TL;DR

Tokenized receivables and inventory only become bank-usable collateral when approved credit policy becomes executable rules. This guide explains the eligibility checks, scoring logic, decision objects, governance controls, and system architecture banks need to automate those decisions.

Why Eligibility Rules Need Production Architecture

DTCC frames tokenized collateral around real-time mobility and capital efficiency. That framing assumes the bank can determine eligibility and value consistently through automated controls.

Most eligibility guides list rules in isolation. Production engines do not work that way. Rules depend on each other. Rules change over time. Rules sometimes conflict. The architecture must handle all three.

What Rules Should a Collateral Eligibility Engine Include?

Both asset types use similar rule categories. Their policy logic differs:

Rule Category | Receivables Logic | Inventory Logic |

Asset type | Approved invoice and receivable categories | Approved commodities, goods, and inventory classes |

Counterparty | Debtor rating, payment history, disputes | Warehouse operator, supplier, and custodian quality |

Ownership | Seller owns the receivable | Borrower owns or controls the goods |

Tenor or age | Remaining invoice maturity and overdue status | Inventory age, shelf life, and obsolescence |

Jurisdiction | Assignment and enforcement requirements | Title, warehouse receipt, and enforcement requirements |

Insurance | Credit insurance and policy validity | Property, storage, and transit coverage |

Pledge status | No prior assignment or duplicate financing | No existing lien or duplicate warehouse receipt |

Concentration | Debtor, sector, geography, and maturity limits | Commodity, warehouse, supplier, and location limits |

Valuation | Verified net invoice amount | Approved market price or appraisal value |

Haircut | Based on debtor, tenor, dispute, and concentration risk | Based on volatility, liquidity, age, and storage risk |

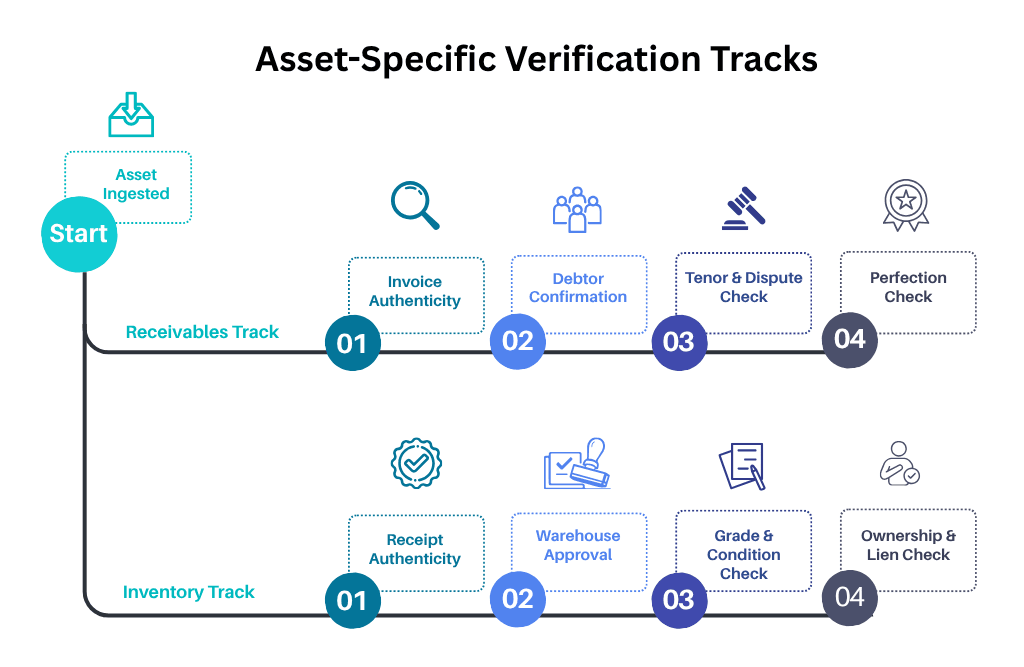

Receivables-Specific Checks

For tokenized receivables, the engine assesses invoice authenticity, debtor confirmation, due date, dispute status, dilution risk, credit quality, assignment perfection, duplicate financing, credit insurance, and concentration limits.

Inventory-Specific Checks

For tokenized inventory, the engine assesses approved inventory type, warehouse operator approval, receipt authenticity, ownership and control, existing liens, commodity grade and condition, age and obsolescence, valuation source, insurance validity, and concentration limits.

How Assets Are Scored for Lending

The eligibility engine produces a final lending outcome through a multi-stage calculation:

Hard-stop checks determine basic eligibility. Any hard-stop failure makes the asset ineligible.

Soft flags adjust the advance rate or haircut. These reduce lending value but do not reject the asset.

Concentration limits cap usable collateral. Even eligible assets may be partially excluded if limits are reached.

The engine calculates the final eligible value.

The engine records reason codes and review triggers.

Eligible Collateral Value Calculation

Eligible collateral value = the lower of (adjusted asset value) or (remaining concentration capacity)

The adjusted asset value uses:

Verified asset value × final advance rate

Note: The scoring examples below illustrate internal credit policy logic. They do not represent Basel-prescribed regulatory capital calculations.

Example for receivables:

Verified receivable value: $100,000

Base advance rate: 85%

Tenor adjustment: minus 5 percentage points

Debtor concentration adjustment: minus 10 percentage points

Final advance rate: 70%

Eligible collateral value: $70,000

Example for inventory:

Verified inventory value: $100,000

Base advance rate: 75%

Commodity volatility adjustment: minus 10 percentage points

Warehouse concentration adjustment: minus 5 percentage points

Final advance rate: 60%

Eligible collateral value: $60,000

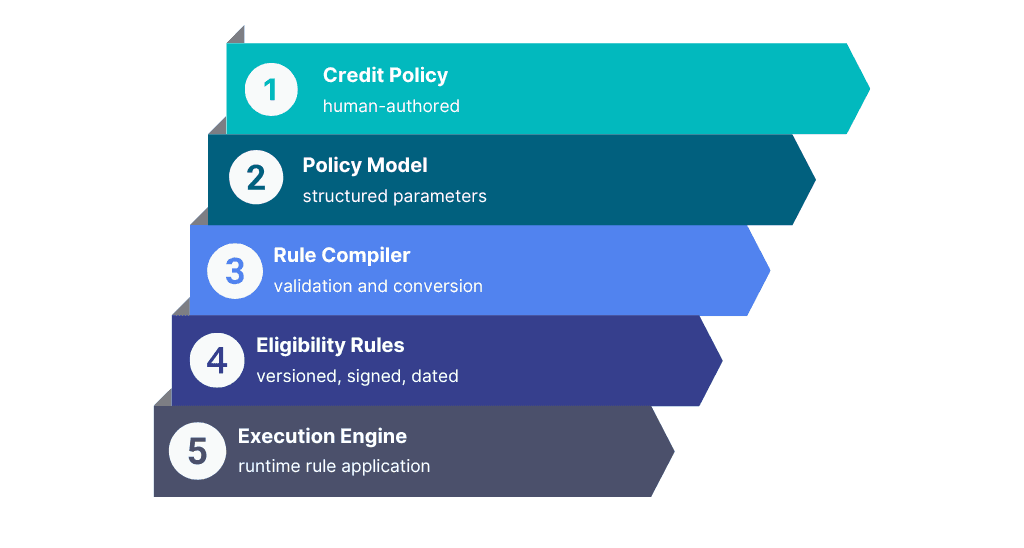

The Policy-to-Rule Compilation Layer

Most implementation guides start with executable rules. They skip the layer that creates them. In production systems, a human-readable credit policy document cannot go directly into an execution engine. An intermediate compilation layer bridges the gap.

The compilation path runs in five stages.

Credit policy. A non-technical document authored by the credit committee. It defines eligibility conditions in plain language. E.g. “Receivables from debtors rated below BB are not eligible”.

Policy model. This is a structured representation of the policy. It converts plain language into defined parameters. The policy model gives each rule a name, an ID, its inputs, thresholds and whether it is a hard stop or soft flag.

Rule compiler. A system component that converts the policy model into executable rule objects. The compiler validates that each rule references valid input fields and that thresholds are within defined system bounds. Rules that fail validation are returned to the policy team before deployment.

Eligibility rules. The compiled, validated rule set ready for the execution engine. Each rule is versioned, signed, and assigned an effective date.

Execution engine. The runtime component that applies rules to incoming assets and produces decision objects.

This layer matters for two reasons. First, it creates a traceable path from board-approved credit policy to automated decision. Second, it prevents unreviewed rule changes from entering production. A rule that bypasses the compiler and goes directly into the execution engine is a governance failure.

Rule Version Lifecycle Management

Production governance requires a full version lifecycle.

Version State | Engine Behavior | Use Case |

Draft | Not executable | Policy authoring and review |

Approved | Staged for deployment | Pre-production testing |

Effective | Applied to all new assets | Normal operations |

Sunset | Applied only to pre-cutoff assets | Transition period management |

Rollback | Prior version reinstated | Defective rule remediation |

Historical replay | Past version re-executed on demand | Regulatory audit and dispute resolution |

Historical Replay Requirements

When the bank retains the original rule version, asset inputs, external data snapshots, model version, and portfolio state, replay should reproduce the original result. Some historical inputs may be unavailable. The system should identify each missing record. It should then explain any replay difference. This supports regulatory auditability, model governance, and dispute resolution.

The Rule Dependency Graph

Rules execute according to defined dependencies. Independent checks may run in parallel, while dependent rules wait for upstream results. Hard-stop failures end the eligibility process and route the asset to the remediation queue. Soft flags allow processing to continue while adjusting the haircut, advance rate, or approval status, and route to the exception queue.

Each node produces a rule result with an outcome, reason code, and supporting evidence. The engine combines these results into the final eligibility decision object.

For the receivables verification checklist that feeds the ownership node, read: What Data Must Banks Verify Before Tokenizing Accounts Receivable?

For the inventory verification checklist, read: How Banks Verify Inventory Ownership and Control Before Tokenization.

After asset-specific verification, both tracks move through jurisdiction, insurance, valuation, haircut, concentration, pledge status, and final decision checks.

Deterministic Conflict Resolution

Real engines encounter conflicting outcomes. Two rules may produce contradictory results for the same asset. The engine needs a defined resolution mechanism, not a runtime error.

Example conflict: A debtor has strong credit quality, but the sector concentration limit is almost reached. The asset may remain individually eligible, while only part of its value contributes to the borrowing base.

Concentration and credit quality are not necessarily conflicting rules. Credit quality affects asset-level risk. Concentration limits the asset’s portfolio contribution.

Conflict Type | Resolution Mechanism | Example |

Concentration vs credit quality | Rule precedence, concentration wins | High-rated debtor blocked by sector cap |

Multiple soft flags produce different adjustments | Policy-defined combined adjustment | Highest, additive, or capped adjustment applied |

Legal perfection failure vs strong rating | Non-overridable hard stop, perfection failure wins | Asset ineligible regardless of rating |

Several soft flags may apply together. The policy must define their combined effect. The engine may use the highest adjustment, additive overlays, or a capped cumulative reduction. The calculation must not weaken a mandatory limit.

Decision Object Design

The final eligibility decision object is divided into core decision fields and audit/replay fields.

Eligibility Decision Fields

Field | Purpose |

asset_id | Identifies the invoice or inventory lot |

asset_type | Selects the applicable rule set |

policy_version | Records the approved credit policy |

rule_set_version | Supports audit and historical replay |

eligibility_status | Eligible, conditional, or ineligible |

verified_value | Records the accepted asset value |

final_advance_rate | Records the approved lending percentage |

final_haircut | Records the applied risk adjustment |

eligible_value | Records the final borrowing-base contribution |

failed_rules | Identifies failed hard-stop checks |

reason_codes | Explains reductions or rejection |

evidence_references | Links the decision to supporting data |

decision_timestamp | Records when the decision was produced |

next_review_date | Defines the next reassessment |

override_status | Records approved exceptions |

Audit, Replay, and Exception Fields

Field | Purpose |

model_version | Identifies the valuation or scoring model |

input_snapshot_id | Links to the original asset inputs |

market_data_snapshot_id | Links to the historical valuation data |

portfolio_snapshot_id | Records the concentration state used |

exception_expiry | Records when a conditional approval ends |

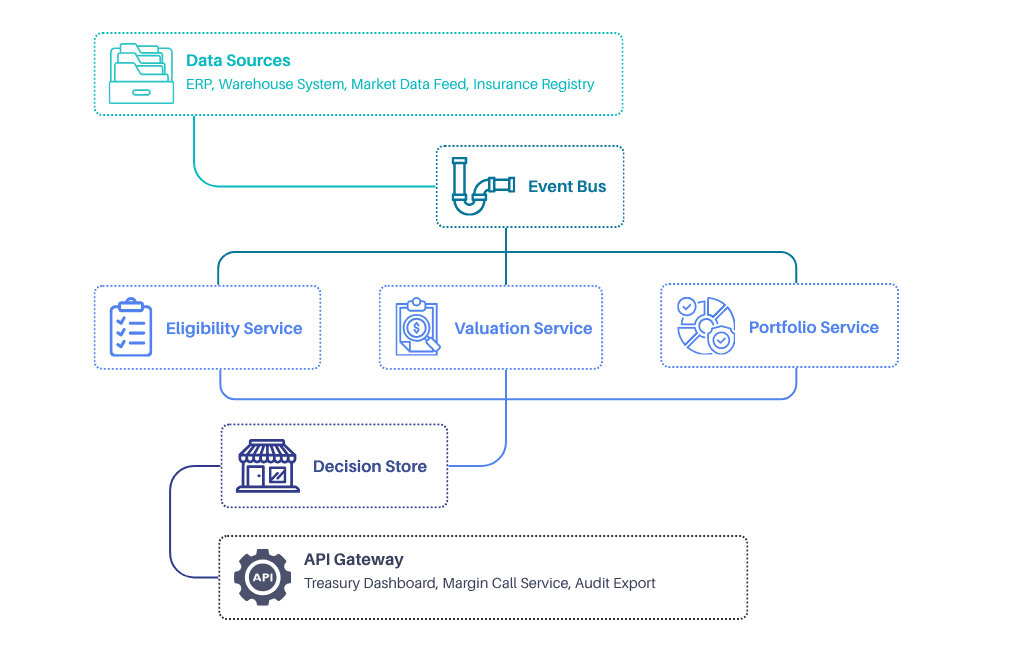

Distributed Service Architecture

The event bus is the communication layer. The services behind it define the system boundaries.

Eligibility Service. Executes the dependency graph for individual assets. Produces decision objects. The Eligibility Service routes overrideable soft flags to the exception queue. Non-overridable failures enter a remediation queue for correction and reassessment.

Valuation Service. Maintains current asset values from market data feeds. Posts valuation events on the event bus when prices move beyond pre-configured thresholds.

Portfolio Service. Runs concentration checks, cheapest-to-deliver selection, and substitution optimization across the full pool. Consumes eligibility and valuation events.

Decision Store. Persists all decision objects immutably. Supports historical replay queries. Feeds the audit export function.

API Gateway. Provides portfolio data and eligibility status to downstream systems. The API gateway enforces role-based access for downstream systems.

Each service has a defined boundary. The Eligibility Service does not access the Decision Store directly. It publishes events. The Decision Store consumes them. This separation prevents the execution layer from modifying its own audit record.

Exception Governance Workflow

Manual override. A collateral officer can override a soft-flag decision. A second risk officer must approve. The override reason is logged. Hard-stop decisions cannot be overridden manually.

Temporary policy exception. The credit committee approves a time-limited exception. Temporary exceptions may apply only to rules marked as overrideable in the policy model. Ownership, legal perfection, duplicate pledge, and other non-overridable failures remain ineligible until the underlying issue is corrected. The engine records the asset as conditionally eligible under the approved exception until its expiry date. At expiry, the full dependency graph re-runs automatically. The decision object should retain the original rule failure, the exception approval, the approving officers, the expiry date, and the adjusted eligible value.

Override expiry. Override duration should be configurable by asset type, risk level, and exception category. For example, a bank may set a 30-day maximum for selected credit exceptions. Missing legal, ownership, pledge, or mandatory insurance evidence should route the asset for correction and reassessment. It should not create temporary collateral value. Automatic renewal is not permitted.

Escalation. Assets in the exception queue beyond a configurable period (e.g., 5 business days) escalate automatically to the credit committee. The escalation deadline should be configurable by exception type and risk level. The escalation is recorded in the exception audit trail. The engine creates a new decision object only when the eligibility outcome changes.

Operational Scale Considerations

Idempotent event processing. Each event carries a unique ID. If the same event is delivered twice, the engine processes it once and discards the duplicate. This prevents double-scoring on retry.

Partial graph execution. Re-scoring runs only the affected nodes. A price movement re-runs valuation, haircut, and concentration nodes. It does not re-run ownership or legal perfection checks. This reduces latency on re-score events.

Latency targets. A single-asset eligibility decision should complete in under one second (illustrative service-level objective). A full portfolio re-score after a concentration change should complete in under 60 seconds for a pool of 1,000 assets (illustrative service-level objective).

Horizontal scaling. The Eligibility Service scales horizontally. Each instance processes a separate queue partition. The Decision Store needs to support concurrent writes from multiple instances without record conflicts.

For haircut calculation and advance rate logic across asset types, read: How Haircuts, Advance Rates, and Concentration Limits Work for Tokenized Trade Collateral.

Design a Bank-Grade Eligibility Engine With TokenMinds

A collateral eligibility engine must do more than execute technical rules. It must translate credit policy into clear asset checks, risk adjustments, decision outputs, and exception workflows.

TokenMinds helps banks define eligibility rules for receivables and inventory. The process can cover policy modelling, hard stops, soft flags, evidence requirements, concentration limits, haircut logic, decision objects, governance, and system architecture.

Schedule an eligibility rules design session with TokenMinds.

Frequently Asked Questions

Q: How do banks define eligibility for tokenized collateral?

A: Banks convert approved credit policy into hard stops, soft flags, valuation rules, concentration limits, evidence requirements, and review triggers. Tokenization records the asset and its control status, but it does not make the asset eligible by itself.

Q: What rules should a collateral eligibility engine include?

A: The engine should assess asset type, ownership, debtor or warehouse quality, tenor, jurisdiction, insurance, valuation, concentration, legal perfection, and existing pledge status.

Q: How can tokenized receivables and inventory be scored for lending?

A: The engine first applies hard-stop rules. It then uses risk adjustments to calculate the final advance rate, haircut, eligible value, decision status, and reason codes.

Q: How does the system prevent duplicate processing of the same external event?

A: Each event should carry a unique identifier. The consuming service checks that identifier against an idempotency store before creating a decision object. Previously processed events are ignored or linked to the existing result. This design helps prevent retries from creating duplicate eligibility decisions.

Q: What if we need to roll back a rule after incorrect decisions have been made?

A: The defective rule version is rolled back to the previous version. All decisions made under the defective version are flagged in the Decision Store. The historical replay feature re-runs these decisions with the correct previous version. The difference between the original outcome and the replayed outcome indicates what assets need remediation.

Q: How does the policy-to-rule compilation layer prevent unauthorized rule changes?

A: Rules must pass through the compiler before they can enter the execution engine. The compiler validates each rule against defined system bounds. Rules that bypass the compiler cannot be executed. The deployment workflow requires recorded credit committee approval. The compiler then performs technical validation. This creates a two-step gate: policy approval and compiler validation.

References

DTCC: "Tokenized collateral could unlock billions in capital and transform liquidity management" (2026). Frames tokenized collateral around real-time mobility, capital efficiency, and risk management. https://www.dtcc.com

UNCITRAL: Model Law on Electronic Transferable Records (MLETR). Provides framework for electronic trade document recognition and control. https://uncitral.un.org/en/texts/ecommerce/modellaw/electronic_transferable_records

UNCITRAL-UNIDROIT: Model Law on Warehouse Receipts (2024). Supports legal framework for warehouse receipt systems and secured inventory finance. https://uncitral.un.org/en/mlwr

Basel Committee on Banking Supervision: Principles for the Management of Credit Risk (2025). Provides guidance on credit risk governance, portfolio limits, and monitoring. https://www.bis.org/bcbs