Key Takeaways

The Fed, FDIC, and OCC confirmed that tokenized securities receive the same capital treatment as traditional securities, removing a major regulatory barrier and opening the door for banks to adopt tokenization infrastructure.

For financial institutions, tokenization can improve settlement speed, collateral mobility and operational efficiency while maintaining the same legal rights, compliance controls, and risk management frameworks used in traditional finance.

Institutions typically implement tokenized securities infrastructure through four systems: compliant issuance, wallet compliance screening, automated reconciliation between on-chain transactions & internal records, and settlement through atomic delivery-versus-payment.

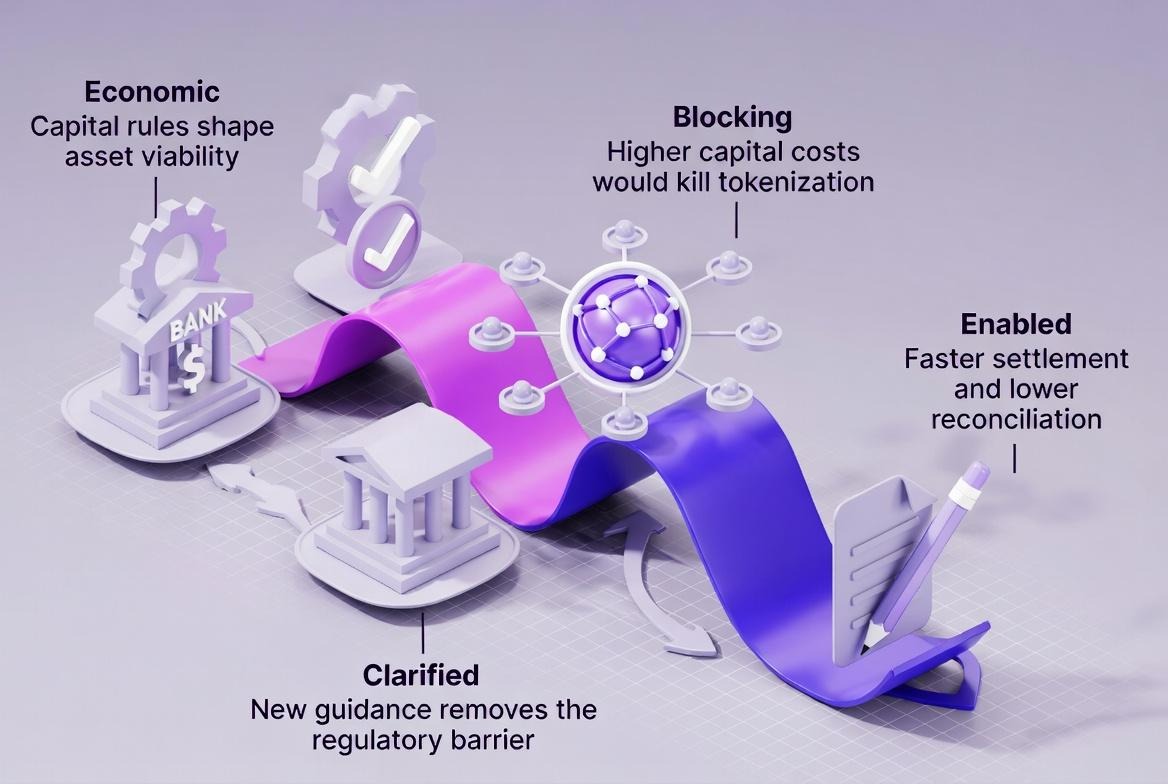

For years, one question blocked bank treasuries from moving into tokenization. If we hold a bond on blockchain instead of through a custodian, do we need more capital against it?

The answer is now official. The Federal Reserve, FDIC, and OCC issued joint guidance on March 5, 2026. A tokenized security gets the same capital treatment as the non-tokenized version of the same asset.

The technology does not change the treatment. It does not matter if the token runs on a permissioned chain or a public one. The capital rule is the same either way.

In plain terms: a tokenized U.S. Treasury is treated the same as a paper Treasury. A tokenized corporate bond carries the same capital charge as the same bond held through a custodian. The blockchain does not add a penalty. It does not trigger a higher capital buffer. The asset is the asset, no matter how ownership is recorded, a regulatory clarity explored in this institutional liquidity access guide for tokenized assets.

The guidance also confirms that tokenized securities can be used as collateral. They get the same haircuts as the non-tokenized form. The legal rights of holders must be identical to the paper version. If a token does not give holders the same rights as the underlying security, it does not qualify. The legal equivalence test is the threshold condition.

This is not a proposal. It is not a pilot. It is binding guidance from the three agencies that supervise every nationally chartered bank in the United States.

Why the New Capital Rule Unlocks Institutional Tokenization

Capital requirements are not an abstract compliance concern. They determine the economics of holding any asset. If a tokenized security needed more capital than its traditional version, every extra basis point of capital cost would eat into the economics of tokenization. Treasury desks would not adopt it. Risk committees would reject it. The business case would not close.

Banks and financial market infrastructure firms had been waiting for this answer. The guidance clears the path for institutions to modernize settlement, cut reconciliation costs, and move assets faster across financial markets. Proponents have argued for years that tokenization could do all three. The capital question was the last regulatory blocker standing in the way.

That blocker is now gone. What remains is the operational question. How do you actually tokenize a security and run it inside an institutional workflow, a process executed in this institutional asset tokenization system.

What Tokenization Actually Changes for Institutions

Tokenization is not just a new label for existing systems. It changes how financial institutions operate in four important ways.

1. Settlement gets faster

Traditional securities settle on T+2. A tokenized security can settle in minutes through atomic delivery versus payment on a blockchain. Counterparty exposure shrinks. Intraday liquidity improves. Capital that was tied up during settlement can be used elsewhere.

2. Reconciliation becomes simpler

Every on chain transfer creates an immutable record with a timestamp, an amount, and a wallet address. This record can match directly to a trade confirmation or invoice. Manual reconciliation shrinks or disappears. Finance teams no longer need to compare settlement notices with custody statements.

3. Assets become more liquid

A tokenized security can be divided into smaller units without changing the legal rights attached to it. This allows a broader investor base to participate. Assets such as private credit, real estate, and infrastructure that previously had limited secondary markets can trade on chain through approved venues.

4. Collateral moves faster

A tokenized security that qualifies as financial collateral under the capital rule can be transferred between counterparties in real time. Repo markets, margin calls, and collateral management programs become faster and more efficient when collateral can settle in minutes instead of days.

How Tokenized Securities Settlement Works

Several financial institutions have already issued tokenized bonds to test blockchain based settlement.

The European Investment Bank issued a €100 million digital bond on the Ethereum blockchain in 2021 with participation from major banks including Goldman Sachs, Santander, and Societe Generale. Investors received the same legal rights as traditional bondholders while settlement was handled through blockchain infrastructure.

UBS also issued a CHF 375 million digital bond listed on both the SIX Swiss Exchange and the SIX Digital Exchange blockchain platform, allowing the bond to settle through either traditional or blockchain infrastructure.

These deployments show that tokenized securities can operate within existing regulatory frameworks while improving settlement speed and operational efficiency.

How To Tokenize Securities Under the New Capital Framework

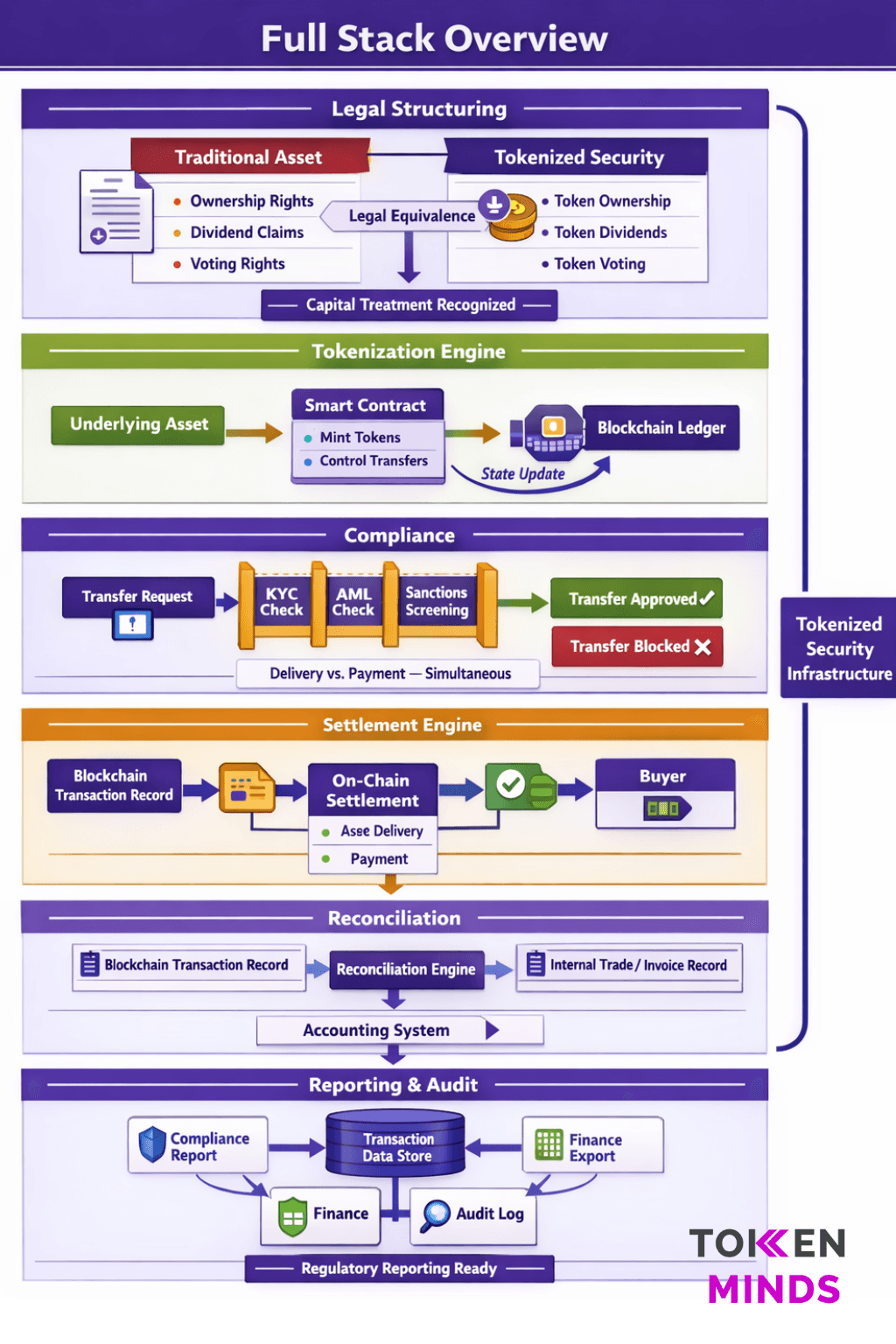

For institutions, tokenization is not just about issuing a token on a blockchain. It requires operational systems that allow the asset to move, settle and reconcile within existing compliance and risk frameworks.

Tokenizing a security is only the first step. Institutions also need operational systems to manage the asset once it exists on blockchain in a way that satisfies the risk management expectations in the new capital guidance. The guidance is clear that sound risk management and full regulatory compliance still apply. Equal capital treatment does not mean fewer controls. It means the same controls applied to a new type of infrastructure.

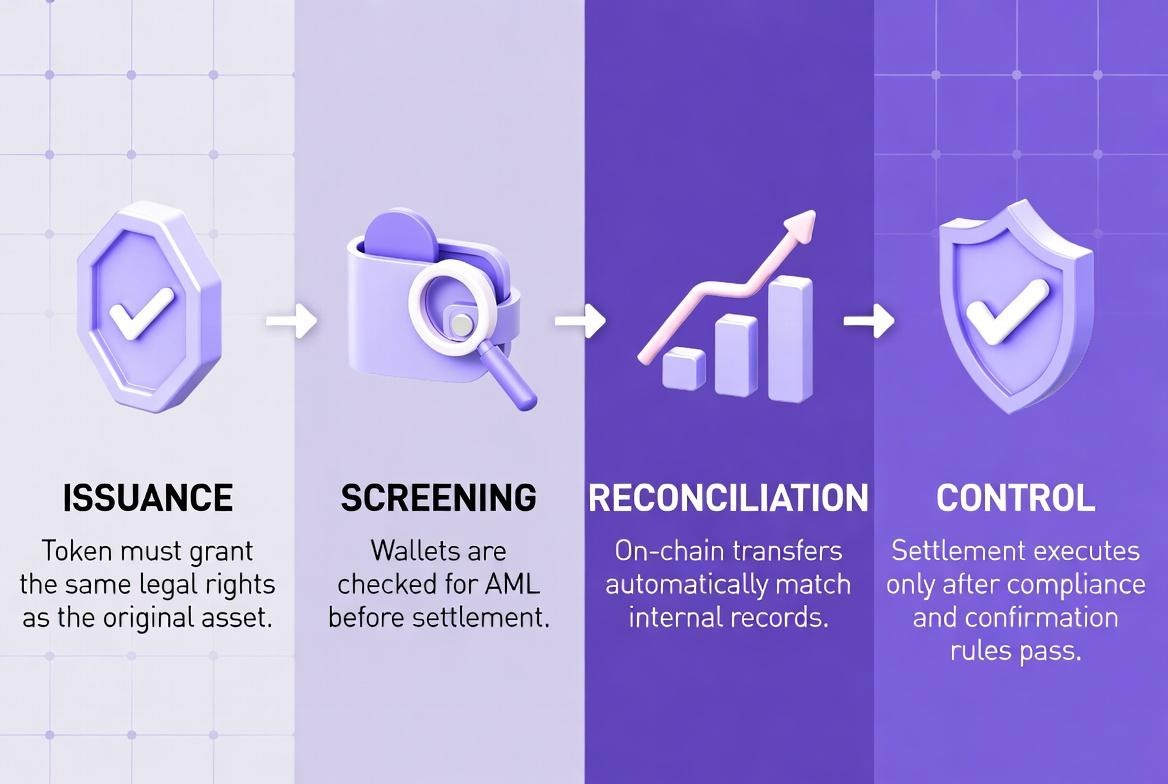

The institutions that will move fastest are the ones that already have these capabilities in place or can deploy them quickly. Institutions typically implement tokenized securities infrastructure in four steps.

1. Compliant issuance on a supported blockchain

The tokenized security must give holders the same legal rights as the paper version. This is the threshold condition for equal capital treatment under the guidance. The issuance platform must support this legal equivalence and produce documentation that confirms it. Without a written legal opinion confirming rights equivalence, the token does not qualify for the same capital treatment regardless of which blockchain it runs on.

2. Wallet compliance screening

Every wallet that sends or receives tokenized securities must be screened for AML and sanctions risk before settlement releases. Traditional AML tools screen bank accounts and SWIFT codes. They do not screen blockchain wallet addresses. The moment an institution processes an on-chain transfer without wallet screening, it is operating outside its compliance boundary. Screening must gate settlement, not run after the fact. The result must attach to the transaction record automatically with a timestamp and a named compliance owner.

3. Automated reconciliation

Every on-chain transfer must match to an internal trade or invoice record without manual work. When a stablecoin or tokenized security arrives on-chain, it has a transaction hash, a block number, an amount, and a sending address. The internal system has a trade confirmation, a purchase order reference, and an expected amount. Nothing connects them unless the reconciliation layer is built. At low volumes, manual matching works. At scale it creates a backlog that grows faster than any finance team can clear. The output must sync to internal ledgers in a format that maps to existing ERP and treasury systems without reformatting.

4. Settlement control logic

Securities must not move until confirmation rules and compliance checks pass. Atomic settlement means the transfer completes fully or does not happen at all. This removes partial settlement risk that creates accounting exceptions and operational delays. A system that releases transfers on the first block confirmation is exposed to blockchain reorganizations where early confirmations can be reversed. Confirmation rules must define how many blocks must pass before settlement is final.

Institutional Tokenization Architecture

The four systems described above are part of a larger infrastructure stack that institutions use to support tokenized securities. In practice, financial institutions build tokenization systems in layers that connect legal issuance, blockchain settlement, and internal financial systems.

The Tokenized Securities Readiness Index

Most institutions do not know how ready their setup is to act on this guidance. This index scores readiness across four areas. Each area is scored 1 to 4. Score of 1 means nothing is in place. Score of 4 means fully ready. Total out of 16.

Area | 1 - Not Started | 2 - Basic | 3 - In Progress | 4 - Fully Ready |

Compliant Issuance | No tokenization setup. Traditional custody only. | Sandbox tests done. No legal equivalence confirmed. | Live on one chain. Legal opinion in progress. | Tokens confer identical legal rights. Live on supported chains. Legal opinion complete. |

Wallet Compliance | No wallet screening. Legacy AML tools only. | Screening runs but after settlement releases. | Screening gates settlement. Results not logged automatically. | Screening gates settlement. Results logged with owner, rule, and timestamp on every transfer. |

Reconciliation | Every transfer matched by hand. No automation. | Some automation. High exception backlog. | Auto-matching for standard transfers. Exceptions still manual. | Full hash-to-invoice matching. Structured output syncs to internal ledger automatically. |

Settlement Control | Transfers release instantly on first confirmation. No rules. | Basic confirmation count. No compliance gate. | Rules in place. Compliance screening runs separately. | Atomic settlement with confirmation rules and compliance gate built in. Transfer completes fully or not at all. |

Score guide:

4 to 6: You cannot safely hold tokenized securities under this guidance yet. On-chain activity is a liability gap.

7 to 10: Partial coverage. Compliance or reconciliation gaps will surface under regulatory review.

11 to 13: Well-placed. Remaining gaps are optimization, not structural risk.

14 to 16: Fully ready. Your setup meets the operational standard the guidance requires.

Where most institutions start:

Area | Score | Why |

Compliant Issuance | 1 | No tokenization infrastructure in production. Legal equivalence not confirmed. |

Wallet Compliance | 1 | Wallet addresses sit outside existing AML screening scope entirely. |

Reconciliation | 2 | Trade confirmations tracked. On-chain transfers still matched manually. |

Settlement Control | 1 | No atomic settlement logic. Transfers release on first confirmation. |

Total | 5/16 | Not ready to operate under the new guidance without infrastructure changes. |

The gap between 5 and 16 is not a technology gap. It is an operational gap. The blockchain works. The capital rule is clear. What most institutions are missing is the layer between the two.

Operational Efficiency Comparison

Tokenized securities can improve several operational processes compared with traditional infrastructure.

Process | Traditional Infrastructure | Tokenized Infrastructure

Settlement | T+2 | Minutes

Counterparty exposure | Up to 48 hours | Near zero after settlement

Reconciliation | Multiple custodians and ledgers | Single shared ledger record

Collateral transfer | Hours or days | Near real time

These differences are why many institutions are exploring tokenized settlement infrastructure.

Estimated Operational Impact

Tokenized securities infrastructure can reduce several operational frictions that exist in traditional market systems.

Metric | Traditional Systems | Tokenized Systems |

Settlement cycle | T+2 | Minutes |

Counterparty exposure | Up to 48 hours | Near zero after settlement |

Reconciliation systems | Multiple custodians and ledgers | Single shared ledger |

Operational processing | High manual processing | Automated smart contract execution |

These operational improvements are one reason financial institutions are exploring tokenized securities infrastructure.

How Institutional Tokenization Platforms Help

Working with banks and financial institutions on tokenized securities, TokenMinds reveals the same problem every time. The blockchain works fine. The real problem is that no one has set up clear processes for how to issue, settle, and check compliance on tokenized assets.

That is where tokenization platforms come in. They handle those processes. TMX Tokenize by TokenMinds does this. It works across multiple blockchains including Ethereum, BNB Chain, Stellar, Algorand, and Midnight. Before any transfer goes through, it checks the wallet for compliance. It updates internal records automatically. Transfers only complete when all rules and checks are passed. Banks can use it without tearing out their existing systems.

TMX Tokenize also connects to the Canton Network for institutions that need access to a bigger market. The Canton Network holds over six trillion dollars in assets. It moves more than three hundred billion dollars a day. Goldman Sachs, HSBC, DTCC, and the European Investment Bank all use it. When a tokenized security goes live, it enters that market immediately.

Conclusion

The Fed, FDIC, and OCC removed the capital penalty that was holding institutions back. The rule is technology neutral. Permissioned or permissionless, it does not matter. A tokenized bond is a bond. A tokenized Treasury is a Treasury. The capital treatment is the same.

What is left is operational. Institutions need compliant issuance that confirms legal equivalence, wallet screening that gates settlement before funds move, automated reconciliation that syncs to internal ledgers, and atomic settlement logic with confirmation rules built in.

The guidance is already live. The institutions that build the operational layer now will be ready to move securities, collateral, and settlement flows onto blockchain rails ahead of the field. Those that wait will spend the next year catching up to ones that did not.

FAQ

What are tokenized securities?

Tokenized securities are traditional financial assets like bonds, stocks, or funds that are issued and recorded on a blockchain. The token represents the same legal ownership rights as the original security.

Are tokenized securities regulated?

Yes. Tokenized securities must follow the same financial regulations as traditional securities. Banks and issuers must still follow rules for compliance, reporting, and investor protection.

How do banks issue tokenized securities?

Banks issue tokenized securities using a tokenization platform that creates the asset on a blockchain. The platform manages issuance, compliance checks, settlement, and record keeping.

Do tokenized securities require additional capital?

In the United States, regulators confirmed that tokenized securities receive the same capital treatment as traditional securities. Banks do not need to hold extra capital simply because the security is tokenized.

What blockchains support tokenized securities?

Tokenized securities can be issued on several blockchain networks used by financial institutions. Examples include Ethereum, Stellar, Algorand, and other networks designed for institutional financial infrastructure.

What is TMX Tokenize?

TMX Tokenize is a tokenization platform built by TokenMinds that helps institutions issue, manage, and transfer tokenized securities. It connects blockchain settlement with compliance checks, reconciliation, and internal financial systems so institutions can operate tokenized assets within existing regulatory frameworks.