TL;DR: Stablecoin-linked cards need more than card issuing. Banks and fintechs need the right account model, custody setup, conversion flow, issuer processor, and compliance owner. The main options are pre-funded fiat ledgers, real-time stablecoin conversion, or hybrid reserve models. Each model affects authorization speed, liquidity risk, tax logs, chargebacks, and user reporting. This guide explains how product teams can evaluate stablecoin card and account infrastructure before choosing a vendor or building middleware.

What Is a Stablecoin-Linked Card?

Stablecoin card infrastructure is no longer experimental. It is a procurement decision. Banks that have already mapped their bank-grade crypto payments architecture now face the implementation question. Build the stack, buy it, or layer both. A stablecoin-linked card lets users spend from a stablecoin balance at supported card network merchants. The card network never sees crypto. What it sees is fiat, converted either at authorization or at settlement, depending on the architecture. That conversion moment is where the entire product design lives or dies. This article breaks down the deployable banking stack, implementation sequence, and production monitoring workflows needed for go-live.

How Do Stablecoin-Linked Cards Work?

The user taps or swipes. The merchant terminal sends an authorization request to the card network. The network routes it to the issuer processor. The processor checks the balance, but that balance is either fiat (pre-funded) or stablecoin (post-funded).

Here's where it gets operational:

Pre-funded model: Stablecoin converts to fiat on deposit. The card runs on a standard fiat ledger. Conversion risk sits with the wallet provider or program manager.

Post-funded model: Stablecoin sits in custody until authorization. The processor triggers a real-time conversion. FX slippage, latency, and liquidity risk shift to the conversion layer.

Hybrid model: Some programs hold stablecoin but pre-reserve fiat for authorization, then reconcile on settlement. Complex. Operationally expensive. But it reduces slippage exposure.

The Bridge-Visa announcement shows a live product model for stablecoin-linked card issuing, where developers can offer cards through one API and Bridge handles stablecoin-to-fiat conversion for merchant settlement.

What Account Model Supports a Stablecoin-Linked Card?

Card issuance is only the front end. The underlying account model determines where funds sit, when conversion occurs, and who owns the ledger.

Account Model | User Sees | Funds Sit In | Conversion Moment | Best Fit |

Stablecoin wallet account | Stablecoin balance | Custody wallet | Authorization or settlement | Crypto-native fintechs |

Fiat ledger account | Fiat balance | Program fiat ledger | Deposit | Consumer neobanks |

Dual-balance account | Fiat and stablecoin | Wallet plus fiat reserve | Depends on transaction type | Digital banks |

Treasury-backed account | App balance | Program treasury | Internal program rules | Closed-loop products |

Match the account layer to the target segment before selecting the card processor or custody provider.

What Is the Authorization Flow for a Stablecoin Card?

Walk through a $50 coffee purchase:

Step 1: Terminal authorization

Merchant POS sends a $50 authorization request to Visa or Mastercard.

Step 2: Issuer processor receives request

The issuer processor (Marqeta, Galileo, i2c, or a direct issuer) checks the available balance. In a post-funded model, it pings the stablecoin custody layer.

Step 3: Balance check and conversion trigger

If the user holds 50.10 USDC, the processor either (a) confirms pre-converted fiat balance or (b) triggers a real-time USDC to USD swap.

Step 4: Authorization response

The issuer processor returns approval to the network. Elapsed time: under 2 seconds target. Conversion latency is the biggest failure mode here.

Step 5: Settlement

24 to 72 hours later, the merchant receives fiat. The program reconciles the conversion, fees, and FX spread.

Step 6: Reporting

Transaction records hit the ledger. If the program operates in a regulated jurisdiction, the conversion event may trigger a taxable transaction for the user.

Pre-Funded vs. Post-Funded: Decision Framework

Decision Factor | Pre-Funded Wallet | Post-Funded (Real-Time Conversion) |

Conversion timing | On deposit | At authorization |

FX risk owner | User (locked rate on deposit) | Program/issuer processor |

Authorization speed | Fastest (standard fiat path) | Dependent on conversion layer latency |

Slippage exposure | Low | Medium–High |

User experience | Simple. Predictable balance. | Live stablecoin balance visible. |

Compliance event | On deposit | On authorization or settlement |

Liquidity requirement | Fiat prefunding pool | Real-time liquidity partner |

Best fit | Consumer neobank, SMB expense cards | Crypto-native wallets, remittance cards |

The right model isn't the more "crypto" one. It's the one the issuer processor can execute with acceptable failure rates.

Integration Models: Comparison Table

Model | Stack Ownership | Issuer Processor | Wallet Provider | Compliance Owner | Time to Market |

BaaS + stablecoin plugin | Program manager | Marqeta / Galileo | External custody (Fireblocks, etc.) | Shared (BaaS + program) | 4–9 months |

Direct issuer + conversion API | Issuer | In-house or licensed | In-house | Issuer | 12–24 months |

White-label stablecoin card program | Vendor-managed | Vendor (pre-integrated) | Vendor-managed | Vendor-led, shared | 6–12 weeks |

Bridge/Stripe model | Stripe/Bridge stack | Bridge-enabled Visa issuing | Bridge stablecoin rails | Bridge + program manager | Varies |

Notes: Time-to-market varies by jurisdiction, issuer setup, compliance scope, and vendor readiness.

For most product teams, the white-label route is the fastest path to production. See White-label stablecoin payments for banks for a full vendor evaluation framework.

What Roles Does the Issuer Processor Play?

The issuer processor is not just a balance checker. In a stablecoin card program, it carries operational weight across four functions:

Authorization decisioning: approves or declines in real time

Conversion trigger: calls the conversion API in post-funded models

Ledger reconciliation: maps stablecoin redemption to fiat settlement

Dispute handling: chargebacks resolve in fiat; the conversion record must be audit-ready

Most standard issuer processor integrations (Marqeta, Galileo, Synapse successors) do not support stablecoin balance checks by default. Operators add a middleware layer, a conversion API or custody bridge, that the processor calls before authorization. That middleware is where most production failures originate.

For a deeper look at how this connects to payment API architecture, see Crypto Payment Gateway vs Stablecoin API vs On/Off-Ramp.

Failure Modes: Where Stablecoin Card Programs Break

Failure Mode | Trigger | User Impact | Mitigation |

Conversion latency timeout | Swap API > 1.5s | Declined transaction | Cache pre-authorized liquidity; set authorization buffer |

Liquidity gap | Thin market for large transaction | Failed conversion, card decline | Some programs may define a reserve buffer based on daily volume and risk tolerance. |

Stablecoin depeg | USDC/USDT trades off $1.00 | Short-funded transaction, chargeback risk | Real-time depeg monitoring; automatic fiat fallback |

Compliance event miscapture | Conversion not logged as taxable event | Regulatory exposure for user and program | Append-only conversion log per transaction; user tax reporting export |

Settlement mismatch | FX rate shifts between authorization and settlement | Program absorbs spread loss | Lock conversion rate at authorization; build spread into program fee |

Custody failure | Custody provider downtime | Card fully offline | Multi-custodian architecture; offline pre-funded fallback |

Most programs treat these as edge cases. Operators who've run card programs at scale treat them as design constraints. Build for failure first.

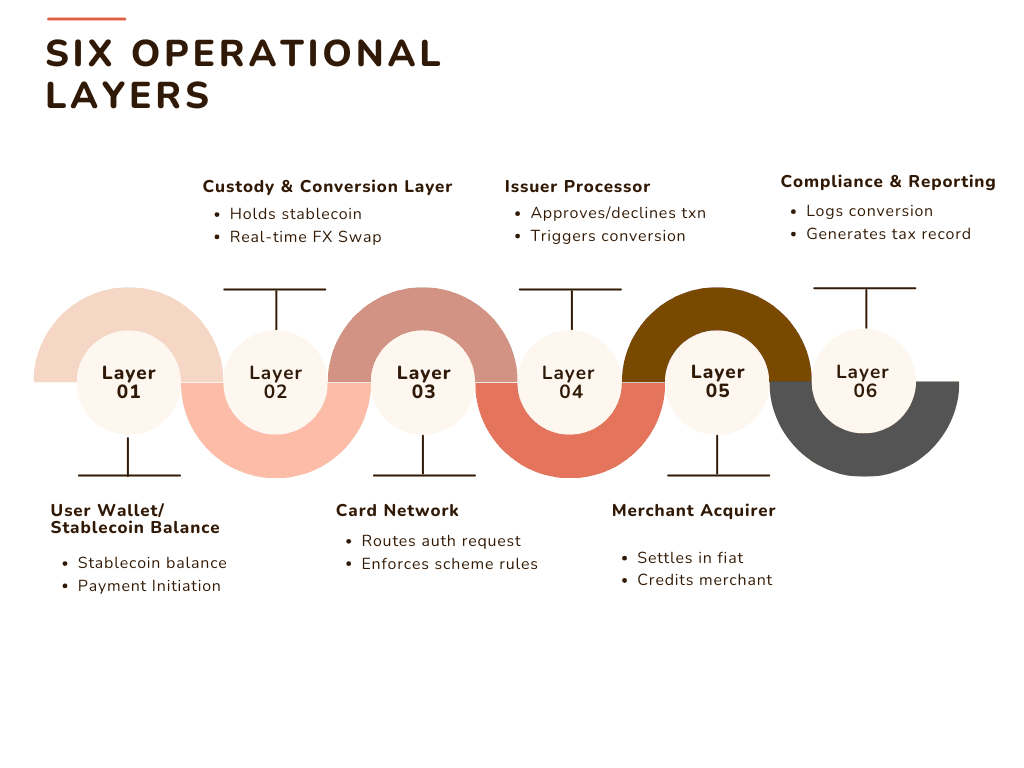

Cross-Layer Dependency Map

Every card transaction crosses six operational layers. A failure in any one breaks the chain.

Compliance ownership doesn't live in one box. It spans the custody layer (conversion event), the issuer processor (authorization record), and the reporting layer (user-facing tax data). Whoever owns program management owns the thread connecting all three.

For a full architecture breakdown, see Bank-Grade Crypto Payments Architecture: A CTO's Blueprint.

Risk and Compliance Ownership Matrix

Function | Wallet Provider | Issuer Processor | Program Manager | Card Network |

KYC/AML on user | ✅ Primary | Shared | Shared | ✗ |

Stablecoin custody | ✅ Primary | ✗ | ✗ | ✗ |

Conversion execution | ✅ Primary | Triggered | Configured | ✗ |

Authorization decision | ✗ | ✅ Primary | Rules config | Pass-through |

Fiat settlement | ✗ | ✅ Primary | ✗ | Facilitated |

Chargeback resolution | ✗ | ✅ Primary | Oversight | ✅ Primary |

Tax event logging | Shared | Shared | ✅ Primary | ✗ |

Card scheme compliance | ✗ | ✅ Primary | ✅ Primary | ✅ Enforced |

Compliance gaps almost always appear at the seams between these parties. Define ownership in contracts before defining it in code.

What to Build Next

If a product lead is evaluating stablecoin card architecture, the immediate decisions are:

Pre-funded or post-funded? Decide based on the target user base's risk tolerance and the processor's conversion capability.

Who owns the custody layer? Avoid letting this default to the BaaS provider without a clear SLA.

How are conversion events logged? Build this before launch, not after the first tax season.

What is the depeg response plan? It should be automated, not a Slack thread.

The Bridge-Visa demonstrates a market model for API-based stablecoin card issuing. The question for product teams is whether the stack (processor, custody, compliance layer) can execute it reliably.

Ready to validate your stablecoin card architecture before you build?

Request a stablecoin card product feasibility sprint.

Our team maps your stack against live issuer processor constraints, conversion API options, and card scheme requirements before you commit to an integration model.

Frequently Asked Questions:

Q: Can a stablecoin card work without a bank license?

A: Often, but usually through a licensed issuer, BaaS provider, or program sponsor. A licensed BaaS provider or issuing bank sponsors the program. The program manager operates under that license. The program manager owns the product and the user relationship, not the charter. Licensing requirements vary by geography; EMEA and APAC have different e-money frameworks than the US.

Q: What stablecoins are supported on live card programs?

USDC is commonly supported in institutional card and custody workflows. It has regulated issuance (Circle), broad liquidity, and existing integrations with Visa and custody providers. USDT support depends on issuer policy, jurisdiction, and risk review. Yield-bearing stablecoins remain an edge case for card programs.

Q: How does authorization work when USDC depegs?

Most programs set a circuit breaker. If USDC trades below a threshold (e.g., $0.995), the conversion layer pauses and the card falls back to a pre-funded fiat reserve or declines transactions. Operators define that threshold in program parameters. This is an operational decision, not just a risk one, it directly affects user experience during market stress events.

Q: Who handles chargebacks on a stablecoin card transaction?

The issuer processor handles chargeback resolution with the card network. The dispute resolves in fiat. The program requires a clear audit trail of the conversion event; timestamp, rate, stablecoin amount, and fiat equivalent to defend against disputes. If that record doesn't exist, the program absorbs the loss.

References:

Stripe: Bridge Partners with Visa to Enable Stablecoin-Linked Cards (April 30, 2025). Source for post-funded stablecoin card architecture, Visa settlement integration, and developer API model. https://stripe.com/newsroom/news/bridge-partners-with-visa