TL:DR: Banks have three stablecoin payment paths. They can partner with a payment network. They can embed an orchestration API. They can launch a branded stablecoin. Each path changes speed, control, licensing, reserve economics, and operating risk. Network partnerships suit corridors and treasury settlement. Orchestration APIs suit bank-owned UX with faster launch. Branded stablecoins suit deeper product control and issuer economics. Build, white-label, or hybrid execution comes after this choice. Banks should assess custody, compliance delegation, portability, and reserve transparency before procurement.

Should Banks Partner, Embed, or Launch Their Own Stablecoin?

Before evaluating build vs. white-label, banks must first choose a strategic path. Each model serves different product goals and risk tolerances.

Strategic Path | Best Fit | Bank Gains | Main Tradeoff |

Partner with a network | Cross-border settlement, FI-to-FI payments, treasury corridors | Faster access to payment rails and liquidity | Less product control and fewer issuer economics |

Embed an orchestration API | Stablecoin payments, cards, accounts, merchant settlement | Faster launch with bank-owned UX | Vendor dependency and integration risk |

Launch a branded stablecoin | Bank wants its own stablecoin product and reserve strategy | More brand control and product economics | Higher licensing, reserve, liquidity, and operating risk |

This strategic choice determines which implementation model (build, white-label, or hybrid) makes sense downstream.

Path 1: Partner With a Stablecoin Payment Network

Network models like Circle CPN provide configurable payment rails where financial institutions meet eligibility requirements and configure risk controls. Circle frames CPN participants as responsible for their own services, licenses, and compliance, with Circle acting as a technology service provider. This model offers faster access to liquidity and settlement infrastructure, with reduced product control.

Path 2: Embed a Stablecoin Orchestration API

API-layer providers like BVNK, Fireblocks, or Bridge enable banks to embed stablecoin functionality while retaining UX ownership. BVNK, for example, offers both managed payments (using their custody, liquidity, and licensing) and self-managed models (where banks plug in their own licenses, custodian, and liquidity partners). This path balances speed-to-market with moderate integration complexity.

Path 3: Launch a Branded Stablecoin Product

For banks seeking full product ownership, platforms like Stripe's Open Issuance via Bridge enable institutions to launch and manage their own stablecoin, customize blockchain support, and define reserve mix. Stripe notes that banks are one target group for this branded stablecoin strategy. This path offers maximum brand control and product economics, but requires significant licensing, reserve management, and operational investment.

How Strategic Fit Shapes Build, White-Label, or Hybrid Execution

Stablecoin payment infrastructure is no longer experimental. It is a procurement decision. Banks that have already mapped their bank-grade crypto payments architecture and reviewed their compliance integration checklist now face the harder question. Build the infrastructure, buy it, or layer both. This article gives product and strategy leads a structured framework for that decision. It covers vendor taxonomy, compliance delegation boundaries, and a pilot-to-scale pathway with clear exit provisions.

The build path means the bank's team owns the full stack. Wallet infrastructure, stablecoin ledger logic, treasury operations, settlement rails, and compliance tooling. That is a significant engineering commitment. Implementation estimates suggest 18 to 36 months and three to five specialized hires for in-house builds, based on TokenMinds planning benchmarks.

The white-label path means licensing a pre-built platform from a vendor like BVNK, Bridge, or a Circle CPN participant. The institution gets faster time-to-market, typically following a 90 to 180-day planning range, depending on scope and vendor readiness. The bank also inherits the vendor's architecture assumptions and their compliance posture.

Neither path is universally correct. The decision turns on four variables. Existing infrastructure, internal compliance maturity, target use case, and acceptable vendor dependency.

Build vs. White-Label vs. Hybrid: Core Tradeoff Matrix

Dimension | Build In-House | White-Label | Hybrid |

Time to market | 18-36 months | 90-180 days | 6-12 months |

Control over architecture | Full | Limited | Partial |

Compliance ownership | Full | Shared (complex) | Modular |

Upfront cost | High (capex-heavy) | Low (opex model) | Medium |

Vendor dependency | None | High | Moderate |

Customization ceiling | Unlimited | Platform-constrained | Component-level |

Exit complexity | Low | High | Medium |

Regulatory clarity | The bank's burden | Shared, but still the bank's | Depends on layer |

Hybrid models are gaining traction. They use white-label rails for settlement and custody, while keeping the customer-facing product and compliance logic in-house. Banks pursuing stablecoin-linked card and account products often find hybrid the most defensible path.

For a detailed technical blueprint of the infrastructure required, see Crypto Payment Integration for Banks: Vendor Landscape & Decision Framework.

What Compliance Does the Bank Still Own with White-Label?

This is where the risk boundary becomes important. White-label vendors may process transactions. They do not hold the bank's license. That distinction matters.

The bank keeps customer KYC and AML obligations. SAR filing stays with the institution. OFAC screening escalation remains with the bank. Chargeback and dispute resolution policy, end-customer liability, all on the bank's side of the ledger. The vendor may handle wallet mechanics, stablecoin conversion, settlement finality, and in some cases, custody. However, the bank retains regulated accountability for the end product.

Stripe's Open Issuance via Bridge illustrates the branded stablecoin path. Their model lets banks and fintechs issue stablecoin-backed instruments. But the issuing institution retains regulatory accountability for the product. Circle's CPN documentation follows the same structure. The network provides rails and liquidity, not a compliance shield.

The compliance delegation boundary map below clarifies what can be shared and what cannot.

Compliance Delegation Boundary Map

Function | Delegable to Vendor | Retained by Bank |

Wallet provisioning | Yes | No |

KYC identity verification | Partially (data sharing) | Final decision |

AML transaction monitoring | Partially (vendor flags) | Review and SAR filing |

OFAC screening | Partially (real-time check) | Escalation and blocking |

Stablecoin custody | Yes (if licensed custodian) | Oversight and audit |

Dispute resolution | No | Yes |

Regulatory reporting | No | Yes |

Consumer liability | No | Yes |

Banks that assume the vendor absorbs compliance risk usually discover the gap during their first regulatory examination. Plan for this before signing.

Vendor Taxonomy: Full-Stack vs. Modular Providers

Not all vendors offer the same surface area. Before issuing an RFP, categorize the vendor type.

Full-stack vendors provide end-to-end infrastructure. Custody, settlement, stablecoin conversion, card issuance connectivity, and compliance tooling. These include platforms like BVNK and Bridge (now integrated into Stripe's ecosystem). They move fastest but create the deepest lock-in.

Modular vendors provide a specific layer. For example custody only, or payment rails only. Circle CPN represents a network partner model, where participants configure risk controls and maintain compliance responsibility. Banks assemble the stack themselves. More control, more integration work.

Embedded finance vendors offer white-label stablecoin features as part of a broader banking-as-a-service platform. Suitability for institutional treasury products depends on controls, data export capabilities, custody depth, and SLA rigor.

The right vendor type maps to the bank's product goal. A remittance corridor pilot needs different infrastructure than an enterprise treasury settlement product.

For a detailed comparison of stablecoin payment rails and providers, see Stablecoin Payment Rails Compared: Circle, Fireblocks, Ripple, BVNK, Bridge | TokenMinds.

How Should a Bank Evaluate Stablecoin Vendors at the BOFU Stage?

By the time a bank reaches vendor evaluation, the product thesis is usually fixed. The evaluation is about fit, risk, and exit.

Vendor Evaluation Checklist

Architecture and custody:

Start with the basics. Does the vendor segregate customer funds by default? What stablecoins does the vendor support? USDC, PYUSD, EURC or something proprietary? Is the settlement layer on a public chain, permissioned chain, or both? And what's the SLA for settlement finality?

Reserve model and economics:

What reserve assets support the stablecoin? Who earns reserve yield or related economics? How are reserve disclosures audited? What happens during redemption pressure or depeg events?

Compliance alignment:

This is where many evaluations fall short. What money transmission licenses does the vendor have in the bank's target jurisdictions? Can they provide audited proof of reserve documentation? What is their OFAC screening methodology and escalation process? How are SAR-trigger events communicated to the issuing institution?

Integration and portability:

Are APIs RESTful and well-documented, or proprietary? Can transaction data be exported in a format compatible with the bank's core banking system? What are the data residency terms?

Exit provisions (critical):

What is the notice period for contract termination? Who owns the customer relationship data post-termination? Is there a wallet portability clause? What happens to in-flight transactions on termination?

Weak exit provisions are the most common long-term risk in white-label agreements. Negotiate them before signing, not after.

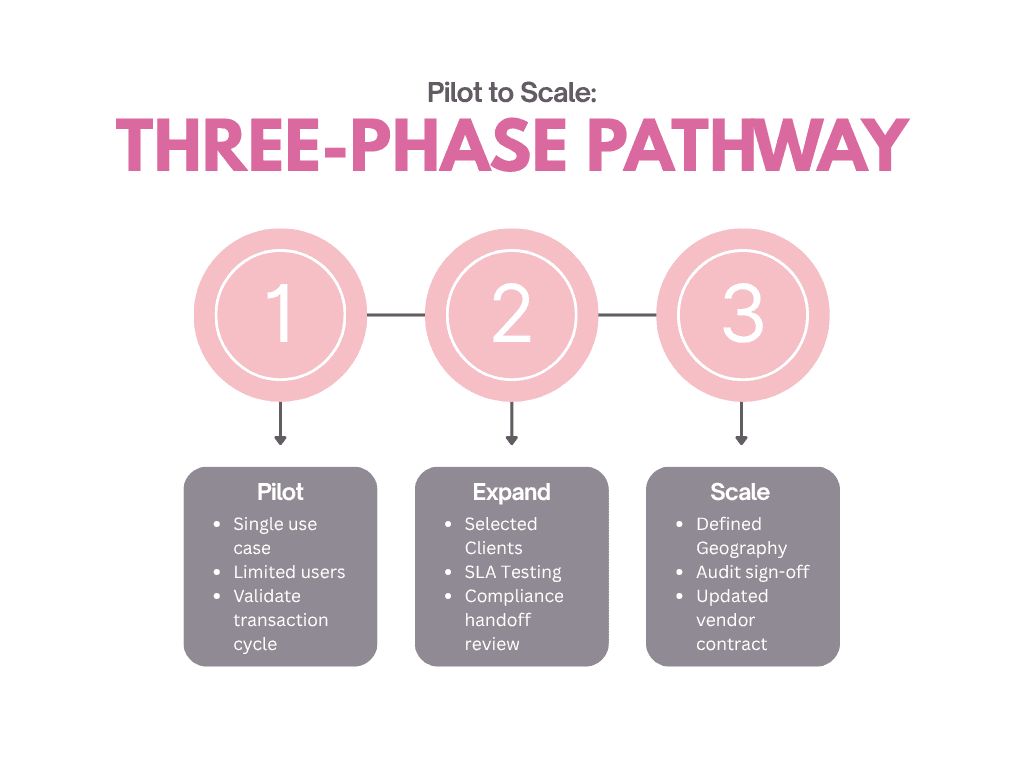

What Does a Stablecoin Payment Pilot Look Like Before Scale?

Pilot design matters more than most banks admit. Skip structured pilots and the institution will discover integration failures or compliance gaps under live transaction volume. Here's a practical pathway that works.

Pilot to Scale: Operational Decision Tree

Phase 1: Pilot (Months 1 to 3)

Keep it narrow. Single corridor or single use case. Internal or limited external users only. The goal is to validate settlement speed, stablecoin conversion rate accuracy, and compliance workflow triggers. The decision gate is simple: Can the bank complete a full transaction cycle, including exception handling, in under 24 hours?

Phase 2: Controlled Expansion (Months 4 to 9)

Now expand to selected enterprise clients or a defined product line. Stress-test the compliance delegation model under real transaction volume. Validate vendor SLA performance. The decision gates multiply here. Is the vendor meeting SLAs? Are compliance handoffs clean? And critically, is the bank's internal team able to manage exception volume?

Phase 3: Scale (Month 10+)

Full product rollout with defined geography and customer segment. But before the institution gets here, three things are needed: audit of pilot data, legal sign-off on compliance ownership documentation, and a renegotiated vendor contract with updated volume tiers.

One thing banks consistently underestimate? The compliance staffing required during Phase 2. Vendors flag. Humans decide. Make sure the bank's internal team is resourced before expanding.

Risk and Ownership Matrix

Risk Category | Primary Owner | Vendor Role | Escalation Path |

Settlement failure | Vendor SLA | Execute remediation | Bank ops team |

Stablecoin depeg event | Bank treasury | Notify | Bank risk committee |

Wallet compromise | Vendor security | Incident response | Bank CISO + regulator |

AML false positive | Bank compliance | Flag transaction | Bank compliance officer |

Regulatory change | Bank | Monitor and advise | Bank legal + vendor |

Core banking integration failure | Bank IT | Support | Vendor TAM + internal IT |

Failure Modes to Anticipate

Failure Mode | Root Cause | Mitigation |

Compliance handoff gap | Unclear contract terms on AML delegation | Define delegation boundary in SLA before signing |

Vendor lock-in at scale | No exit clause, proprietary APIs | Negotiate portability and data export rights upfront |

Settlement SLA miss at volume | Vendor infrastructure not tested under load | Require load testing data during procurement |

Stablecoin reserve opacity | Vendor uses algorithmic or opaque reserve | Require audited proof of reserve as contract condition |

Pilot success, scale failure | Compliance staffing gap | Build internal headcount plan into Phase 2 budget |

Cross-Layer Dependency Map

Layer | Component | Owned By | Depends On |

Customer interface | App / portal | Bank | Core banking API |

Identity | KYC/AML engine | Bank (with vendor data feed) | Vendor transaction data |

Stablecoin rails | Issuance, conversion, transfer | Vendor | Chain availability, liquidity |

Settlement | Finality confirmation | Vendor + Bank treasury | Chain SLA, nostro accounts |

Compliance | OFAC, SAR, reporting | Bank | Vendor transaction flags |

Custody | Wallet + key management | Vendor (if custodian) | Proof of reserve audit |

Card issuance | Virtual/physical card linkage | Vendor or bank | Card network agreements |

Ready to evaluate which stablecoin partner model fits your institution? Request a stablecoin partner-model strategy workshop with the TokenMinds team. https://tokenminds.co/become-our-client/

Frequently Asked Questions:

Q: Can a bank use a white-label stablecoin platform without holding a crypto license?

The answer depends on jurisdiction. In many markets, the vendor's license covers the underlying rails, but the issuing bank still needs relevant payment or e-money authorizations. Get a legal opinion specific to the bank's target markets before assuming the vendor's license covers the institution's product.

Q: How long does a typical stablecoin payment integration take with a white-label vendor?

Most production integrations take 90 to 180 days from contract to first live transaction. Banks with legacy core banking systems on the slower end, or without a dedicated integration team, should plan for the upper bound.

Q: What exit rights should a bank negotiate in a white-label stablecoin agreement?

At minimum: wallet data portability, a 90-day minimum notice period, in-flight transaction completion guarantees, and a clean customer data export clause. Anything shorter than this creates meaningful operational risk at termination.

Q: How does the build vs. white-label decision change for a bank launching stablecoin-linked cards?

Card products add network agreement complexity. Most banks launching stablecoin-linked cards start with a white-label vendor that already holds Visa or Mastercard principal membership or a co-brand agreement. Building that relationship from scratch adds 12 to 18 months. See Stablecoin Card Issuing API for Banks | TokenMinds on stablecoin-linked card architecture for the full breakdown.

Q: Should a bank partner with a network or launch its own stablecoin?

A bank should partner with a network when speed, liquidity, and settlement access matter most. A bank should launch its own stablecoin when product control, brand ownership, and reserve economics justify higher operating risk.

References:

Stripe. "Introducing Open Issuance from Bridge." Stripe Blog. https://stripe.com/blog/introducing-open-issuance-from-bridge

Circle. "Circle Payments Network (CPN): Product and Technical Documentation." Circle Developer Docs. https://developers.circle.com/circle-mint/docs/circle-payments-network

BVNK. "Stablecoin Payments Infrastructure for Financial Institutions." https://www.bvnk.com

Stripe. "Open Issuance: Launch and Manage Your Own Stablecoin." Stripe Documentation. https://stripe.com/docs/open-issuance