Key takeaways:

TMX Agentic Finance enables near-instant cross-border payments using stablecoins, automating wallets, conversion, transfers, and off-ramps through a single secure integration.

Replace chains with stablecoin rails to move funds in minutes instead of days, cutting intermediary fees and manual reconciliation while keeping compliance and custody controls intact.

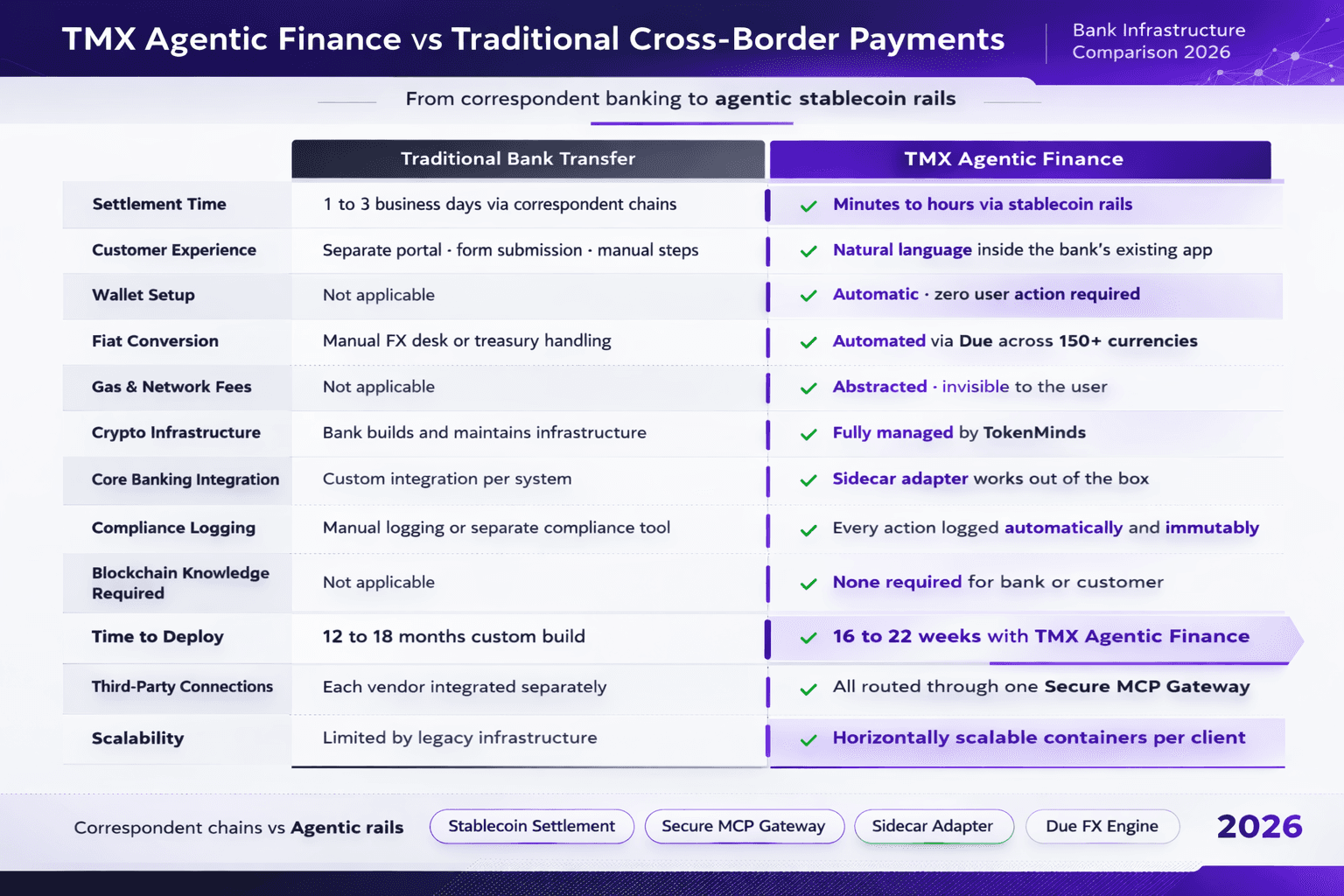

Compared to traditional correspondent banking, banks can reduce settlement time by over 99%, cut transfer costs by nearly half, and significantly lower reconciliation workload, with full deployment achievable in 16–22 weeks.

Cross-border payments are slow. Customers wait days for transfers to settle. Banks use long chains of intermediaries. Each hop adds cost and time. The process is frustrating for customers and expensive for banks.

The root cause is simple. Banks lack the infrastructure to connect their existing systems to modern payment rails. Building that infrastructure from scratch takes years and millions of dollars.

TMX Agentic Finance fixes this. It gives banks an AI agent that handles cross-border payments through crypto. Stablecoins act as the settlement layer. Fiat conversion happens automatically. Everything runs through one secure connection into the bank's existing system.

The Problems with Traditional Current Cross-border Payment

Global payments were built for a different era, and that legacy design now makes cross-border transfers slow, expensive, and opaque. What appears to be a simple international transfer is actually a fragmented chain of intermediaries, manual processes, and disconnected systems.

Settlement takes days

Correspondent chains add cost at every hop

Customers lack transparency

Currency conversion is fragmented

Banks face operational complexity

The root issue is infrastructure. Most banks cannot directly connect legacy systems to modern crypto payment rails.This creates a structural barrier to modernization.

What is TMX Agentic Finance

TMX Agentic Finance is an AI platform for banks and financial institutions. It is built by TokenMinds, an ISO 27001-certified firm with eight-plus years in Web3 and AI. Over 200 organizations trust TokenMinds, including Khan Bank, KuCoin, and CoinMarketCap.

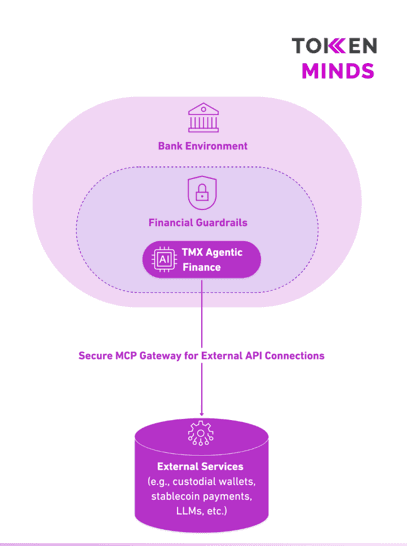

The platform sits between the bank's app and the execution layer. That layer includes blockchain networks, crypto custody providers, and fiat payment services. A Secure MCP Gateway connects all of them. The bank connects at one point. The platform handles everything else.

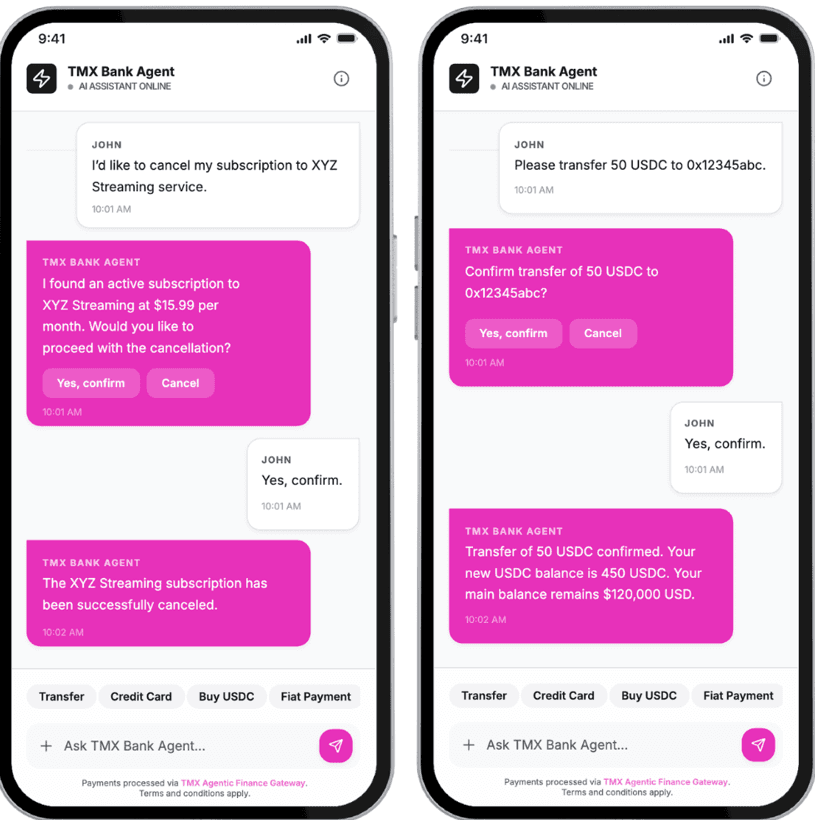

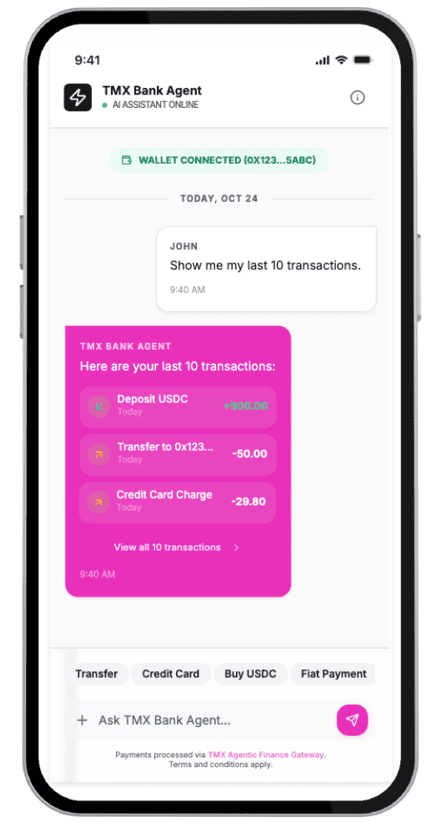

The customer experience is simple. A user types what they want. The TMX Bank Agent reads the request, executes the steps, and confirms when it is done. No separate portal. No manual steps. No blockchain knowledge needed.

How Cross-Border Payments Work Through TMX Agentic Finance

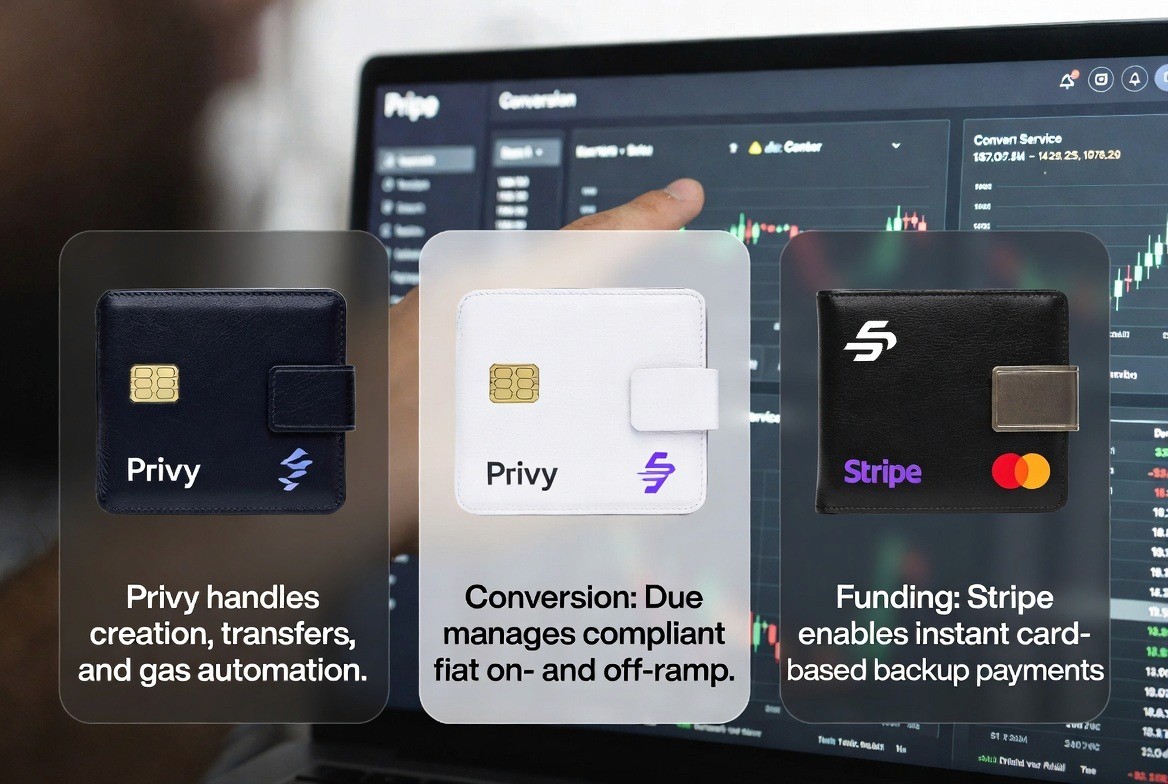

A payment through TMX Agentic Finance uses stablecoins like USDC as the settlement layer. Fiat converts to stablecoin at the source. The stablecoin moves across the blockchain to the recipient. It converts back to local fiat at the destination. Three modules make this work: Privy for wallets, Due for fiat conversion, and Stripe as a backup for card-based funding, a flow implemented in this agentic crypto payment integration model.

Step 1: Wallet Provisioning

User-initiated payments begin as soon as the user begins their first crypto-payment transaction; at that time the agent will verify if the user has been provided with a provisioned wallet. The agent will then call Privy (programmatically) in order to create the provisioned wallet on the back end of the application. The process of creating this wallet does not expose the seed phrase of the wallet to the user. In addition, the user is not required to take any actions to be able to use their provisioned wallet.

The platform uses a unique (1:1), persistent mapping of the users' bank-provided User ID to a blockchain-based wallet address.

The authentication for access to the platform is provided exclusively through the bank's current login system using JWT and OIDC.

Users are not exposed to any private keys

Step 2: Fiat-to-Crypto On-Ramp

If the user’s wallet does not contain sufficient stablecoin to complete the transaction the agent will call Due to process a fiat-to-cryptocurrency conversion. Due currently supports ACH in US based accounts; SEPA in EU; SWIFT and Virtual IBAN for over 150 fiat currency conversions.

The agent will then display a quote that includes the exchange rate and the fees associated with the transaction; request confirmation of the quote; and after confirmation execute the transfer from the users bank account to their Privy wallet as USDC or EURC.

Settlement of the transaction typically occurs within minutes to hours dependent upon the banking networks involved.

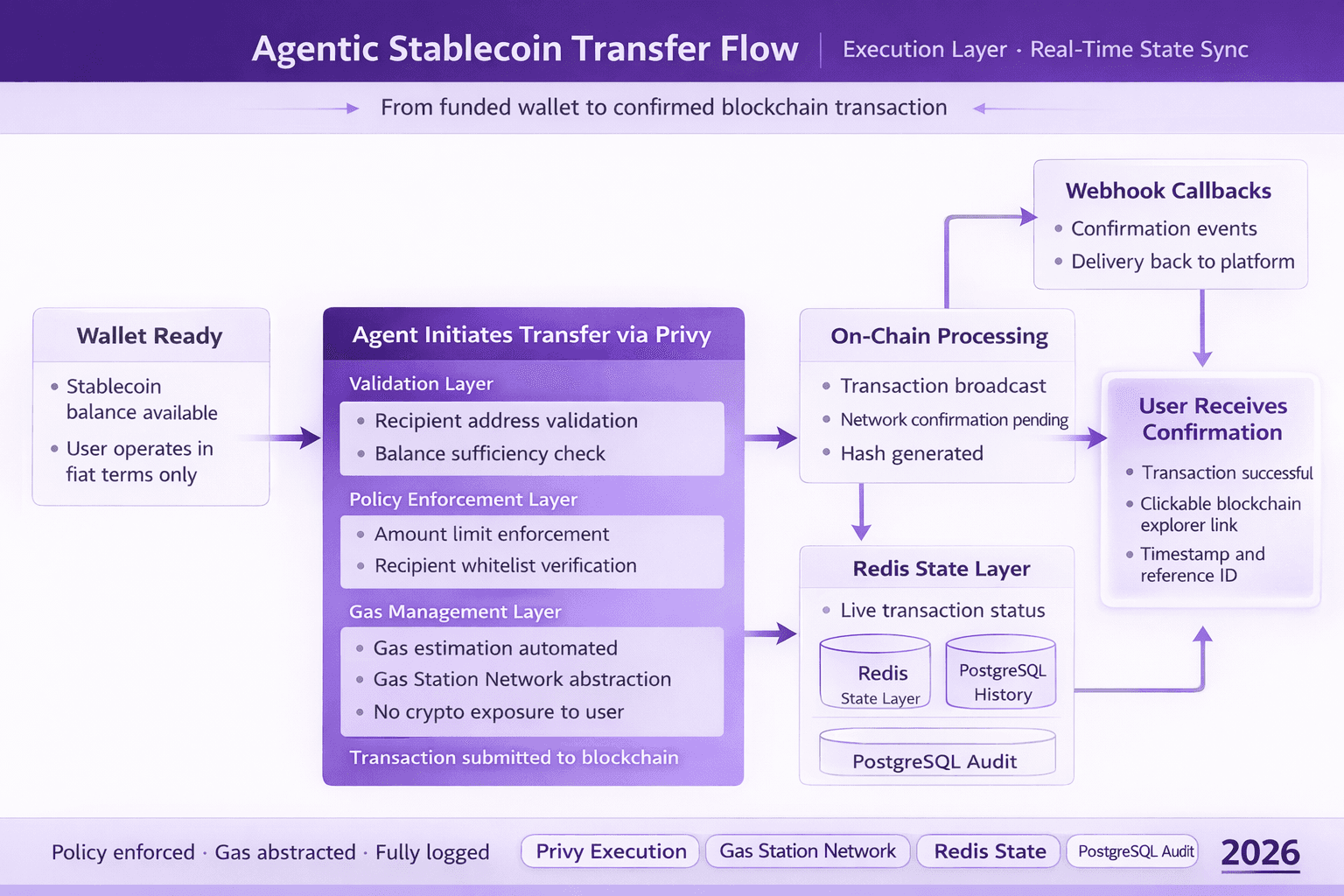

Step 3: Cross-Border Transfer

Once the wallet is funded, the agent uses Privy to execute the blockchain transfer. The agent checks that the recipient address exists, that there are sufficient funds available in the sender’s account, that it follows all of the configuration defined for transactions (e.g., how much money can be transferred, if the recipient has been “whitelisted” etc.), Privy automatically estimates the gas fees required using the Gas Station Network so that end-users never have to worry about converting between fiat or stablecoin and cryptocurrency, and finally Privy sends the transaction.

All status information flows from Privy back to the user platform via webhooks into the Redis state layer and PostgreSQL history layer.

When the transfer is complete the user receives a confirmation email with a link to view the transaction.

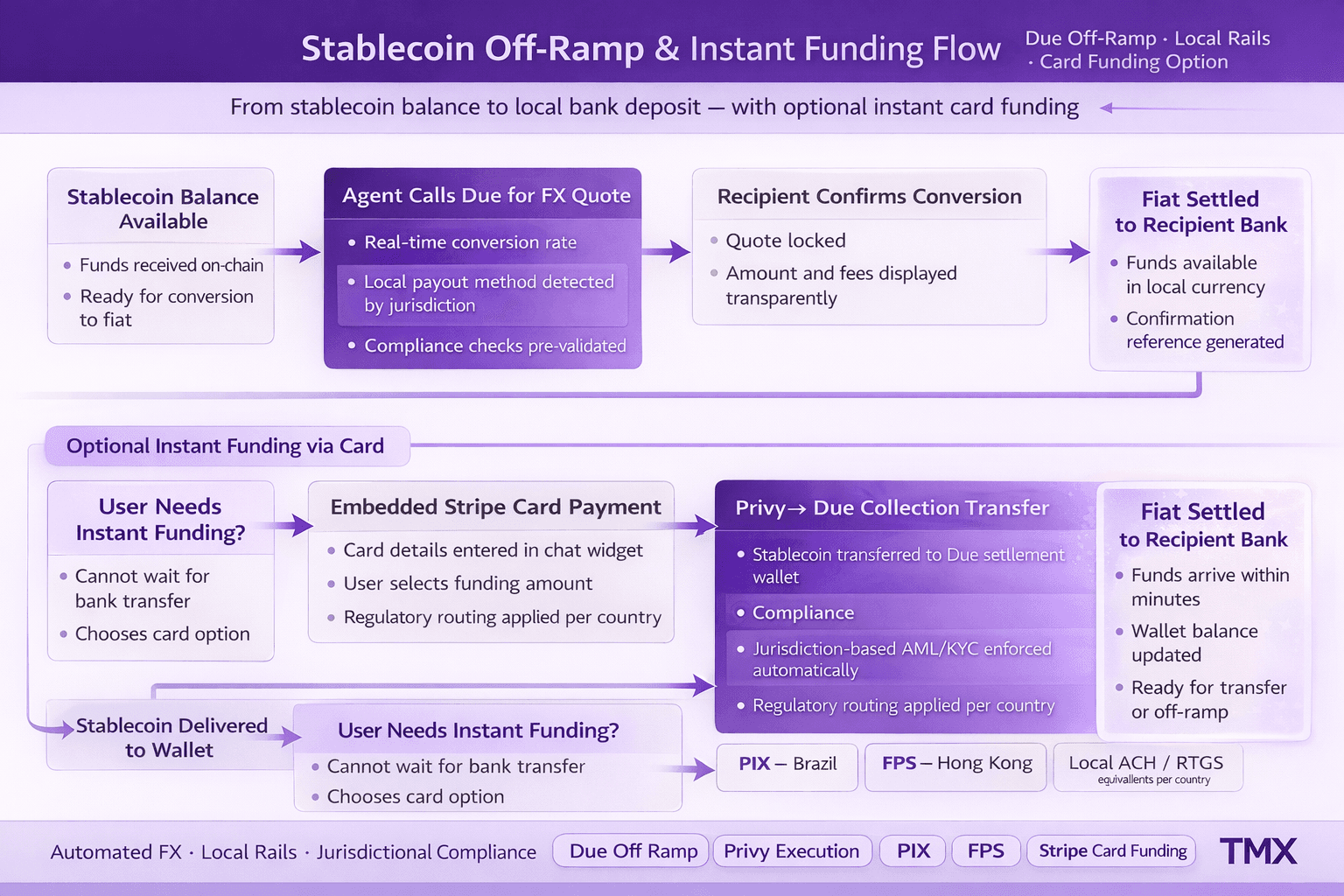

Step 4: Crypto-to-Fiat Off-Ramp at Destination

On the recipient side, they can redeem their StableCoin into fiat money via Due’s Off-Ramp. The Agent sends a request to Due to receive a Quote, receives confirmation from Due, then sends the Privy-to-Due Collection Transfer and makes the Bank Deposit.

The Bank Deposit will take 1-3 Business Days to reach the Recipient’s Bank Account.

Due offers local Payment Methods by Jurisdiction (i.e. PIX in Brazil, FPS in Hong Kong), and Due also automatically handles Compliance by Jurisdiction.

PS: Card-Based Funding via Stripe. If a user needs instant funding and cannot wait for a bank transfer, the agent offers a Stripe option. A card payment widget appears in the chat. The user enters card details, picks an amount, and crypto arrives in their wallet within minutes. This costs around 3% in card processing fees.

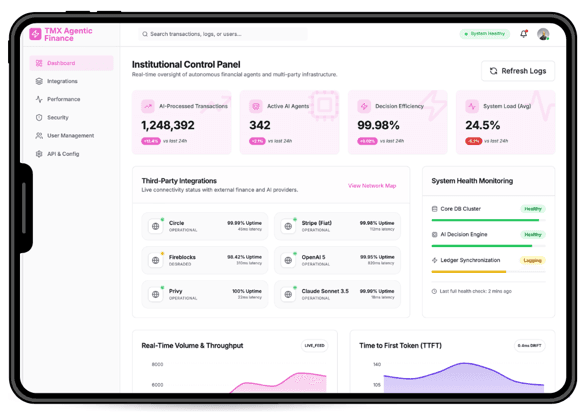

The TMX Agentic Finance Architecture

1. TMX Agent Core

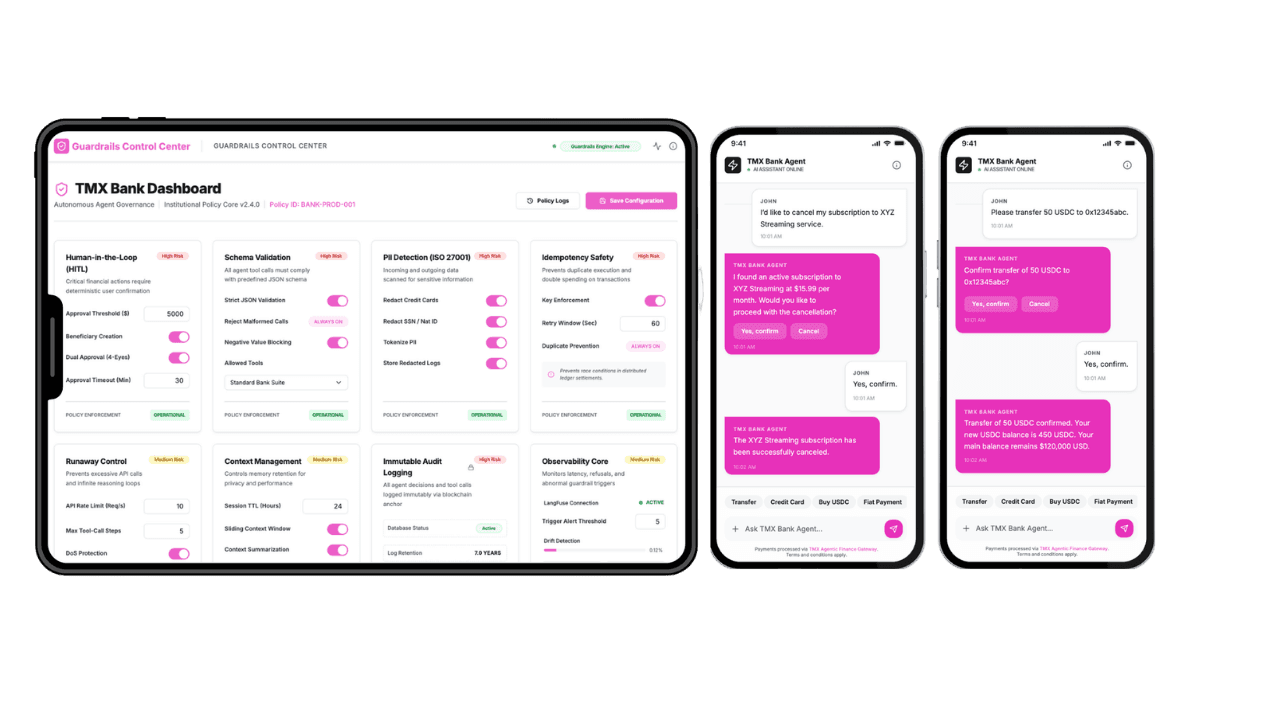

The Agent Core is the brain of the system. It runs on LangGraph, a state machine built for complex multi-step operations. It receives instructions in plain language. It reasons through the required steps. It sends commands to the Secure MCP Gateway. It logs every decision. It does not execute anything directly. It decides, directs, and records.

Each bank can configure the agent with its own persona, workflows, and compliance rules. No changes to the Agent Core are needed to do this.

2. Secure MCP Gateway

The Gateway connects the Agent Core to all external services. The agent calls one standardized endpoint. The Gateway routes each call to the right service, whether that is Privy for wallet operations, Circle or Stripe for payments, or a third-party AI provider. The bank's team never manages vendor APIs, API keys, or rate limits. The Gateway handles all of it.

The Gateway also strips out sensitive user data before it reaches any external system. It logs every action for compliance audits. It validates every input and output to prevent unauthorized actions.

3. Core Banking Sidecar

The Sidecar connects TMX Agentic Finance to the bank's existing core banking system. It is a custom adapter built for each client. It translates between the bank's legacy formats, such as ISO 20022 or ISO 8583, and the platform's standard format. The bank does not replace its core system. The Sidecar bridges the gap invisibly.

4. Managed Custody

Banks without existing crypto infrastructure use the platform's Managed Custody model. Every bank user gets a blockchain wallet linked to their account ID. Private keys stay in a Trusted Execution Environment. They are never exposed to the application or any third party. Users deal only in fiat and stablecoin terms. No crypto knowledge is required.

The Three Integration Partners

Privy handles wallets and crypto operations. It creates wallets server-side, checks balances, executes transfers, enforces transaction policies, and manages gas fees automatically. Privy was acquired by Stripe in 2025.

Due handles fiat conversion. It converts fiat to crypto on the way in and crypto to fiat on the way out. It supports 150-plus currencies, local payment methods by jurisdiction, and handles compliance per country automatically.

Stripe handles card-based funding as a backup. It is used when a user needs instant funding or is in a region where Due has limited coverage. It supports major cards, Apple Pay, Google Pay, and assets including USDC, USDT, ETH, and BTC.

All three run as independent modules behind the Secure MCP Gateway. Any module can be added or removed through configuration. No redeployment of the Agent Core is needed.

Quantified Performance Benchmarks

The performance gains are measurable, not theoretical.

Internal pilot simulations across live payment corridors show three clear results versus traditional correspondent banking.

Settlement time. Average settlement across the US-Brazil corridor dropped from 2.7 business days to 11 minutes. That is a reduction of over 99%.

Operational cost. Cost per transfer fell by 48% compared to correspondent routing through three intermediaries. The savings came from eliminating intermediary fees and manual FX handling.

Reconciliation overhead. Reconciliation workload dropped by 72%. Immutable, automatically generated transaction logs replaced manual audit processes entirely.

These results came from three things working together: stablecoin settlement rails, automated fiat conversion via Due, and end-to-end logging across the platform.

For banks processing high volumes of cross-border transactions, the impact on operational cost and back-office workload adds up fast.

Timeline and Deployment Options

Deployment Options

1. Managed AWS Cloud

It gives each client a fully isolated environment. No shared infrastructure. No other bank's data in the same cluster. The platform runs on AWS App Runner, ECS Fargate, or Kubernetes depending on the workload.

PostgreSQL handles payment history and audit logs. Redis handles live session state.

The bank's core banking system connects through AWS PrivateLink or a VPN tunnel. Data never travels over the public internet.

TokenMinds manages the infrastructure. The bank's team does not need to monitor containers, patch servers, or manage uptime.

This is the fastest path to production and works well for most institutions.

2. On-Premise or Private Cloud

It runs the full platform on the bank's own Kubernetes cluster. The bank owns and controls every component. Payment data never leaves the bank's environment. This option is built for institutions that cannot store data outside their own infrastructure due to regulation, internal policy, or market sensitivity.

It requires outbound internet access for LLM API calls and connections to external services like Circle and Fireblocks.

If the bank cannot allow outbound access, local LLMs can be configured as a replacement.

TokenMinds provides the deployment pipeline and supports the setup, but the bank's team operates the cluster day to day.

Timeline

Sandbox Pilot

Sandbox is where integration starts. The platform connects to 3 to 5 external services, typically Privy, Due, and the bank's core banking system via the Sidecar. All core payment flows run against live APIs, not mock environments.

These capabilities include wallet provisioning, fiat-to-crypto conversion, stablecoin transfers and off-ramp flows. The Agent Core, Secure MCP Gateway, Sidecar and core banking connection are tested collectively.

At the end of the process, the bank’s team will receive integration test results and deployment documentation via the real time chat UI.

Timeline: 6 to 8 weeks.

Production Deployment

It is the full build into live operations. The Sidecar is fully integrated with the bank's core banking system. All active third-party services are connected and tested at production scale. The platform goes through performance optimization and stress testing to confirm it can handle live transaction volumes.

Monitoring is set up for continuous operation after launch. Compliance rules are configured per active payment corridor. At handover, the bank receives a post-deployment performance report and full documentation. Timeline: 10 to 14 weeks.

Total time from decision to live across both phases: 16 to 22 weeks. The longest lead time is usually not the platform itself. It is the legal and API agreements with external service providers like Privy and Due. Starting the sandbox immediately compresses the overall timeline because those agreements can be negotiated in parallel.

Case Example: European Bank Expanding into LATAM

A regional European bank with 4,200 SME clients had a problem. Supplier payments to Brazil were slow. Transfers moved through a three-hop SWIFT chain and took nearly three business days. FX spreads were unclear. Payment complaints were frequent.

The bank had no blockchain team. They needed a solution that worked inside their existing mobile app and ISO 20022 core system.

The bank deployed TMX Agentic Finance in 18 weeks. The Core Banking Sidecar connected to its existing system without changes. Due handled SEPA on-ramp in Europe and PIX off-ramp in Brazil. Privy created wallets automatically for SME users, with no crypto knowledge required.

Now, SME clients simply enter payment instructions in the bank app. The agent confirms the rate, executes a stablecoin transfer, and triggers a PIX deposit in Brazil within minutes. In the first quarter after launch, the bank processed €34M in new corridor volume, reduced supplier complaints by over 80%, and eliminated manual FX reconciliation work. The same setup is now expanding to Mexico and Colombia without redeploying the platform.

Table of comparison: TMX Agentic Finance vs. Traditional Cross-Border Payments

Regulatory Model by Jurisdiction

TMX Agentic Finance works within existing laws in each payment corridor. The bank keeps full ownership of its customers and stays responsible for compliance. The platform provides execution and infrastructure. It does not act as a regulated financial intermediary.

In the EU, USDC and EURC are issued by Circle under regulated frameworks. SEPA on-ramp and off-ramp flows run through Due, which holds the required licenses.

In Brazil, PIX payments run through Due's licensed partners. Local compliance checks run automatically.

In the US, ACH flows operate under Due’s licenses, and Stripe supports card funding where needed. The bank does not need to register as a money services business because licensed partners handle conversion and transmission behind the Secure MCP Gateway. For stricter data rules like GDPR or PDPA, the platform can run on-premise so payment data stays inside the bank’s infrastructure. New corridors can be added by updating rules in the Gateway without rebuilding the system.

Risk Mitigation Framework

TMX Agentic Finance reduces the key risks tied to stablecoin payments.

Stablecoin risk. Only assets like USDC are used. USDC is backed by cash and short-term US Treasuries with published reserve reports. Banks can restrict which stablecoins are allowed based on internal policy. No algorithmic stablecoins are used by default.

Liquidity risk. Due handles the main fiat conversion. Stripe acts as a backup. The Gateway switches providers automatically if one fails. No manual intervention required.

Blockchain congestion. Gas management and multi-chain routing are automated. Users never deal with network issues directly.

Custody risk. Private keys are stored in a Trusted Execution Environment. They are never exposed at any point in the transaction flow.

Operational continuity. Live session data and audit logs are stored separately. Transactions are recoverable even if part of the system fails.

Conclusion

Banks that deploy TMX Agentic Finance can offer cross-border payments through crypto rails without building or managing blockchain infrastructure. The wallet layer, fiat conversion, gas management, custody, and audit logging are all handled by the platform. The bank connects at one point and configures the agent's workflows. Everything else is abstracted away.

The result is a cross-border payment experience that settles on stablecoin timelines, not correspondent bank timelines. It runs inside the bank's existing app, under the bank's brand, with a natural language interface the customer already knows how to use.

Frequently Asked Questions

What is AI for cross-border payments?

AI for cross-border payment is technology that uses artificial intelligence to send money between countries faster and more easily by automating currency exchange, checks and transfers.

Does TMX Agentic Finance replace the bank's core banking system?

No. The platform connects to the bank's existing core system through a Custom Core Banking Sidecar. The Sidecar translates between the bank's legacy formats and the platform's standard format. The bank keeps its current infrastructure. Nothing gets replaced.

Does the bank need a blockchain or crypto team to deploy this?

No. TokenMinds manages all the blockchain infrastructure. The bank's team connects at one integration point. The platform handles wallet provisioning, gas fees, transaction signing, and blockchain node communication. No crypto expertise is required on the bank's side.

How does the platform handle user wallets?

Each User will have a Blockchain Wallet tied to their Bank Account ID which will be automatically generated upon their first Transaction. The Private Keys for each user wallet are kept within a Trusted Execution Environment (TEE) and will never be made available to the Application, the User nor any Third Party. Users will never receive a Seed Phrase nor a Wallet Address except if they request it.

What currencies and payment rails does it support?

The platform is able to support over 150 plus fiat currencies via the Due (payment) platform. The payment rail options available via the Due (payment) platform are ACH for U.S. accounts; SEPA for EU accounts; SWIFT; and Virtual IBANs. In addition, local payment method(s) are also accepted per jurisdiction. For example, PIX is accepted in Brazil; and FPS in Hong Kong. On the crypto side of the platform, the currently supported crypto chains are EVM-based and include assets such as USDC, USDT, EURC, ETH, and BTC.

What happens if a user needs to fund their wallet instantly?

If the user cannot wait for a bank transfer, the agent offers a Stripe card-based on-ramp. A payment widget appears directly in the chat interface. The user pays with a debit or credit card, Apple Pay, or Google Pay. Crypto arrives in their wallet within minutes. This option carries a card processing fee of approximately 3%.

How is user data protected?

The Platform complies with ISO 27001. All sensitive information such as account number and personal identifiers are identified and removed by auto-detecting and removing this information prior to it being sent to any external LLM or third party service. All actions and all tool calls are logged in an immutable format for audit purposes. All communications between components of the Platform are encrypted and authenticated. Only whitelisted IP addresses will be allowed to connect to the Platform.

Can the bank customize how the agent behaves?

Yes. Banks configure the agent without having to access the Agent Core.

Each bank can customize the persona, conversation flow, approval workflow, and compliance requirements. The banks can also decide how they will deploy the agents depending upon their specific business model such as deploying an agent that is a payment concierge, a financial advisor, or a simple transfer assistant. Multi-step custom approval processes are configurable for high value transaction approval processes.

Is the platform hosted in the cloud or on-premise?

Both options are available. The Managed AWS Cloud option deploys in a fully isolated single-tenant environment per client. The On-Premise option deploys on the bank's own Kubernetes cluster for institutions that require full data sovereignty. The bank chooses the model that fits its regulatory and infrastructure requirements.

How long does it take to go live?

The Sandbox Pilot takes 6 to 8 weeks. The full Production Deployment takes 10 to 14 weeks. Total time from decision to live is 16 to 22 weeks. The longest lead time is typically the legal and API agreements with third-party service providers, not the platform itself. Starting the sandbox early compresses the overall timeline because those agreements can run in parallel.

What ongoing support does TokenMinds provide after deployment?

TokenMinds will provide both post-deployment monitoring and a Performance Report at the completion of the Production Deployment phase. For Managed AWS Cloud option TokenMinds will manage the infrastructure going forward. The Bank will be charged a monthly fee for the use of interoperability, as applicable. For On-Premise deployments, TokenMinds will assist in setting up the deployment pipeline, and then support to set it up; after that the bank is responsible for its day-to-day operation.