TL;DR

Three documents appear in trade finance collateral discussions. Each works differently for title, possession, control, pledge, and enforcement. This guide adds four layers most comparisons omit: collateral enforcement outcomes after default, a three-layer control model for tokenized instruments, conflict-of-priority scenarios across multiple creditors, and a corridor-specific implementation matrix. It closes with a decision framework for product and legal teams.

Document Fundamentals at a Glance

Document | Legal Basis | What It Proves | Holder Right |

Warehouse receipt | Warehouse receipt law, with UNCITRAL-UNIDROIT Model Law as reference framework | Goods in storage at a licensed warehouse | Claim or pledge the stored goods |

Bill of lading | Shipping law plus MLETR where adopted | Goods received for shipment | Claim goods on arrival or pledge in transit |

Inventory token | Contract law, platform rules | Digital representation of a goods claim | Contractual only unless statute extends further |

Transferability and Control

Document | How Transfer Usually Works | Lending Meaning |

Warehouse receipt | Endorsement, registry transfer, or warehouse notice | The bank may control stored goods if the receipt and pledge are valid |

Bill of lading | Endorsement, possession, or eBL platform transfer | The bank may control goods while they are in transit |

Inventory token | Platform transfer under contract rules | Token transfer does not automatically transfer legal control |

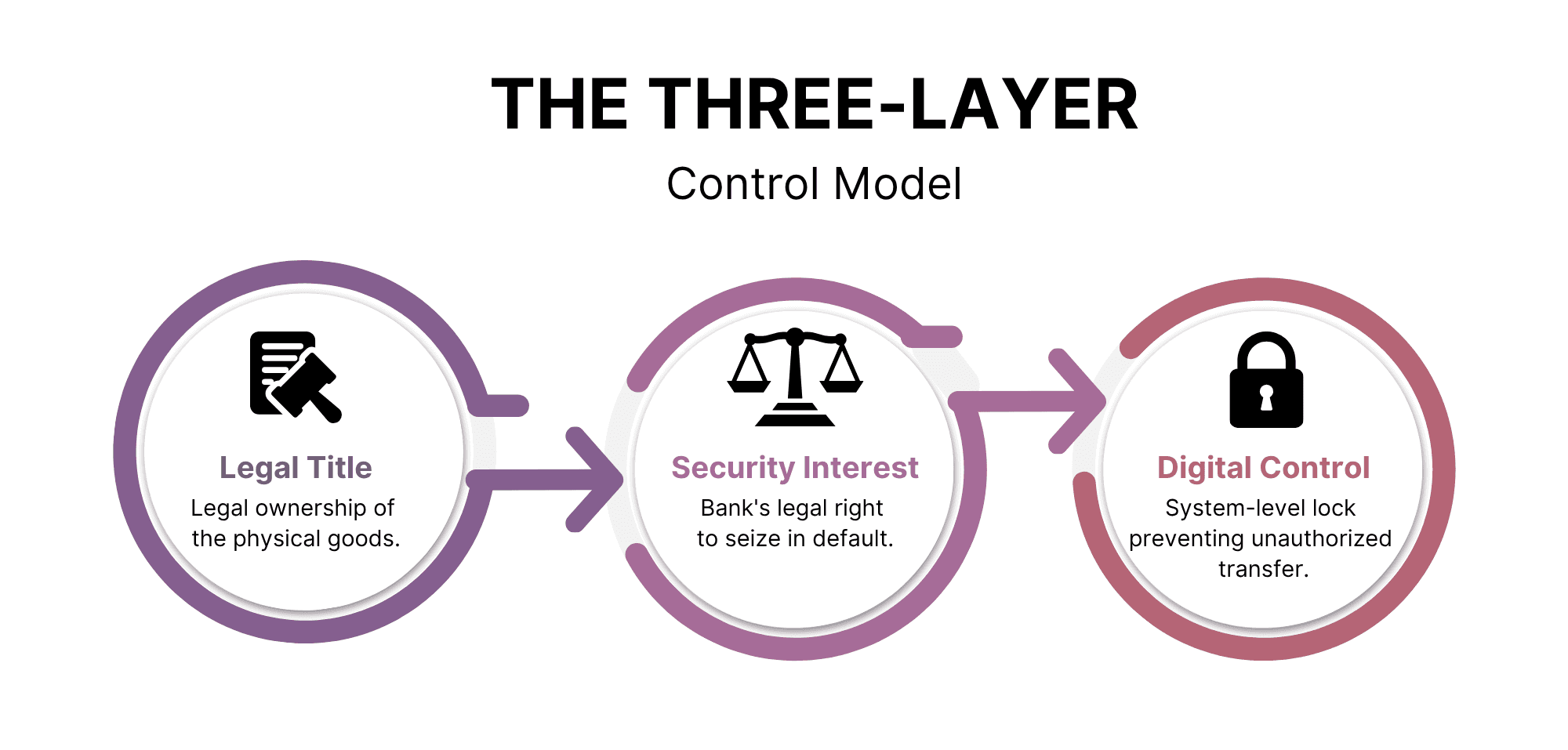

Title, Possession, and Control: The Three-Layer Model

Most comparisons treat these as one concept. They are three separate legal layers. Banks that conflate them underestimate their enforcement risk.

Layer 1: Legal title. Ownership of the goods. Determines who can sell or pledge. A warehouse receipt may give the holder title depending on jurisdiction and receipt type. An inventory token holder may not, depending on the contract.

Layer 2: Security interest. Legal right of the bank to goods in default. Created by pledge agreement. Perfected by possession, control or registry filing depending on jurisdiction.

Layer 3: Digital control. The ability to prevent a transfer or release through a system. This is operational control, not legal control. MLETR states that digital control is equal to possession of physical documents (for covered documents) under the law, but only in those jurisdictions that adopt MLETR.

Document | Layer 1: Legal Title | Layer 2: Security Interest | Layer 3: Digital Control |

Warehouse receipt | Holder may have title, depending on jurisdiction and receipt type | Pledge via notice or endorsement | Electronic registry where MLETR adopted |

Bill of lading | Holder may have title in transit, depending on shipping law | Pledge via endorsement or eBL platform | eBL platform control under MLETR |

Inventory token | Contract-dependent | Requires separate security agreement | Platform-enforced, not statute-backed |

The inventory token gap is critical. Layer 1 only works if the contract explicitly transfers title. Layer 2 requires a separate legal instrument. Layer 3 exists at the platform level but carries no statutory weight without specific legislation.

Banks using warehouse receipts or eBLs in MLETR-aligned jurisdictions can receive stronger alignment between document control, legal recognition, and operational transfer rights.

Paper Bills of Lading vs Electronic Bills of Lading

A paper bill of lading and an electronic bill of lading serve the same trade function. Both can evidence goods received for shipment and support control over goods in transit. The difference is legal recognition. A paper bill relies on physical possession and endorsement. An eBL relies on platform control and the law of the relevant corridor, including whether MLETR or equivalent rules apply.

Collateral Enforcement After Default

Creating a pledge is step one. Enforcing it under time pressure is the real test. The three documents produce materially different enforcement outcomes.

Warehouse receipt enforcement

The bank holds or controls the receipt. On default, it instructs the warehouse to hold the goods pending sale. The bank employs a selling agent or a commodity broker to liquidate. The proceeds of sale repay the advance. In a cooperative warehouse and liquid commodity market, warehouse receipt enforcement may be faster than token-only enforcement.

The primary risk is warehouse operator cooperation. A warehouse that disputes the bank's instruction authority creates delay. A correctly drafted tripartite agreement can reduce this risk by confirming the warehouse operator’s obligation to follow the bank’s instructions. Without it, the bank must obtain a court order before the operator will act.

eBL enforcement in transit

The bank holds the eBL on the eBL platform. On default, it endorses the eBL to a buyer it arranges or redirects the goods to a destination port where it can take possession. eBL enforcement can take longer when destination port recognition or carrier cooperation is uncertain.

Principal risk: Port jurisdiction. If the goods arrive in a jurisdiction that does not recognize the legal standing of the eBL platform, the bank may need local legal process to take possession. Banks must pre-map enforcement procedures for every destination port in the corridor before the facility is put in place.

Enforcement of inventory token

The bank's promise is contractual. If the borrower defaults, the bank cannot instruct the warehouse or redirect the goods by virtue of the token itself. The bank must rely on the security agreement and in most jurisdictions obtain a court order or follow the statutory enforcement process for secured creditors. Inventory token enforcement is often slower because the bank usually relies on a security agreement, public filing, and local enforcement procedure.

Enforcement Dimension | Warehouse Receipt | Bill of Lading | Inventory Token |

Basis for enforcement | Document of title where recognized | Document of title where recognized | Security agreement only |

Warehouse or carrier cooperation | Required, secured by tripartite agreement | Carrier cooperation required at destination | Operator cooperation required, no document right |

Typical enforcement timeline | May be faster in cooperative markets | May take longer with port/carrier uncertainty | Often slower due to court process requirements |

Primary risk | Operator dispute without tripartite | Destination port recognition | Court process required in most markets |

Conflict-of-Priority Scenarios

Priority disputes arise when more than one creditor claims the same goods. The document type strongly affects priority, but the final outcome depends on governing law, perfection, notice, registry rules, and possession or control.

Scenario A: Bank A holds electronic warehouse receipt, Bank B files a public security interest.

Bank A has constructive possession under MLETR because it controls the electronic receipt. Bank B has a public filing but no control of receipt. In an MLETR compliant jurisdiction, the control position will generally prevail over the filing position. In a non-MLETR compliant jurisdiction, the public filing position may prevail. Banks operating across both environments must confirm the applicable rule for each storage location.Scenario B: Two banks each hold an endorsed copy of the same paper bill of lading.

This is the classic bill of lading fraud pattern. Both banks have a facially valid document. Priority depends on which bank first took the document in good faith and for value. The second bank has a legal claim against the fraudulent party but may not recover from the goods. This risk is substantially reduced with eBLs because the platform enforces singularity.Scenario C: Bank holds inventory token, subsequent purchaser buys the goods in good faith.

The token gives the bank a contractual claim. A good-faith purchaser who receives the actual goods from the warehouse, and who has no notice of the bank's token-based claim, may take free of the bank's interest in many jurisdictions. This depends on whether the bank's security interest was perfected through a public filing. An unperfected interest typically loses to a good-faith purchaser. A perfected interest may still lose if the jurisdiction gives priority to buyers in the ordinary course of business.

Scenario | Document | Priority Outcome | Key Risk |

Control vs public filing | Electronic warehouse receipt | Control wins in MLETR jurisdictions | Non-MLETR jurisdictions may favor filing |

Duplicate paper endorsement | Paper bill of lading | First good faith holder wins | Second holder loses rights in the goods |

Token vs good faith purchaser | Inventory token | Purchaser may prevail if interest unperfected | Unperfected token pledge loses in most markets |

Corridor-Specific Implementation Matrix

MLETR adoption determines which documents carry legal weight electronically. Banks must match document choice to corridor legal environment before structuring a facility.

Corridor Type | Warehouse Receipt | eBL | Inventory Token |

Both jurisdictions MLETR-aligned | Electronic receipt fully enforceable | eBL carries full legal weight | Token requires separate security layer |

Origin MLETR-aligned, destination not | Electronic receipt valid at origin | eBL may lose legal standing at destination | Token requires dual legal backing |

Neither jurisdiction MLETR-aligned | Paper receipt remains controlling | Paper BL required, eBL is tracking only | Token is contractual only, high enforcement risk |

Domestic trade, no cross-border element | Electronic receipt typically recognized | eBL not relevant | Token viable with strong contract and public filing |

Banks running multi-country programs must confirm MLETR status for each jurisdiction on the route, not just the origin and destination. An intermediate jurisdiction, such as a transhipment port, can affect eBL enforceability even if it is not the final destination.

For the legal recognition framework, read MLETR, eBLs, and Warehouse Receipts: The Legal Layer Behind Tokenized Trade Collateral.

Inventory Token as a Layered Structure

Inventory tokens become more legally robust when they are explicitly layered over an underlying legal instrument rather than standing alone.

Three bridging structures increase token enforceability without requiring new legislation.

Token linked to underlying warehouse receipt. The token references the specific receipt by serial number and hash. Any transfer of the token is conditional on a corresponding transfer of the receipt in the recognized registry. If the linkage is documented in the pledge agreement and recognized registry, this structure can align the token holder’s rights with the receipt holder’s rights, subject to governing law.

Token linked to custodial acknowledgment. A licensed custodian confirms in writing that it holds goods on behalf of the token holder and will follow the token holder's instructions for release. This structure is stronger than a bare contractual claim but weaker than a document of title.

Token linked to public registry filing. The security interest is perfected by a public filing with respect to the token. The filing can help establish priority over later creditors, depending on local secured transaction rules and proper perfection. The combination of token tracking and public filing provides operational convenience with legal priority protection.

For the operational workflow, read Digital Warehouse Receipts for Bank Collateral: How the Workflow Works.

Decision Framework

Starting Condition | Recommended Document |

Licensed warehouse, domestic trade, MLETR-aligned | Electronic warehouse receipt |

International shipment, both ends MLETR-aligned | Electronic bill of lading |

International shipment, destination not MLETR-aligned | Paper bill of lading with bank endorsement |

Multiple storage locations, no formal receipts | Inventory token linked to public registry filing |

Pre-export commodity finance, MLETR corridor | eBL held by bank until arrival |

Uncertain legal environment | Warehouse receipt plus traditional security filing |

Assess Trade Document Tokenization With TokenMinds

Choosing the right document layer matters before any inventory tokenization program starts. A token cannot fix weak title, unclear pledge rights, or poor enforcement design.

TokenMinds helps trade finance and legal teams assess warehouse receipts, eBLs, inventory tokens, custody structures, registry filings, and corridor-specific enforceability.

Request a trade document tokenization assessment with TokenMinds. https://tokenminds.co/become-our-client/

Frequently Asked Questions

Q: What is the difference between warehouse receipts and bills of lading?

A: A warehouse receipt relates to goods stored in a warehouse. A bill of lading relates to goods received for shipment. In lending, a warehouse receipt is usually stronger for stored inventory. A bill of lading is more relevant for goods in transit.

Q: Which trade document proves control of inventory collateral?

A: It depends on where the goods are. A warehouse receipt can support control over stored goods. A bill of lading can support control over goods in transit. An inventory token only supports control when it is linked to a legal document, custody agreement, or perfected security interest.

Q: Can eBLs or warehouse receipts be tokenized for lending?

A: Yes, but the token should not stand alone. The safer structure links the token to a recognized warehouse receipt, eBL, custody acknowledgment, or registry filing.

Q: Can an inventory token replace a warehouse receipt as a document of title?

A: No, in most jurisdictions. A warehouse receipt may operate as a document of title where the governing law recognizes that status. An inventory token usually derives authority from contracts, platform rules, custody agreements, or public filings. Banks using tokens as the primary collateral instrument must stack legal title, security interest, and digital control through contract and public filing.

Q: What is the fastest enforcement path after borrower default?

A: A warehouse receipt with a correctly drafted tripartite agreement usually gives the clearest enforcement path. The bank may be able to instruct the warehouse directly and appoint a selling agent without first relying on a court process, depending on the governing law and warehouse cooperation. An eBL enforcement depends on carrier cooperation and destination port recognition. An inventory token requires a security agreement and, in most markets, formal enforcement proceedings.

Q: How does priority work when a token holder and a public registry filer claim the same goods?

A: The public registry filer typically wins in jurisdictions that base priority on filing order, unless the token holder also has a public filing that predates the competing creditor's claim. An unperfected token pledge is vulnerable to any creditor who files in the public system, and to good-faith purchasers in many markets.

References

UNCITRAL: Model Law on Electronic Transferable Records (MLETR). Covers transferable documents and instruments including bills of lading and warehouse receipts, defining control as the electronic equivalent of possession.

UNCITRAL and UNIDROIT: Model Law on Warehouse Receipts (2024). Supports the legal framework for warehouse receipt systems and secured inventory finance.