may sign a notice of assignment. They may confirm via a secure digital portal. In some structures, the debtor provides an irrevocable payment instruction directly to the bank. The format is less important than the outcome: a documented, enforceable acknowledgment that the debt exists and will be paid to the lender.

This step also serves as the first fraud screen. If a debtor fails to recognize an invoice, the bank has identified a problem before any funds are committed.

Stage 3: Verification prior to tokenization

Prior to tokenizing a receivable, the bank needs to verify that it meets the eligibility criteria. Verification has five dimensions.

Verification Dimension | What the Bank Confirms |

Invoice authenticity | Invoice matches a real delivery with supporting documentation |

Debtor creditworthiness | Obligor has acceptable credit standing based on scoring or ratings |

No prior assignment | Receivable has not been pledged or sold to another creditor |

Eligible asset class | Receivable type, jurisdiction, and currency meet collateral policy |

Concentration limits | Adding the receivable does not breach sector or obligor limits |

This step is the basis of the collateral control framework. Omitting it or weakening it creates downstream legal and operational risk. Lenders using self-reported data without independent verification remain exposed to duplicate financing and fraud.

Stage 4: Tokenization and Pledge

Tokenization does not automatically create legal priority. The bank still needs a valid pledge, assignment, notice, or registration process under the relevant jurisdiction. When a receivable is verified, it can be tokenized. The token embodies a specific verified payment claim. It contains the invoice data, the debtor confirmation status, the assigned maturity, and the legal pledge details.

The bank must also perfect its security interest under applicable law. This requires completing jurisdiction-specific formalities, such as debtor notices or public registry filings, depending on the receivable type and governing law.

Stage 5: Funding

Once the pledge is completed, the bank makes advances against the receivable. The advance rate depends on the quality of the receivable, the credit profile of the debtor, maturity and the bank’s internal collateral policy. The smart contract logic can calculate the eligible collateral value at the time of funding, apply haircuts based on current parameters and track the drawdown amount against the pledged receivable. This reduces manual steps and provides a clean audit trail of each funding event.

Stage 6: Monitoring, repayment and substitution

When the financing is granted, the bank monitors the receivable until the debtor pays. Monitoring covers three areas: invoice payment status, debtor credit quality, and early payment or default triggers.

When the debtor makes a payment, cash flows to the bank to repay the advance. If the receivable pays early, the bank may need replacement collateral. Tokenized structures can support substitution workflows. New verified invoices are added to the pool as older ones mature or pay down.

Stage 7: Release and Audit Trail

Once the advance is fully repaid, the pledge is released. The token record is updated to reflect the release. The audit trail is the final product of the entire lifecycle. Every event is logged: invoice data at origination, debtor confirmation, verification results, pledge registration, funding drawdown, payment receipt, and final release.

For a full breakdown of what data banks need to capture and confirm before an invoice can enter the tokenization workflow, read What Data Must Banks Verify Before Tokenizing Accounts Receivable?

Collateral Performance Metrics Banks Should Track

Operational outcomes separate tokenized programs from paper-based processes. Banks should track five KPI areas when evaluating tokenized receivables workflows.

KPI | Conventional Process | Tokenized Workflow | Improvement |

Invoice verification time | 2–3 business days | 3–5 hours | ~90% faster |

Duplicate financing detection | Post-funding review | Pre-funding registry check | Prevents exposure before funds are advanced |

Collateral onboarding cost | USD 150–300 per invoice (manual) | USD 20–50 per invoice (automated) | ~75–85% cost reduction |

Audit preparation time | 2–3 weeks per quarter | Real-time log export | Near-zero preparation overhead |

Substitution workflow | 3–7 days (manual review) | Same-day (automated eligibility check) | ~80% faster collateral replacement |

*These figures should be treated as indicative ranges. Actual results depend on platform design, bank infrastructure, invoice volume, and local legal requirements.

The duplicate financing detection improvement is particularly significant. In conventional programs, double-pledging is often discovered after funds are advanced. In tokenized programs with a shared registry, the check happens before any funding is committed. That difference matters for credit risk management.

Continuous Collateral Monitoring: The Bank Operating Model

The monitoring stage is where most procedural guides stop short. Knowing that monitoring should happen is not the same as knowing how to run it operationally. Banks managing tokenized receivables at scale need a real-time framework. Batch-cycle reviews are not enough.

The framework consists of five dashboard components. Each tracks a specific risk dimension. Each triggers an automated response.

Dashboard Component | What It Tracks | Automated Action |

Concentration risk monitor | Sector or obligor exposure approaching policy limits | Alert sent to credit officer; new invoices from that obligor held for review |

Debtor deterioration alerts | Credit score change, rating downgrade, or payment delay signal | Automatic haircut adjustment applied to affected invoices |

Payment aging thresholds | Days past due on each invoice in the pool | Invoice flagged; collection team notified; collateral value reduced |

Haircut adjustment engine | Receivable maturity, debtor quality, and market conditions | Real-time collateral value recalculated; borrowing base updated |

Exception management queue | Invoices outside normal eligibility parameters | Routed to analyst for manual review; excluded from borrowing base until cleared |

The key operating principle is exception-based management. The system runs 24/7. Analysts only review exceptions, not the entire portfolio. This allows a small collateral team to manage a large, active invoice pool without manual checks on every receivable.

Payment aging thresholds and haircut engines work together. When a debtor misses a payment, the aging flag triggers an automatic haircut adjustment. The borrowing base decreases. The borrower must then pledge additional receivables or reduce the outstanding advance.

Risk Controls Banks Must Build Into the Workflow

Duplicate Financing Prevention

Duplicate financing occurs when the same receivable is pledged to more than one lender. Tokenization reduces this risk if the platform maintains a central register of pledged receivables. Before accepting an invoice, the bank checks whether it has already been tokenized and pledged on any connected platform.

The token itself does not prevent duplicate financing unless the underlying registry is shared and enforced. Banks should verify that the tokenization platform they use has a credible deduplication mechanism before relying on it for collateral control.

Fraud Prevention

Invoice fraud can take many forms: fictitious invoices for nonexistent trade, inflated quantities, invoices from related entities at non-arms’ length prices, and forged debtor signatures. The verification stage is the first line of defense against fraud. Banks should seek documentary evidence of the underlying trade. Debtor confirmation provides a second layer of verification that is more difficult to forge at scale.

For a detailed look at how banks can build deduplication controls into a tokenized invoice program, read How to Prevent Double Financing in Tokenized Invoice Collateral.

Operational Integration Points That Matter

Integration Point | Function | Why It Matters for Collateral |

ERP systems | Source of invoice data and trade records | Eliminates manual entry and reduces verification errors |

E-invoicing infrastructure | Government or platform-level invoice registration | Provides independent confirmation of invoice and debtor details |

Debtor confirmation portals | Direct digital acknowledgment from obligors | Creates enforceable record without paper-based notices |

These integrations outline how much of the lifecycle can be automated. Banks with robust ERP connectivity can handle large volumes of invoices with little manual review. Banks with paper-based processes face scaling limits that cap program size and increase operating costs.

Legal Control and Priority: What Banks Cannot Outsource

Technology improves data handling and automation. It does not replace legal formality. Banks using tokenized receivables as collateral must comply with the same legal requirements as for traditional receivables financing. Perfection of a security interest is jurisdiction-specific. For example, in some countries, the assignment must be notified to the debtor to be enforceable against third parties.

In other countries, registration in a public registry is necessary. A tokenized record that is not in proper legal formality offers operational convenience but not legal priority. Legal counsel should review the pledge structure prior to the program going live, including the governing law of the receivables, the form of the security agreement and the steps needed for perfection in each relevant jurisdiction.

Collateral Lifecycle Summary

Stage | Key Action | Primary Control Point |

1. Invoice Data Capture | Structured data ingestion from ERP or e-invoicing | Data completeness and source authentication |

2. Debtor Confirmation | Formal acknowledgment from the obligor | Fraud screening and enforceability |

3. Verification | Eligibility check across credit, legal, and operational criteria | Duplicate financing prevention |

4. Tokenization and Pledge | Token minting and security interest registration | Legal perfection and priority |

5. Funding | Advance against verified collateral value | Advance rate and haircut application |

6. Monitoring and Repayment | Payment tracking and portfolio review | Early payment, substitution, and default triggers |

7. Release and Audit | Pledge release and complete event log | Regulatory reporting and dispute resolution |

What This Means for Banks in 2026

The institutional case for tokenized receivables financing is collateral control and operational efficiency. Banks that verify, pledge, monitor, and release receivables with precision are better positioned to extend credit at scale. They can manage portfolio risk and meet regulatory expectations more effectively.

The performance metrics above show where potential operational gains concentrate: verification speed, onboarding cost, and audit overhead. The monitoring framework shows how those gains extend into the post-funding lifecycle. Together, they define what a production-grade tokenized receivables program actually requires.

Banks that invest in these operational foundations now will be better placed to serve SME borrowers. They will compete more effectively in trade finance markets and deploy receivables as collateral at an efficiency level that paper-based processes cannot match.

If your institution is ready to test this in a controlled environment, read 90-Day Tokenized Receivables Collateral Pilot: A Bank Sandbox Roadmap.

Interested in mapping your bank’s tokenized receivables journey? Schedule a collateral lifecycle assessment with our trade finance experts. Contact TokenMinds to schedule a tokenized receivables collateral workshop: https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What is the difference between tokenized receivables financing and traditional invoice discounting?

Traditional invoice discounting uses paper-based or email-based processes. Verification is done by hand. The collateral record sits in internal spreadsheets or legacy systems. Tokenized receivables financing shares the invoice data, debtor confirmation, pledge status and payment record on a common ledger. As a result, the collateral record is real time, auditable and accessible to multiple authorized parties with no reconciliation gaps.

Q: If I tokenize a receivable, does that automatically mean it is eligible collateral for a bank?

No. Tokenization is a digital representation of the receivable. Eligibility depends on verification: the invoice must be for a real trade, the debtor must confirm it, it must not be pledged elsewhere, and it must meet the bank’s credit and legal criteria. A token that does not pass these checks is not eligible collateral regardless of the technical format it is in.

Q: How do banks know that the same invoice is not pledged to two lenders?

The most reliable mechanism is a shared receivables registry that records each pledge as it happens. Before accepting an invoice, the bank checks the registry for existing claims. Some platforms build this registry into their tokenization infrastructure. Where no shared registry exists, banks must run independent deduplication checks against their own records and any available market data.

Q: What makes an invoice verified for bank lending?

A verified invoice should include structured invoice data, debtor confirmation, trade documentation, no prior pledge, and eligibility under the bank’s collateral policy.

Q: Does tokenization remove credit risk?

No. Tokenization improves verification, monitoring, and auditability. The bank still manages debtor risk, borrower risk, legal enforceability, and concentration exposure.

Q: Can banks use tokenized receivables across jurisdictions?

Yes, but legal perfection, debtor notice, assignment rules, and registry requirements vary by jurisdiction.

References

Bank for International Settlements: "Tokenisation of deposits and other financial assets" (othp92). Covers Credix and AmFi as examples of tokenized receivables used to access credit lines. https://www.bis.org/publ/othp92.pdf