TL;DR

Asset tokenization is the process of converting ownership of real-world assets into digital tokens recorded on a blockchain. The process spans governance, regulatory compliance, and technical infrastructure. It involves understanding the types of tokenization models, the legal frameworks across various jurisdictions, and the components that make up the tokenization infrastructure (e.g., blockchain, smart contracts). Each of these elements plays a crucial role in making asset tokenization efficient, transparent, and compliant.

What Is Tokenization?

Tokenization Definition

Tokenization is the process of converting rights into digital tokens. These tokens represent ownership, claims, or access permissions. Distributed ledgers record these tokens across network participants. The system enables direct transfer between approved parties. The process restructures how ownership is issued and settled. It does not create new economic value.

Tokenization in blockchain

The digital token is created and stored on a blockchain network. The blockchain acts as a shared online record ledger. The ledger shows who owns each tokenized asset. Participants can view ownership through the network. This blockchain system removes the need for paper certificates.

Tokenization vs Digitization vs Encryption vs Securitization

The concept of tokenization may sound similar to other financial terms. Many readers confuse it with digitization, encryption, or securitization. Each term serves a different purpose. The table below explains the key differences.

Term | What It Does | Main Purpose |

Tokenization | Creates digital tokens that represent ownership rights | Records and transfers ownership digitally |

Digitization | Converts physical information into digital format | Stores data in digital systems |

Encryption | Scrambles data into unreadable coded text | Protects information from unauthorized access |

Securitization | Packages assets into financial securities | Creates tradable investment products |

Asset Tokenization Terms

Digital Asset

Digital assets are tokens recorded in a blockchain system. These assets represent ownership, value, or access rights. These assets exist only in digital form.

Asset Tokenization

Asset tokenization is the conversion of asset ownership into digital tokens. These tokens represent financial or physical assets on a blockchain network. These tokens enable the digital transfer of ownership rights.

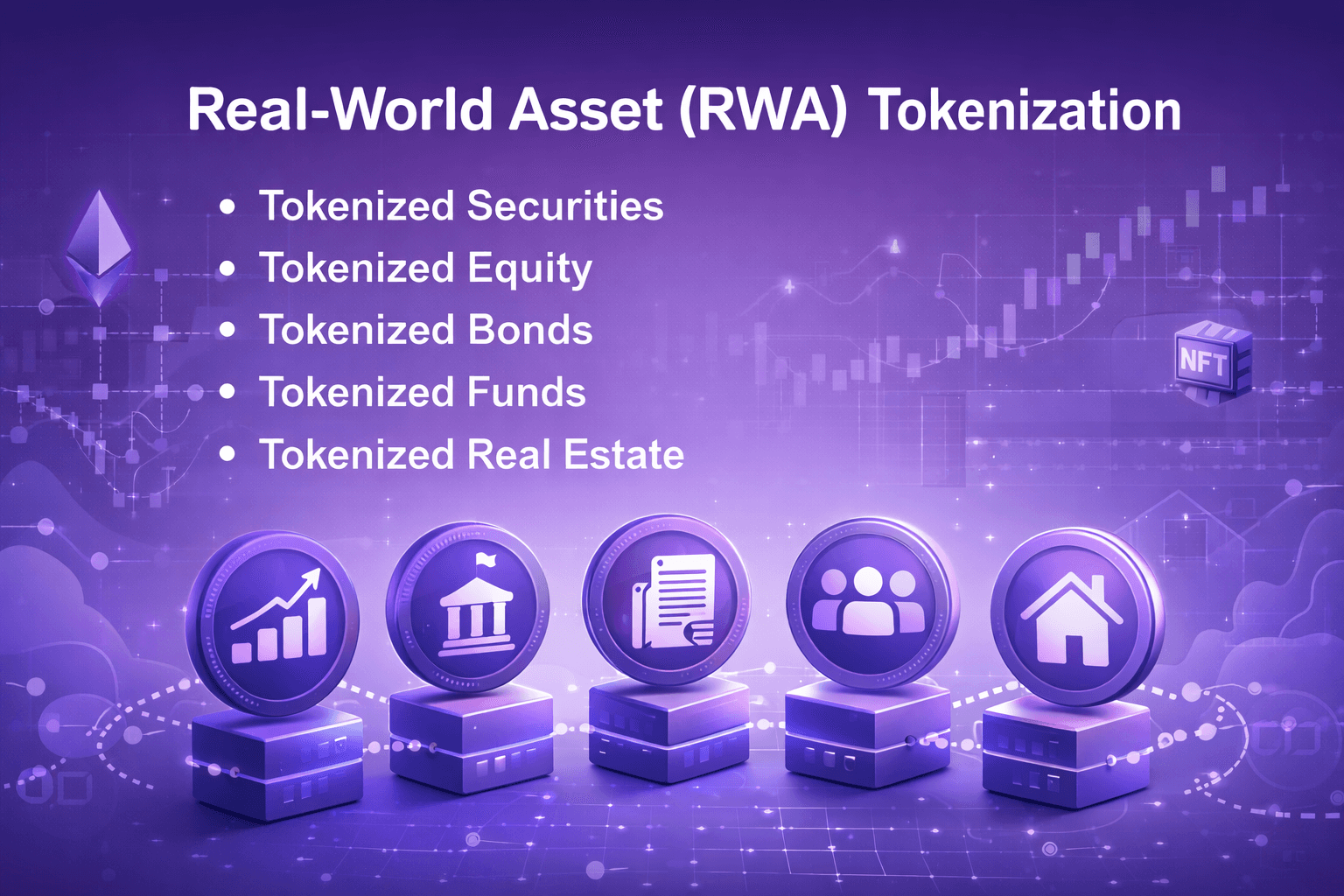

Real-World Asset (RWA)

Real-world asset is a physical or traditional financial asset. It includes real estate, bonds, equity, or commodities. It becomes tradable on blockchain after tokenization.

Tokenized Securities

Tokenized securities are financial instruments regulated and issued as digital tokens. These instruments represent equity, debt, or investment contracts.

Tokenized Equity

Tokenized equity is company ownership represented as a digital token. This grants holders rights similar to traditional shares. Ownership is recorded on a blockchain system.

Tokenized Bonds

Tokenized bonds are debt instruments issued as digital tokens. These tokens represent the borrower's repayment obligations. The coupon and settlement processes are automated through smart contracts.

Tokenized Funds

Tokenized funds are shares of investment funds issued as tokens. These tokens represent participation in a pooled investment portfolio. Ownership is recorded digitally on a blockchain network.

Tokenized Real Estate

Property tokenization is the representation of property ownership as a token. These tokens divide the property's value into smaller digital units. This allows for partial ownership through a blockchain system.

The Structural Gap in Tokenization

Tokenization is often described as a shift from off-chain to on-chain systems. In reality, this description is incomplete. Research from CFA Institute shows that tokenization includes multiple structural models. Assets do not automatically become fully on-chain instruments when tokenized. Instead, some structural elements may remain outside the distributed ledgers. These arrangements form hybrid structures.

In practice, different parts of an asset can reside on different layers. Three structural components shape this arrangement:

Asset representation

Ownership enforcement

Transfer and settlement mechanisms

For example, a token can be transferred on the blockchain. However, legal ownership may remain recorded in an off-chain registry. This separation creates structural complexity. To address this issue, tokenization is better understood as a spectrum.

Assets generally fall into three broad categories. Conventional structures, hybrid models, and fully on-chain native assets. Understanding this framework is necessary before evaluating efficiency, liquidity, or compliance impacts. The following sections explain this spectrum in detail.

The Asset Spectrum of Tokenization

The asset spectrum describes different levels of digitalization in tokenization. It rejects the idea that assets are either tokenized or not. Instead, tokenization exists across a spectrum. Along this spectrum, assets differ in how they are structured. Some assets remain fully conventional.

Some adopt hybrid arrangements. Others exist entirely within distributed ledgers (on-chain).

The spectrum shows that tokenization is not defined by asset type. Instead, it is defined by structure. Two identical assets can occupy different positions on the spectrum. The distinction depends on how ownership is recorded and transferred. This structural design affects settlement processes, compliance controls, and custody models. Understanding this relationship makes tokenization frameworks easier to evaluate.

The Three Structural Components of the Spectrum

The asset spectrum is defined by three structural components. These components determine how ownership is recorded, enforced, and transferred.

Representation of the Asset

Representation defines where the asset exists. It describes how ownership or economic rights are recorded. The asset may exist in a paper record, electronic registry, or on a distributed ledger.

Ownership Enforcement Form

Enforcement defines how ownership is legally validated. It may rely on traditional legal systems, blockchain consensus, or a combination of both. Hybrid enforcement structures often create legal uncertainty.

Operations and Mode of Transfer

Operations define how the asset moves between parties. Transfer may occur through traditional clearing systems or distributed ledgers. Some blockchain systems enable atomic settlement. Transfer structure influences capital efficiency.

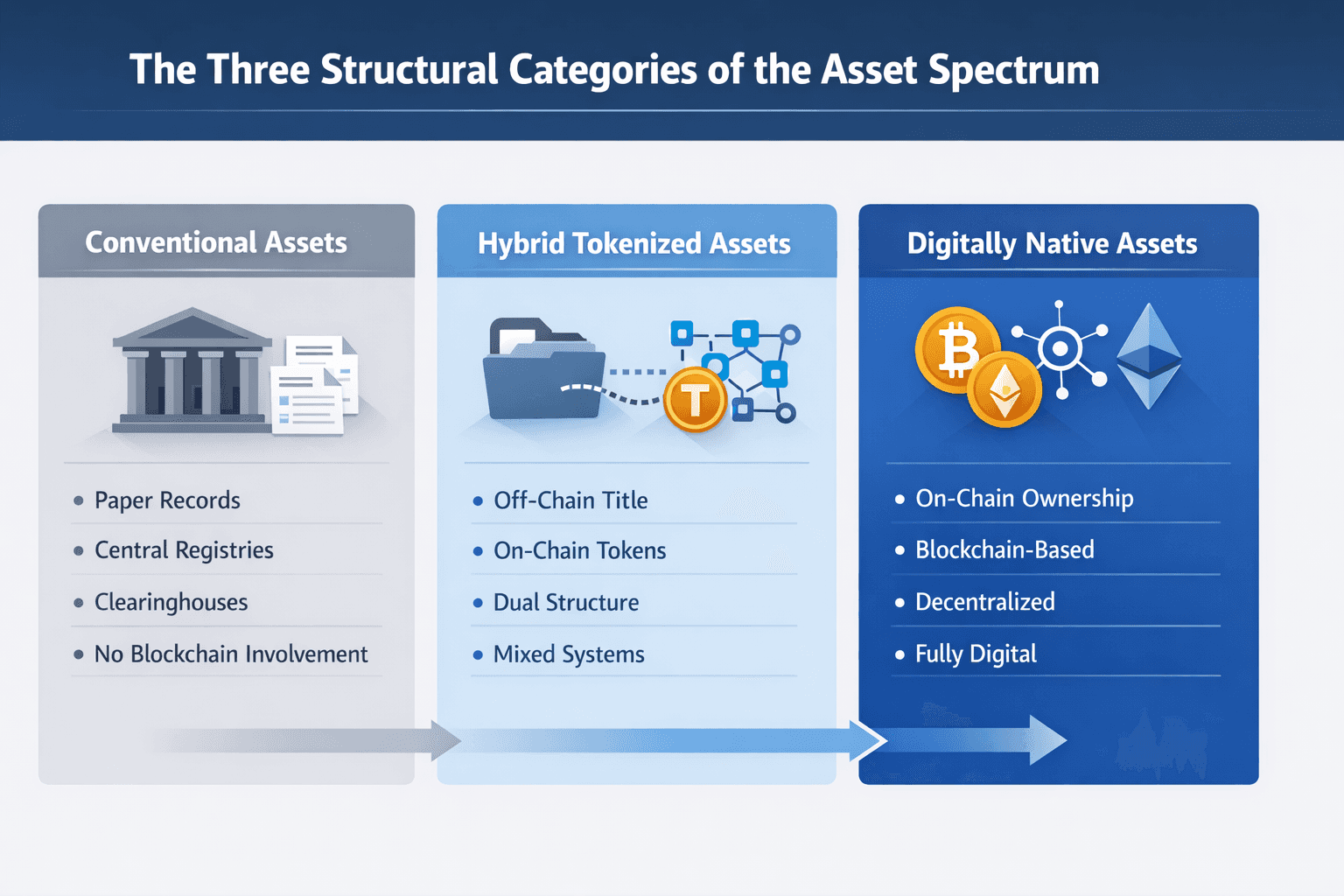

The Three Structural Categories of the Asset Spectrum

The asset spectrum can be grouped into three structural categories. These categories describe how ownership and transfer are arranged. They do not classify assets by industry. Instead, they classify assets by structural design.

1. Conventional Assets

Conventional assets operate fully outside distributed ledgers. Ownership is recorded in paper documents or centralized databases. Transfer depends on intermediaries such as custodians and clearing systems. Settlement follows established clearing cycles.

In these cases, no part of the asset exists on a blockchain.

2. Hybrid Tokenized Assets

Hybrid assets combine traditional ownership with blockchain elements. Legal titles often remain in an off-chain registry. At the same time, a blockchain token may represent economic rights. This creates a dual-layer structure. Because of this structure, transfer may occur on-chain. However, legal enforcement may still depend on traditional systems.

3. Digitally Native Assets

Digitally native assets exist entirely on distributed ledgers. The token itself represents ownership. No separate off-chain registry records title. Transfer and settlement occur through blockchain consensus.

In this model, representation, transfer, and enforcement align on the same layer.

These three categories show that tokenization is not uniform. An asset’s position depends on where ownership is recorded and enforced. This structural difference shapes settlement design, compliance approach, and operational processes.

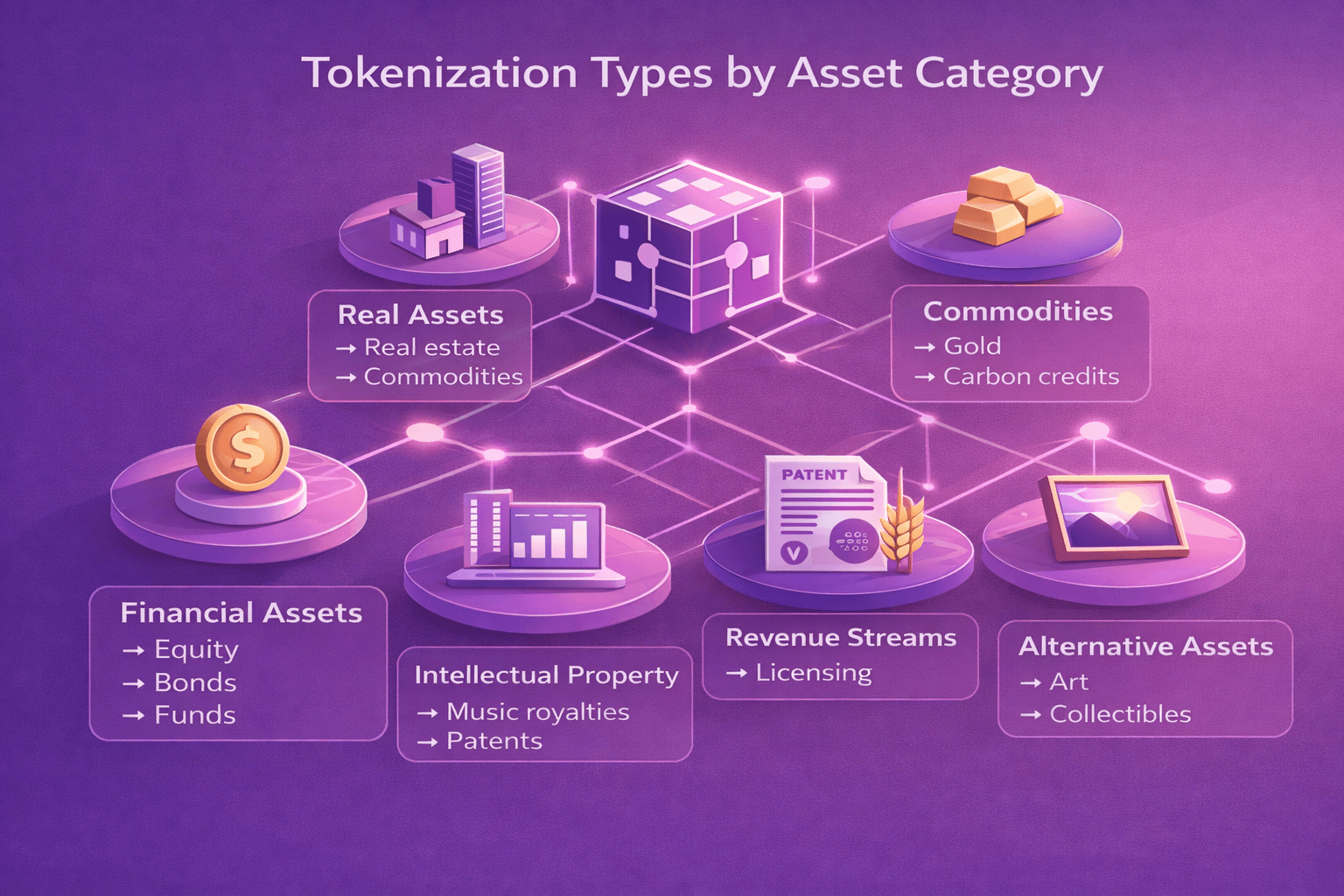

What Assets Can Be Tokenized?

The asset spectrum explains how ownership structures differ. The next question concerns which assets can move within this spectrum. Tokenization of assets applies to assets with clearly defined ownership rights. Ownership must be recordable and transferable. Many traditional assets meet this condition.

Financial Assets

These assets already have defined ownership and registry systems. Examples include:

Public equities

Corporate bonds

Government bonds

Money market funds

Private equity

Private credit

Structured products

Real Assets

These assets rely on physica ownership records. Examples include:

Residential real estate

Commercial real estate

Infrastructure assets

Energy assets

Precious metals

Agricultural commodities

Commodities

These assets are often standardized and measurable. Examples include:

Gold

Oil

Agricultural products

Carbon credits

Alternative Assets

These assets depend on valuation frameworks.

Examples include:

Art

Collectibles

Fine wine

Rare watches

Most of these assets begin as conventional structures. When a blockchain token represents ownership or economic rights, they move into hybrid form. Digitally native assets differ because they originate directly on distributed ledgers.

How Assets Move Across the Spectrum

An asset’s position on the spectrum depends on three decisions. Each decision determines whether the asset stays conventional, hybrid, or digitally native.

Define Ownership Location

First, decide where ownership exists. If ownership exists only in traditional registries, the asset remains conventional. If a token represents the asset but the legal title stays off-chain, the asset becomes hybrid. If ownership exists entirely on a blockchain, the asset becomes digitally native. Ownership location is the starting point of spectrum movement.

Define Ownership Enforcement

Next, decide how ownership is protected. If courts and legal systems enforce ownership, the structure remains conventional. If blockchain validation rules enforce ownership, the structure becomes digitally native. If both systems are required, the structure is hybrid. Enforcement defines legal certainty.

Define the Settlement Model

Finally, decide how ownership transfers between parties. If transfer relies on intermediaries and clearing cycles, the structure remains conventional. If tokens transfer on-chain but legal updates occur off-chain, the structure is hybrid. If transfer and settlement occur entirely on-chain, the structure becomes digitally native. Settlement design determines operational complexity.

What This Means

An asset does not move across the spectrum all at once. It shifts layer by layer. Most tokenization of assets today modifies one or two layers. That is why hybrid models dominate.

Why the Asset Spectrum Matters for Institutions

The asset spectrum explains structural differences in ownership design. These structural differences affect how the tokenization of assets is implemented. They influence legal recognition, settlement design, custody structure, and operational control. An asset’s position on the spectrum determines how these elements interact.

1. Compliance and Legal Recognition

Legal recognition depends on where ownership is enforced.

Conventional assets rely entirely on established legal systems.

Hybrid assets split enforcement between blockchain records and legal registries.

Digitally native assets rely on network consensus for validation.

Because enforcement mechanisms differ, compliance design must also differ. Misalignment between token transfer and legal title can create structural risk.

2. Settlement and Capital Efficiency

Settlement processes also change across the spectrum.

Conventional assets settle through intermediaries and clearing cycles.

Hybrid assets may reduce processing time through on-chain transfers.

Digitally native assets enable direct blockchain settlement.

As settlement models change, liquidity and capital usage may also change.

3. Custody and Control

Custody requirements follow the same structural logic.

Conventional assets rely on custodians and centralized registries.

Hybrid assets require coordination between off-chain custody and on-chain key management.

Digitally native assets depend entirely on secure key control.

Each position demands a different custody framework.

4. Operational Complexity

Operational design varies across categories. Hybrid structures introduce dual systems. Institutions must manage blockchain infrastructure alongside traditional records. Research from Baltais and Sondore note that automation depends on reliable data inputs. Infrastructure readiness therefore becomes a critical factor.

Current State of the Spectrum in 2026

The asset spectrum continues to evolve. However, adoption remains concentrated in hybrid structures. Most tokenized assets still combine off-chain legal ownership with on-chain representation.

Stablecoins Lead the Market

Stablecoins represent the largest share of tokenized markets. The total stablecoin market has grown toward nearly $300 billion in value in 2025. They are backed by off-chain reserves. At the same time, their tokens circulate on distributed ledgers. This structure reflects the hybrid position of the spectrum.

Tokenized Treasuries Are Expanding

Tokenized government bonds and treasury products are increasing. Since early 2024, tokenized U.S. treasuries have risen to nearly $11 billion. This increase highlights growing interest in asset tokenization for safe-asset classes. These products keep traditional legal frameworks. However, they allow transfer and settlement on-chain. This model shows gradual movement across the spectrum.

Institutional Risk Scenario: Hybrid Tokenized Bond

Hybrid Tokenized Bond is an Institutional Risk Scenario.

A corporate bond is a tokenized corporate bond issued by a financial institution on a hybrid basis. This relationship is registered at a conventional registry. A token is control over a distributed registry. The token is transferred on-chain to another buyer by an investor. Nevertheless, the legal registry is not updated. Records on-chain indicate the new owner. The former owner is still registered in the legal registry. In case of a dispute, courts will depend on the legal registry. The blockchain transfer is not likely to establish legal ownership.

Key Structural Risks

Legal Ownership Conflict

Transfer On chain is not equal to legal registry.

Litigation Risk

Antagonistic claims of ownership might have to be resolved in court.

Settlement Uncertainty

Finality of transfer may come under question in the market.

Liquidity Impact

The investors will be reluctant to deal with assets whose enforcement is not clear.

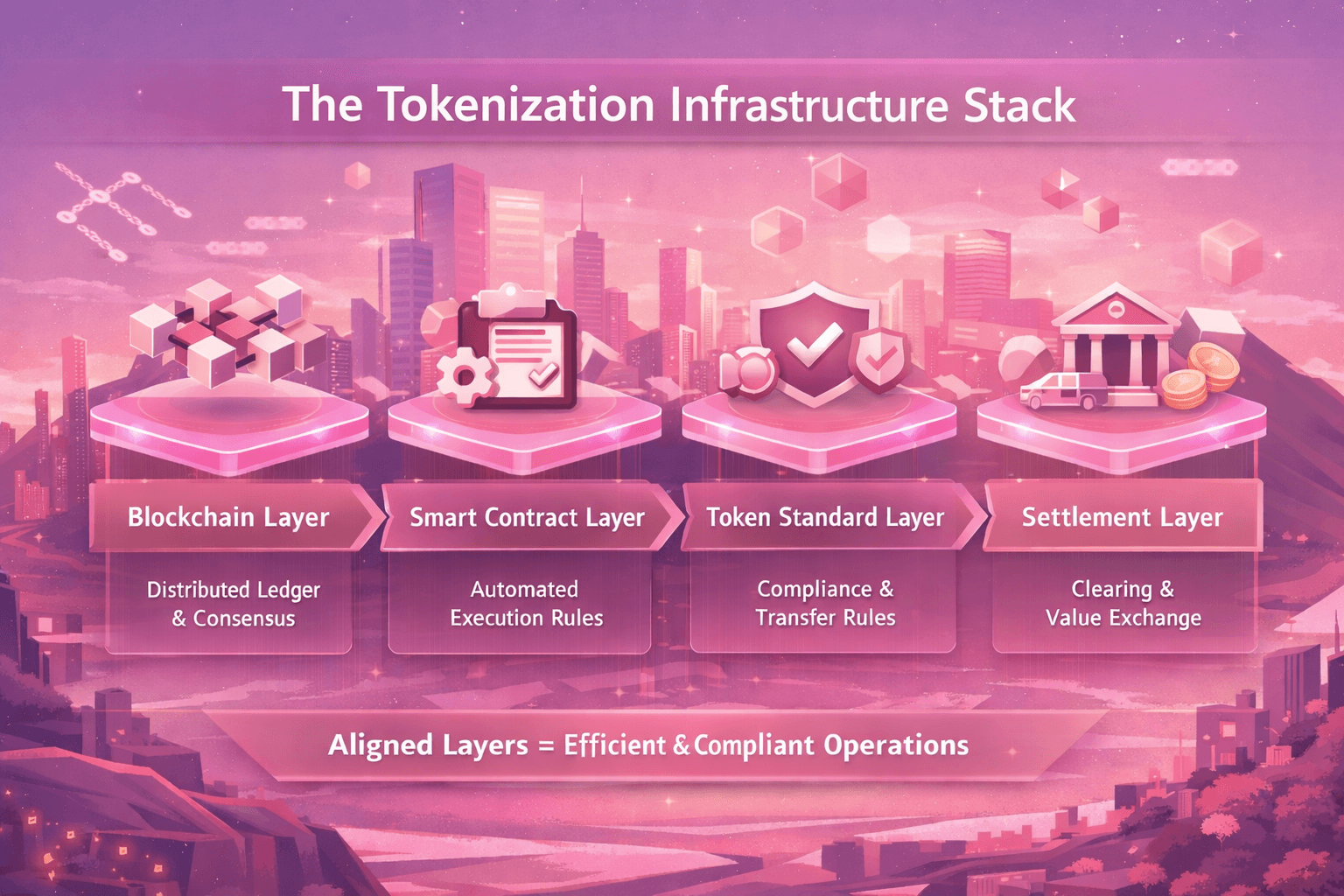

What Is Asset Tokenization Infrastructure?

Asset tokenization infrastructure is the technical foundation enabling digital asset representation. It uses distributed ledger technology to record ownership rights. Digital tokens function as bearer instruments on the ledger. The system replaces centralized registries with consensus mechanisms.

Why Businesses Must Understand Asset Tokenization Infrastructure

Tokenization can improve efficiency across issuance and settlement processes. By tokenizing assets, businesses can represent ownership as digital bearer instruments. These digital representations enable programmable and automated transactions.

However, these benefits do not occur automatically. Tokenization depends on distributed ledger design choices. Distributed ledgers replace centralized registries with consensus mechanisms. Beyond the ledger, additional infrastructure layers shape performance outcomes:

Blockchain layer

Smart contract layer

Token standard layer

Settlement layer

The layers have different functions that handle the asset lifecycle. Lack of alignment between these layers reduces anticipated efficiency benefits. Businesses must understand tokenization infrastructure before implementation.

Overview of the Asset Tokenization Infrastructure Stack

Tokenization infrastructure operates through four interconnected technical layers.

Blockchain Layer

Provides the distributed ledger and consensus mechanism.Smart Contract Layer

Automates predefined execution and verification rules.Token Standard Layer

Defines compliance features and transfer behavior.Settlement Layer

Governs clearing, settlement, and value exchange.

Each layer supports a different stage of the asset lifecycle. Alignment across layers determines operational efficiency outcomes.

Blockchain Layer

Tokenization begins when an asset receives a digital representation. That representation is issued as a blockchain-based token. The token is then recorded on a distributed ledger. Distributed ledger technology maintains synchronized records across participants. The network validates transactions through consensus mechanisms.

This blockchain layer forms the base of tokenization infrastructure. To evaluate this layer, businesses must understand governance models for tokenized assets. These models determine who can issue, validate, and transfer tokenized assets.

Core Properties of the Blockchain Layer

The role of the network is to verify and secure tokens once they are added to the blockchain. The blockchain layer is equipped with three important properties that facilitate tokenization.

Consensus Mechanisms

The consensus mechanism is a method for validating transactions within the network. This mechanism ensures that all parties agree on the same record of ownership. It replaces the centralized clarification process through clearing.

Immutability and Auditability

Immutability means recorded transactions cannot be changed. This protects the ownership history of tokenized assets. Auditability means that this history can be viewed and tracked.

Transaction Finality

Transaction finality determines the permanence of a transfer. Once immutability is achieved, it cannot be changed. Absolute immutability reduces settlement uncertainty in tokenization.

Blockchain Architecture Models for Tokenization

Blockchain infrastructure for tokenization can be evaluated across two dimensions:

Network visibility

Access control

Model | Who Can View? | Who Can Validate? | When It Is Suitable for Tokenization |

Public + Permissionless | Anyone | Anyone | When businesses want global access and open trading |

Public + Permissioned | Anyone | Approved validators only | When visibility is open but validation must be controlled |

Private + Permissioned | Approved participants only | Approved validators only | When assets must follow strict regulatory controls |

Private + Permissionless | Approved participants only | Anyone within network | Rare setup with limited practical use |

Network Visibility

This dimension defines who can view and participate in the network.

1. Public Blockchain

A public blockchain is an open digital network. Anyone can access this network and view any transactions within it. In addition, everyone can also help validate transactions through consensus. Businesses can tokenize assets on a public blockchain. That way, ownership records become publicly verifiable. This can increase transparency among participants.

For companies aiming to gain broad market access, this is the best fit. Public blockchains are often the preferred choice. They enable tokenized assets to reach global participants. Businesses can also easily connect with decentralized finance applications. However, businesses do not directly control the network rules. Network management is shared among participants.

Examples of public blockchains include:

Ethereum

Solana

Polygon

Avalanche

Binance Smart Chain

2. Private Blockchain

A private blockchain is a restricted digital network. Only selected participants can access and validate transactions. The network operator controls participation and governance rules. When businesses tokenize assets on a private blockchain, access remains controlled. Ownership records are visible only to authorized entities.

This is a structure that will help meet institutional compliance requirements. Private blockchains often fit tokenization models involving regulated assets. These blockchains are commonly used in banking and corporate environments. Validation rules and participant roles can be defined within the organization. This allows for a high degree of governance control compared to public networks.

Examples of private or enterprise blockchain frameworks include:

Hyperledger Fabric

R3 Corda

Quorum

Access Control

This dimension defines who can validate and write transactions.

1. Permissionless Network

Permissionless networks allow anyone to participate without prior approval. Each participant can validate transactions through a consensus mechanism. There is no central authority controlling validator access. While tokenized assets operate on a permissionless network, transactions remain publicly verifiable. This model supports transparency and open market participation. It allows tokenized assets to interact with decentralized financial applications.

However, institutions cannot restrict who validates the network. Governance decisions are typically distributed among participants. Permissionless networks are generally associated with public blockchains.

Examples include:

Ethereum

Solana

Polygon

Avalanche

Binance Smart Chain

2. Permissioned Network

A permissioned network restricts participation to approved entities. Network operators decide who can validate transactions. Validator access requires prior authorization. When tokenized assets operate on permissioned networks, transaction control remains limited. Only selected participants can access validation rights. This structure supports regulated environments and institutional governance. Organizations can define compliance rules at the network level. They can also manage participant roles and permissions directly.

Permissioned networks are commonly associated with enterprise blockchain frameworks.

Examples include:

Hyperledger Fabric

R3 Corda

Quorum

Smart Contract Layer

Once a token exists on a blockchain, it needs rules. Smart contracts provide those rules. A smart contract is a program stored on the blockchain. It automatically executes actions when specific conditions are met. In tokenization, smart contracts control how assets are issued and managed.

Smart Contract Encoding

In tokenization, smart contracts define how tokenized assets operate. They contain the core rules that govern the digital asset.

Token issuance logic

The contract defines how tokenized assets are created. It also defines who receives the issued tokens.

Transfer logic

The contract regulates the circulation of tokenized assets among participants. The contract can restrict transfers based on predefined rules.

Dividend and interest distribution

Payments can be automatically distributed to token holders in the contract. This supports systematic tokenization models (e.g., bonds or funds).

Lifecycle events

The contract has the ability to handle maturity, redemption, or burning. These events reflect the life cycle of tokenized assets.

Enforcement of predefined conditions

The contract only takes action if the specifications are met. This ensures that tokenization rules work consistently.

Automation and Compliance

Tokenization often involves regulatory and operational requirements. Smart contracts can automate parts of those requirements.

Encoding regulatory requirements

Compliance conditions can be written directly into the contract. Transfers can be blocked if rules are not met.

Invoice validation example

Smart contracts can verify data before executing payments. This reduces manual verification in tokenized processes.

Service-level agreement automation

The contract can trigger payments when predefined milestones occur. This supports structured tokenization use cases.

Reduction of intermediaries

Automated execution reduces reliance on centralized intermediaries.

Transparency and audit trails

Every contract action is recorded on the blockchain. This improves transparency in tokenization infrastructure.

Token Standard Layer

After defining token rules through smart contracts, the next question is structure. Token standards define that structure. A token standard defines how a token is structured on a blockchain. It sets technical rules such as:

How tokens are created

How they are transferred

What data they contain

What functions they must support

In tokenization, different standards are used depending on the type of asset.

Common Token Standards Used in Tokenization

Token Standard | Asset Type | What It Is Used For | Typical Tokenization Example |

ERC-20 | Fungible tokens | Identical and interchangeable tokens | Tokenized bonds, shares, stablecoins |

ERC-721 | Non-fungible tokens | Unique and indivisible tokens | Tokenized real estate property, certificates |

ERC-1155 | Multi-token | Combines fungible and non-fungible tokens | Platforms issuing mixed asset types |

ERC-1400 | Security tokens | Tokens with built-in transfer restrictions | Regulated securities and investment products |

ERC-3643 | Permissioned security tokens | Identity-controlled token transfers | KYC-based institutional tokenization |

CMTAT | Capital markets tokens | Institutional-grade compliant issuance | Regulated capital market instruments |

ERC-20: Fungible Token Standard

ERC-20 is the most widely used token standard. It is used when all tokens are identical and interchangeable.

Example:

Tokenized shares

Tokenized bonds

Stablecoins

Fund units

If one token equals another token, ERC-20 is usually suitable.

It supports:

Token issuance

Transfers

Balance tracking

This standard is simple and widely compatible with wallets and exchanges.

ERC-721: Non-Fungible Token Standard

ERC-721 is used when each token is unique. Each token represents a distinct asset.

Example:

Tokenized real estate property

Digital collectibles

Unique certificates

No two tokens are identical under this standard.It allows each token to carry its own identity.

ERC-1155: Multi-Token Standard

ERC-1155 allows both fungible and non-fungible tokens in one contract. It is more flexible than ERC-20 or ERC-721.

Example:

A platform issuing both ownership tokens and access rights

Mixed asset structures

It improves efficiency when managing multiple asset types.

ERC-1400: Security Token Standard

ERC-1400 is designed specifically for security tokens. It includes features for:

Transfer restrictions

Compliance checks

Partitioned ownership

This makes it suitable for regulated tokenization.

Example:

Tokenized securities

Regulated investment products

It embeds compliance logic into the token structure.

ERC-3643: Permissioned Security Token Standard

ERC-3643 focuses on identity-based tokenization. It integrates identity verification directly into transfer logic. Only approved participants can hold or receive tokens.

This supports:

KYC-based tokenization

Institutional issuance models

It is often used in regulated environments.

CMTAT (Capital Markets Tokenization Asset Token)

CMTAT is designed for regulated capital markets. It supports compliance features required for financial institutions. It aims to standardize institutional token issuance.

Settlement Layer

The change of the form of representation of assets is accompanied by the change in the form of their issue or settlement. Various systems in a traditional market deal with issuance, clearing and settlement. Through tokenization, these operations may be carried out in the same distributed registry. This helps to remove the necessity to update various registries.

Issuance and Primary Distribution

In traditional finance, issuing securities often requires intermediaries and manual record keeping. With tokenization, new digital securities can be created directly on the blockchain.

When a token is issued, ownership is immediately recorded in the ledger. There's no need to maintain a separate ownership register. Tokens can be distributed directly to investors' digital wallets. This connects issuance and ownership recording into a single system. Simplifying the primary distribution process.

Clearing and Settlement

Once assets are issued, they can be traded. Traditional markets perform clearing and settlement after transactions are executed. Confirmation ensures the terms of the transaction between both parties. Settlement involves the transfer of ownership and the payment process. This procedure usually involves various intermediaries and systems.

Clearing and settlement can be realized in the same distributed ledger system. In this case, ownership is transferred instantly when the transaction is verified. All done through consensus. This eliminates the need to match records across different institutions. Some models allow delivery and payment to be made in the same transaction. This consolidation can reduce the complexity of the post-transaction process.

Cash Leg and Payout Flows

In financial transactions, transfer of ownership is not the only aspect of the process. Another aspect is cash flow. Money transfers associated with asset transfers are referred to as cash flows. Conventionally, both cash and asset settlements are carried out through different systems. In tokenization systems, ownership is stored in a distributed ledger.

However, the associated cash flow can be carried out either on the blockchain or using an external financial system. This results in a hybrid settlement structure in most institutional models. Smart contracts can also be used to record and execute dividend and interest payments. If integrated properly, payment flows will become more transparent and traceable. Therefore, the level of capital flow efficiency is determined by the settlement infrastructure.

End-to-End Issuance Flow in Tokenization

Tokenization infrastructure becomes clearer when mapped across layers. Each step in the issuance process belongs to a specific layer.

Asset Terms Definition (Pre-Infrastructure Stage)

The economic and legal terms of the asset are defined before technical implementation.

Smart Contract Layer (Smart Contract Encoding).

Smart contracts are written in terms of issuance, rules of a transfer, and conditions. This is what determines the behavior of the tokenized asset.

Token Standard Layer Token Standard Selection (Token Standard Layer)

The token standard is chosen in order to define structure and compatibility. This provides wallet and platform interoperability.

Creation and Minting of Tokens (Blockchain Layer + Smart Contract Layer)

The tokens are generated and stored in the blockchain. Minting logic is implemented by the smart contract.

Primary Allocation (Settlement Infrastructure + Blockchain Layer)

Investor wallets are allocated tokens. The ownership updates get registered at the distributed ledger.

Settlement Confirmation

The transaction is validated by consensus. Ledger records complete ownership.

Practical Example: Infrastructure Choice for a Bank

Client: Commercial bank

Objective:

The client wants to adopt a blockchain-based payment system. They want it to facilitate automated online payments. The solution must be able to operate in accordance with regulatory guidelines. It also needs to be integrated with existing banking systems.

Type of network selected: Permissioned blockchain network.

Reasons for choosing a permissioned network:

Banks require controlled participation and clear governance controls. The permissioned model allows for:

Limited validator access.

A clear governance system.

Regulatory compliance.

Integration with internal banking systems.

Operational risk control.

Smart Contract Design:

Smart contracts provide compliance rules. It also provides conditions used in payment execution and minimizes manual validation procedures.

Settlement Approach:

A hybrid settlement system matches on-chain execution with the bank's internal ledger system.

Results:

The infrastructure architecture enables regulated blockchain engagement. This allows for automated payment transactions to occur in a controlled environment. The design is also compatible with existing banking systems.

The Next Phase of Asset Tokenization Infrastructure (2026–2028)

The infrastructure of tokenization is in progress. The development in the future will involve size. It also involves relationships between networks and system design. The important developments could encompass:

Institutional tokenization rollups

Secondary networks are capable of executing higher operations. They continue to use a primary blockchain in security.

Cross-chain token standards

The tokenized assets can be transferred between blockchains using new standards. This decreases isolation of the networks.

Decentralized blockchain design

There are systems that are separated between execution, settlement and the data storage. This has the ability to enhance performance and flexibility in the design of systems.

Interoperability protocols

Various blockchains can be able to communicate and exchange data. Also value through their communication systems. This favors interrelated financial networks.

What Is the Asset Tokenization Process?

Tokenization is the process of recording real-world assets on a distributed ledger. This process creates a digital representation of the asset's economic rights. During the process, the underlying real-world asset remains off-chain. Instead, only the economic rights are transferred onto the chain. A technical bridge connects the asset's traditional ledger to the DLT system. This bridge locks the original asset as collateral for the token. The framework then follows a six-phase structure.

The Asset Tokenization Process Overview

The asset tokenization process follows a structured six-phase model. The phases follow a sequential order. Each phase builds on the outcome of the previous step:

Asset Selection → Asset Evaluation → Regulatory Analysis → Platform Selection → Smart Contracts Development → Token Creation and Issue

Each phase depends on the outcome of the previous step. The sequence ensures legal, technical, and economic consistency.

Step 1: Asset Selection

The tokenization process begins with selecting a real-world asset. This decision shapes the entire tokenization framework. The selected asset class impacts several subsequent steps.

Impact on Asset Evaluation

The asset type determines the appropriate valuation methodology. Different asset classes require different evaluation approaches. For example, real estate and securities adhere to different standards.

Impact on Regulatory Analysis

The asset class determines the applicable regulatory framework. Different assets fall into different legal classifications. Consequently, regulatory obligations vary across asset categories.

Impact on Platform Selection

The asset type can influence the platform selection decision. Technical requirements vary depending on the asset's characteristics. The wrong asset selection can lead to structural complications later on.

Illustrative Examples of Asset Selection Impact

The following table illustrates how asset type influences regulatory and platform considerations.

Asset Example | Regulatory Implication | Platform Implication |

Residential real estate property | Must comply with local property ownership laws and land registry rules | May require permissioned access and a trusted custodian |

Corporate bond issuance | Must comply with securities issuance and investor protection laws | May require smart contracts to automate coupon payments |

Private debt instrument | May require AML and KYC verification for investors | May require restricted transfer rules embedded in smart contracts |

Step 2: Asset Evaluation

After asset selection, the process moves to asset evaluation. This phase defines whether tokenization is viable. The evaluation includes several key components:

Key Evaluation Components

Economic Value Definition

The issuer defines the asset’s economic value. This value becomes the basis for token backing.Ownership Rights Verification

The issuer verifies legal ownership of the asset. The issuer confirms enforceable economic claims.

Market Demand Assessment

The process gauges potential investor demand. It evaluates expected future revenue generation.

Token Feasibility Review

The issuer assesses whether tokenization adds value. The structure must remain economically sustainable.Valuation Method Selection

The chosen method must match the asset type. Incorrect methods may create value discrepancies. Such discrepancies distort on-chain representation.

Asset evaluation determines whether the token structure can be trusted. This phase aligns off-chain value with on-chain representation. Without proper evaluation, tokenization may create structural imbalance.

Step 3: Regulatory Analysis

Along with asset evaluation, regulatory analysis begins. This phase identifies the applicable regulatory framework. Issuers must determine how the assets are legally classified. Different asset classes will fall under different regulatory requirements.

Additionally, issuers must review AML (Anti-Money Laundering) and KYC (Know Your Customer) requirements. This process must comply with applicable data protection regulations. Regulations vary from country to country.

Regulatory Overview Checklist For Tokenization Process

Token and activity classification

Teams classify the token and related activities under local rules.

Offering and disclosure requirements

Teams check disclosure duties for issuance and marketing.

Authorisation and licensing

Teams assess licensing for issuers, brokers, exchanges, and custodians.

AML and CFT program

Teams apply FATF risk-based controls for token flows and intermediaries.

KYC and customer due diligence

Teams verify identities and apply risk-based onboarding controls.

Sanctions controls

Teams screen counterparties and monitor prohibited exposure.

Travel Rule obligations

Teams check data-sharing duties for virtual asset transfers.

Custody and safeguarding

Teams define segregation, control, and loss-handling requirements.

Conflicts management and market integrity

Teams resolve the manipulation, conflicts and fair dealing expectations.

Operational risk and outsourcing risk

Incidents, continuity expectations and vendor risk are handled by teams.

Inter-country regulations and the lack of jurisdiction

Issuer and investor jurisdiction and overlaps of enforcement are mapped in teams.

When banks are involved in bank prudential treatment

The capital and disclosure regulations of crypto exposures are implemented by banks.

Step 4: Platform Selection

The process then selects the technology and platform for the token. This decision defines where the tokenized asset will be placed. The issuer must choose between permissionless and permissioned networks. The issuer must also choose between blockchain and other DLT types. These choices affect access, governance, and transaction execution. The platform choice must match the asset and compliance requirements.

Key Platform Decisions

The issuer selects a permissioned or permissionless network.

The issuer selects blockchain or another DLT system.

Platform selection sets the technical boundaries of token operations. This step prepares smart contract development and token issuance. A mismatched platform may restrict the token’s intended use.

Step 5: Smart Contract Development

Once the issuer has chosen a platform, he or she determines the logic of the token. The rules of operating the token are coded in smart contracts. These contracts are automatically executed upon fulfillment of conditions.

Core Smart Contract Functions

Token Issuance Logic

The contract defines how and to whom tokens are issued.

Transfer Logic

The contract regulates how tokens move between participants.

Distribution Logic

The contract automates dividend or interest payments when required.

Lifecycle Management

The contract manages maturity, redemption, or token burning events.

Compliance Encoding

The contract enforces predefined regulatory and transfer conditions.

Smart contracts operationalize the token structure on the DLT. Incorrect contract design may compromise execution and compliance.

Step 6: Token Creation and Issuance

After smart contract development, token creation begins. This phase models the digital asset on-chain.

Asset Locking Mechanism

The asset should be kept as collateral security. Common mechanisms include:

Technical interoperability between traditional ledger and DLT.

Lock of the off-chain asset on a contractual basis.

Reliable custodian of the tangible property.

These systems guarantee the consistency of values in relation to asset and token.

Tokenization Model Selection

The issuer defines the ownership structure. Different models create different ownership functions.

Fractional ownership divides the asset into multiple tokens

Individual ownership represents the asset as one token

The chosen model determines token quantity and structure.

Offering Structure Definition

The issuer defines how tokens enter the market. Offering structures include:

Public offering, such as an ICO.

Private placement for selected investors.

The offering choice affects distribution scope and access.

Common Risks in the Tokenization Process

Each stage of tokenization introduces specific risks. These risks may affect legal validity and technical execution. Proper coordination across stages reduces structural failure.

Regulatory Uncertainty

Token classification may differ across jurisdictions. Different countries apply different regulatory frameworks. As a result, cross-border issuance increases complexity. Unclear regulation may delay or restrict token issuance.

Ownership and Rights Misalignment

Tokens must reflect real and enforceable ownership rights. Legal documentation must align with on-chain representation. If misaligned, claims may become difficult to enforce. This weakens investor protection and trust.

Valuation Discrepancies

Asset valuation determines the token’s economic backing. Incorrect valuation distorts token pricing at issuance. Overvaluation inflates expectations. Undervaluation reduces demand. Such mismatch creates imbalance between asset and token value.

Smart Contract Errors

Smart contracts govern issuance and transfers. Incorrect code may disrupt execution. Compliance rules may fail if poorly implemented. Testing and audits reduce operational risk.

Asset Custody Risk

The underlying asset must remain properly secured. Custodian failure may weaken token credibility. Weak segregation increases operational exposure.

Market Structure Risk

Offering design affects participation and liquidity. Restricted transfers may limit trading activity. Low demand may reduce post-issuance stability.

Benefits of Understanding the Tokenization Process Before Starting

According to MarketWatch, the tokenized asset market passed $30 billion in 2025. Tokenized U.S. Treasurys reached about $5.5 billion within that growth. Knowing the full process gives clear advantages:

Helps avoid mistakes at the beginning

Keeps legal and technical parts aligned

Improves how the asset is valued

Reduces compliance problems later

Prevents costly changes to the platform

Lowers the risk of smart contract errors

Builds stronger investor trust

Supports long-term project stability

Explore the best asset tokenization platform here.

What is Asset Tokenization Regulation?

Asset tokenization regulation is the legal regulation of digital assets such as tokens. This regulation defines the issuance, trading, and oversight of tokenized assets.

The financial laws that regulators often apply to tokenized assets are existing financial laws. These laws include securities laws, anti-money laundering (AML) laws, and market regulations. In some jurisdictions, new regulatory frameworks now strictly regulate digital assets.

These rules are intended to ensure investor protection and market integrity. They also establish compliance requirements for institutions introducing tokenized assets.

Why Asset Tokenization Regulations Matter for Tokenization

Tokenization converts ownership rights into digital tokens recorded in a distributed ledger. However, tokenization does not change the legal nature of the underlying assets. Regulators still evaluate tokenized assets under applicable financial laws.

Asset tokenization regulatory oversight focuses on several areas:

Investor protection

Market integrity

Financial stability

Anti-money laundering compliance

Regulatory clarity may be the main barrier to institutional adoption. Many institutions often delay tokenization initiatives and the adoption of Web3 technologies. The most common reason is that they want to wait until the compliance structure becomes clearer. For this reason, it is crucial for institutions to understand the asset tokenization regulations.

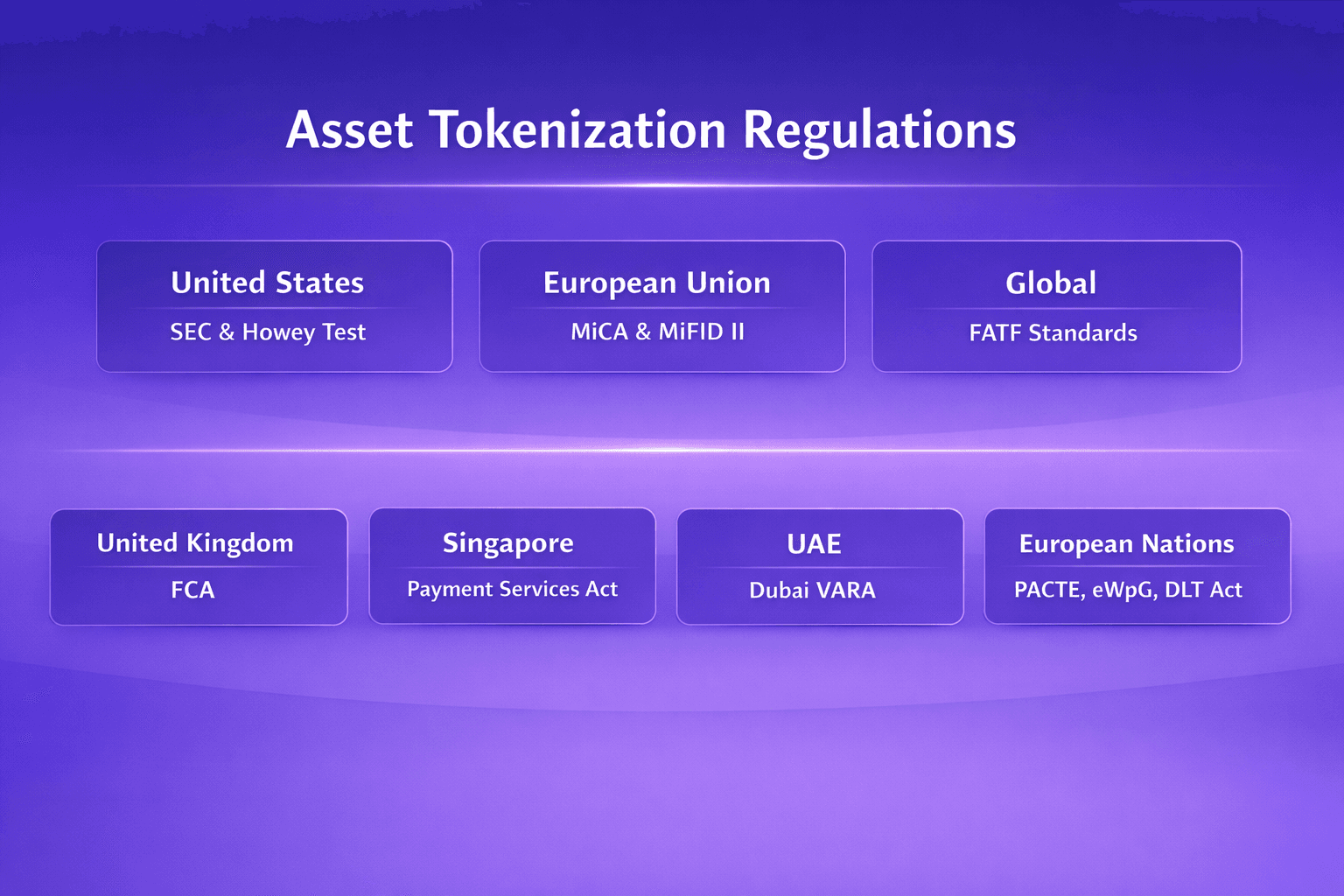

Asset Tokenization Regulatory Overview

Asset tokenization regulations differ across jurisdictions. Some regulators apply existing securities laws to asset tokenization. Other jurisdictions introduced dedicated frameworks for digital assets. The following overview highlights the main regulatory approaches discussed in the research papers.

# | Region | Framework | Main Focus |

1 | Global | FATF | AML and Travel Rule compliance |

2 | United States | SEC | Securities classification |

CFTC | Commodity regulation | ||

FinCEN | AML oversight | ||

3 | European Union | MiCA | Crypto-asset regulation |

MiFID II | Financial instruments regulation | ||

DLT Pilot Regime | DLT market infrastructure | ||

4 | European National | Luxembourg Blockchain Laws | Recognition of DLT for securities processes |

France PACTE Law | Digital asset service provider regime | ||

Germany eWpG | Electronic securities issuance framework | ||

Switzerland DLT Act | Legal framework for digital securities | ||

Liechtenstein TVTG | Token law defining tokens as containers of rights | ||

5 | United Kingdom | FCA | Crypto asset classification |

6 | Singapore | Payment Services Act | Digital asset licensing |

7 | UAE | VARA | Virtual asset supervision |

Different jurisdictions combine traditional financial regulation with new digital asset frameworks. Institutions must evaluate these regulatory environments before launching tokenized assets.

1. Global Compliance Standards

FATF Requirements

The Financial Action Task Force (FATF) sets global standards for anti-money laundering (AML). Also for counter-terrorism financing. These standards apply to digital asset service providers operating tokenization platforms. The FATF guidance introduces several obligations.

Key compliance areas include:

Customer identification and KYC procedures

Transaction monitoring

Suspicious activity reporting

Travel Rule information sharing for digital asset transfers

The Travel Rule obliges the providers to disclose sender and recipient data in transactions. This is a requirement where tokenized assets are transmitted over blockchain networks. Consequently, systems that carry out identity verification should be provided by tokenization platforms.

2. United States Regulatory Framework

The United States regulates tokenized assets through several agencies. The most important authority is the Securities and Exchange Commission.

SEC Oversight

The SEC evaluates whether tokenized assets qualify as securities. If a tokenized asset qualifies, federal securities laws will apply. These rules govern:

Disclosure obligations

Registration requirements

Investor protection standards

Therefore, companies issuing tokenized securities must comply with these rules. These rules are the same rules that apply to traditional securities.

The Howey Test

The Howey test determines whether a tokenized asset qualifies as an investment contract. A token can be considered a security if the following conditions are met:

Investment of money

Joint venture

Expectation of profit

Profit derived from the efforts of others

If all conditions are met, regulators can treat the token as a security.

CFTC Oversight

The Commodity Futures Trading Commission (CFTC) oversees the derivatives and commodities markets. Some digital assets may fall under the commodity classification. Therefore, tokenized commodities or derivatives may fall under the CFTC's jurisdiction.

FinCEN Compliance

FinCEN stands for Financial Crimes Enforcement Network. They focus on AML (Anti-Money Laundering) compliance. To qualify, tokenization platforms must be able to facilitate the transfer of digital assets. This allows them to be recognized as financial services businesses. These obligations include:

AML programs

Transaction monitoring

Suspicious activity reporting

These obligations aim to prevent financial crimes in the digital asset market.

3. European Union Regulatory Framework

The European Union has developed a comprehensive regulatory framework for digital assets. Several regulations impact the regulation of asset tokenization across the EU market.

MiCA Regulation

MiCA stands for The Markets in Cryptoassets Regulation. MiCA is the European Union's framework for crypto assets. MiCA sets out rules for the issuance of crypto assets and the operation of crypto asset services in the European Union.

MiCA regulates several areas:

Issuance of crypto assets

Service providers operating digital asset platforms

Consumer protection requirements

Issuers may be required to publish disclosure documents before offering tokens to the public. These documents explain the token's structure, risks, and holder rights.

MiCA also introduces licensing requirements for crypto asset service providers. Platforms offering trading, custody, or other services must obtain authorization from national regulators.

MiFID II

MiFID II regulates financial instruments across the European Union. Tokenized assets that qualify as financial instruments must comply with MiFID II requirements. These requirements include:

Investor protection rules

Reporting obligations

Trading venue regulations

Therefore, tokenized securities fall under traditional capital markets regulations.

EU DLT Pilot Regime

The EU DLT Pilot Regime allows financial institutions to test DLT in regulated markets. It creates a controlled environment where tokenized securities can operate under supervision.

The framework focuses on several areas:

trading of tokenized securities

settlement using distributed ledger systems

supervised testing of new market infrastructure

This pilot regime helps regulators study how tokenization works in real financial markets. The results may guide future regulation of tokenized securities and digital asset infrastructure.

4. European National Tokenization Laws

Several European countries introduced specific legislation supporting digital asset markets. These laws complement broader EU regulatory frameworks.

Luxembourg Blockchain Laws

Luxembourg introduced several laws that recognize distributed ledger technology in financial markets. These laws enable:

securities issuance through blockchain systems

DLT-based securities settlement

The framework supports tokenization within traditional financial infrastructure.

France PACTE Law

France introduced the PACTE Law to regulate digital asset markets. The law created a voluntary approval regime for digital asset service providers. It also introduced rules for token offerings and digital asset custody.

Germany Electronic Securities Act

Germany introduced the Electronic Securities Act, known as eWpG. The law allows securities to exist as electronic records instead of paper certificates. These records may be maintained on distributed ledger systems. The framework enables tokenized securities issuance within German financial markets.

Switzerland DLT Act

Switzerland implemented legislation supporting distributed ledger markets. The DLT Act recognizes digital securities and introduces a legal framework for DLT trading systems. The law also clarifies insolvency treatment for digital assets.

Liechtenstein TVTG

Liechtenstein introduced the Token and Trusted Technology Service Provider Act. This framework defines tokens as containers of rights. The law provides a technology-neutral legal structure for digital assets.

5. United Kingdom Regulatory Framework

The United Kingdom regulates digital assets through the Financial Conduct Authority.

FCA Crypto Asset Framework

The FCA came up with a crypto asset classification regime. The framework differentiates between:

Exchange tokens

Security tokens

Utility tokens

Security tokens are subject to the current financial regulations. Firms that offer crypto-asset services are also monitored by the FCA. These companies have to adhere to regulatory norms of AML and licensing.

6. Asia Regulatory Framework

Singapore Payment Services Act

Singapore regulates digital assets through the Payment Services Act. The Monetary Authority of Singapore supervises digital payment token services. Companies operating digital asset platforms must obtain licenses under this framework. Compliance obligations include:

AML procedures

risk management controls

customer due diligence

Singapore positioned itself as a regulated environment for digital asset innovation.

7. Middle East Regulatory Framework

Dubai VARA

Dubai has put in place the Virtual Assets Regulatory Authority which oversees digital asset markets. VARA applies to the providers of virtual asset services in Dubai. The licensing requirements are applied to companies offering services in the following:

Digital asset trading

Custody

Brokerage

Its framework focuses on creating a controlled space of digital assets.

Emerging 2026 Regulatory Trends

Regulators are tightening digital asset oversight during 2026 planning cycles. Several trends affect tokenization and asset tokenization regulations.

MiCA transition deadlines are approaching across the EU.

According to ESMA, some firms can operate until 1 July 2026 under grandfathering.

MiCA passporting will shape cross-border crypto service expansion.

According to ESMA, authorised CASPs can serve multiple EU states under one licence.

FATF tightened Travel Rule alignment and payment transparency expectations.

FATF updated Recommendation 16 changes during June 2025 plenary.

Asset Tokenization Regulatory Burden Comparison

Different regulatory frameworks impose varying levels of compliance on tokenization projects. The following comparison highlights how major frameworks approach asset tokenization regulation.

Regulatory Framework | Jurisdiction | Token Classification | Regulatory Burden |

SEC / Howey Test | United States | Tokens evaluated as securities through the Howey test | Case-law driven interpretation and enforcement risk |

MiCA | European Union | Crypto-assets regulated under a unified EU framework | Extensive documentation and authorization requirements |

MiFID II | European Union | Tokenized financial instruments treated as securities | Full capital markets regulation requirements |

VARA Framework | Dubai (UAE) | Virtual asset service providers regulated through licensing | Licensing and operational approval requirements |

MAS Payment Services Act | Singapore | Digital payment token services regulated under payment laws | Strict AML supervision and licensing requirements |

Regulatory Risk Matrix for Issuers

This matrix summarises issuer decision risk across major jurisdictions. The ratings reflect how each regime works in practice. They do not reflect legal advice.

Risk area | US | EU | Singapore | UAE |

Classification uncertainty | High | Medium | Medium | Medium |

Licensing complexity | Medium | High | High | Medium |

Enforcement predictability | Medium | Medium | Medium | Medium |

Basis for the ratings:

US classification uncertainty is High

US securities analysis often relies on Howey and case-driven interpretation.

EU classification uncertainty is Medium

MiCA establishes a harmonised framework for crypto-assets. MiFID II still applies to financial instruments.

EU licensing complexity is High

MiCA introduces authorisation obligations and passporting for service providers.

Singapore licensing complexity is High

MAS sets detailed AML and CFT requirements for digital payment token services.

UAE licensing complexity is Medium

VARA uses a defined application process with staged steps and documentation.

Enforcement predictability stays Medium across regions in this matrix

The sources describe active supervision. They do not provide a comparable scoring method.

Compliance Requirements for Tokenization

Regulators at cross-jurisdictions concentrate on parallel principles of compliance. The tokenization platforms should consider a number of operational prerequisites. Standard compliance requirements are:

Customer identity authentication.

AntiMoney laundering monitoring.

Licensing of digital asset service providers.

Investor protection and disclosures.

Custody and settlement protection.

Such requirements are intended to secure the investors and to liberalize the financial market.

Compliance processes should be developed ahead of tokenization assets issuance. Especially in institutions that intend to implement tokenization programs.

What Is Asset Tokenization Governance?

Asset Tokenization Governance is the decision-making layer in the asset tokenization process. Asset tokenization governance determines how stakeholders control and coordinate the tokenized system.

Governance determines:

Who can submit proposals

Who can vote

How votes are counted

How decisions are implemented

Asset tokenization distributes ownership or participation through tokens. Governance determines how these tokens are converted into voting rights. This article describes governance as a structured framework. This framework manages transparency, participation, and system updates.

Asset Tokenization Governance Models in Tokenization Overview

In this article three broad categories of asset tokenization governance models are found. The different models are balanced in terms of transparency. Also efficiency and participation of stakeholders.

Model Type | Decision Location | Execution Method | Main Strength | Main Risk |

On-chain | Blockchain | Smart contract execution | Transparency | Voting concentration |

Off-chain | Forums or committees | Manual coordination | Deliberation | Slower decisions |

Hybrid | Mixed structure | Combined execution | Balance | Structural complexity |

Core Asset Tokenization Governance Models in Tokenization

1. On-Chain Governance

Blockchain-based governance involves the use of blockchain to implement governance decisions. The system uses smart contracts as a form of automation. Direct voting takes place with token holders. The voting power is normally an expression of token holdings.

Proposals, which are approved, run automatically via code. Automation minimizes the use of hand work. It is a structure that enhances transparency and minimizes human error. Automation was one of the strengths of the research.

However, token concentration creates structural risk. Large holders may control majority voting power. This control may centralize decision influence. Centralization may favor minority interests. Therefore, automation does not remove governance imbalance.

2. Off-Chain Governance

Off-chain governance makes decisions outside of the blockchain. This process relies on human coordination. Stakeholders discuss proposals in forums or meetings. Community discussions shape the final decision. Voting can be done through informal agreements. Implementation often requires manual execution.

This model allows for broader discussion and more detailed input. It supports qualitative analysis before change. However, coordination can be slower. Human processes reduce the speed of implementation. Dominant participants can influence the outcome. Influence can disrupt the balance of stakeholders. Bitcoin demonstrates dominant off-chain governance.

3. Hybrid Governance

Hybrid governance combines on-chain execution with off-chain deliberation. This model integrates automation with structured discussion. Stakeholders first discuss proposals off-chain. Formal voting can be conducted on-chain. Approved proposals can be executed automatically via smart contracts. Automation maintains transparency and audit trails.

This model seeks to balance speed and inclusion. This model leverages the advantages of both approaches. However, the hybrid structure increases design complexity. Different layers require clear coordination rules.

Polkadot is an example of a layered governance structure. MakerDAO also combines on-chain voting with off-chain analysis. A clear structure is essential in hybrid systems.

Asset Tokenization Governance Mechanisms and Design Tools

The forms of governance must have formal systems. The article singles out certain tools that determine fairness in decision making.

Key Governance Mechanisms:

Token-based voting

Quadratic voting

Approach systems of proposals.

Decentralized program architecture like DAOstack.

Quadratic voting minimizes the power of big token holders. It makes changes in the voting weight as compared to concentration of tokens. This is an effort by this mechanism to restrain power imbalance. It enhances subjective fairness during decision-making.

DAOstack is open-source modular governance infrastructure. It provides proposal submission and voting logic. They facilitate the inclusion of more people in the decision making process. This tool does not supersede governance models. It perfected the way governance is conducted.

Governance Implementation Framework

Asset tokenization governance requires structured implementation. Each stage builds on the previous stage.

1. Define Governance Objectives

Governance objectives define the system’s decision purpose. They clarify what governance must control or manage. Objectives align governance with project goals. Clear goals prevent structural ambiguity. Without defined objectives, governance lacks direction.

2. Identify Stakeholders

Stakeholders represent participating parties in the ecosystem. Identification clarifies who holds influence or voting rights. Different stakeholders may hold different interests. Governance must account for those interests. Clear stakeholder mapping improves balance and representation.

3. Select Governance Mechanisms

Governance mechanisms determine how decisions occur. Examples include on-chain voting or hybrid structures. Project size and complexity influence mechanism selection. Stakeholder diversity also affects design choice. The selected model must align with governance objectives.

4. Deploy and Test the System

Deployment implements governance protocols in practice. Testing evaluates structural performance. Simulations or pilot phases may expose weaknesses.Early testing reduces operational disruption. Testing validates whether assumptions match real behavior.

5. Monitor Performance and Refine

Monitoring tracks governance effectiveness over time. Feedback mechanisms gather stakeholder input. Evaluation identifies structural gaps or inefficiencies. Refinement adjusts governance to changing conditions.

Governance evolves through feedback and observation. Therefore, asset tokenization governance remains adaptive. It requires ongoing review and adjustment.

Asset Tokenization Governance Trade-Offs

Asset tokenization governance introduces structural trade-offs. Different governance models create different risks. These risks affect decision quality and system balance. Design choices determine governance outcomes.

Voting power concentration

Slow decision cycles

Dominant participant influence

Structural complexity

Regulatory alignment challenges

1. Voting Power Concentration

On-chain governance links voting power to token ownership. More tokens usually mean more influence. If a few people hold many tokens, they gain control. Their votes can outweigh others.

The system stays transparent. But power may become unbalanced. Transparency does not always mean fairness.

2. Slow Decision Cycles

Off-chain governance depends on discussion. People debate before making decisions. Discussion improves understanding.

However, it takes time. Long discussions delay action. Urgent changes may move slowly. Careful debate may reduce speed.

3. Dominant Participant Influence

Off-chain discussions allow open participation. Anyone can contribute ideas.

However, strong voices may dominate conversations. Influential members may shape outcomes. This influence may not reflect the whole community. Participation does not always mean equal power.

4. Structural Complexity

Hybrid governance combines two systems. It mixes discussion with automated voting. This design tries to balance speed and fairness.

However, it becomes more complex. More layers require clearer coordination. Poor coordination creates confusion. Complex systems need careful design.

5. Regulatory Alignment Challenges

Some tokenized systems operate within legal frameworks. Governance design may interact with external obligations. Potential alignment challenges include:

Legal jurisdiction differences.

Custodian control over real-world assets.

Token-holder and issuer decision conflicts.

Voting limits under certain regulatory structures.

These factors may influence governance design. They may restrict how voting rights operate. Governance must reflect both system rules and external constraints. Poor alignment may create operational friction.

Benefits of Effective Asset Tokenization Governance

Effective governance creates real benefits in tokenized ecosystems. Clear rules improve how people work together.

1. Stronger Stakeholder Engagement

Good governance gives people a voice. Clear voting systems encourage participation. When people feel included, engagement increases. Active communities support healthier ecosystems.

2. Better Adaptability

Governance allows systems to change over time. Clear processes make updates easier. Structured voting helps respond to new challenges. Adaptable systems survive longer.

3. Greater Stability

Defined rules reduce confusion. Clear decision paths prevent disorder. The research links governance to higher project stability. Stable systems handle pressure more effectively.

4. Long-Term Sustainability

Governance supports long-term coordination. Balanced decisions protect ecosystem health. Sustainable systems grow steadily over time. Strong governance supports lasting success.

Effective asset tokenization governance improves trust. Structured processes increase transparency. Transparent systems build confidence among participants. Confidence strengthens ecosystem durability. Therefore, governance acts as a stability foundation.

Asset Tokenization Governance Real-World Examples

Tezos – On-Chain Governance

Tezos uses on-chain governance. Token holders vote directly on protocol upgrades. Approved changes execute automatically through blockchain code.

Key characteristics:

Voting happens on the blockchain

Smart contracts execute approved decisions

Transparency remains high

Main benefit:

Automation improves upgrade speed.

Main limitation:

Large token holders may gain more influence.

Bitcoin – Off-Chain Governance

Bitcoin relies mainly on off-chain governance. Developers and community members discuss proposals. Changes require voluntary software adoption.

Key characteristics:

Discussions happen outside the blockchain

Consensus forms through agreement

Execution depends on human coordination

Main benefit:

Community discussion improves decision depth.

Main limitation:

Decision speed may decrease.

MakerDAO – Token-Based Governance

MakerDAO uses token-based governance. Token holders vote on system parameters. Voting directly affects operational rules.

Key characteristics:

Token holders influence system decisions

Voting shapes risk and policy settings

Participation drives governance direction

Main benefit:

Token holders actively control decisions.

Main limitation:

Voting power links to token ownership.

Polkadot – Hybrid Governance

Polkadot uses a hybrid governance structure. It combines on-chain voting with councils and committees.

Key characteristics:

Public referenda for token holders

Councils oversee specialized functions

Multiple governance layers operate together

Main benefit:

The structure balances automation and representation.

Main limitation:Multiple layers increase coordination complexity.

Tokenize Your Business Assets with TokenMinds

TokenMinds supports businesses in designing and implementing tokenization strategies. This includes asset structuring, smart contract, or blockchain integration. Whether you are evaluating tokenized securities or planning enterprise blockchain infrastructure.

Visit our asset tokenization page today. Or schedule a free consultation with our expert here.

FAQs on Assets Tokenization

What is tokenization of assets?

Tokenization of assets creates a digital representation of ownership on a blockchain. The token reflects ownership or economic rights in an asset.

Does tokenization of assets move assets fully on-chain?

Tokenization of assets does not always move ownership fully on-chain. Many assets remain partly off-chain. Legal title often stays in traditional registries.

What assets qualify for tokenization of assets?

Tokenization of assets applies to assets with defined ownership rights. Ownership must be legally recognized and transferable. Examples include equities, bonds, real estate, and commodities.

How does the asset spectrum relate to tokenization of assets?

The asset spectrum explains structural positions in tokenization of assets. Assets may be conventional, hybrid, or digitally native. Position depends on representation, enforcement, and transfer design.

Are stablecoins part of tokenization of assets?

Stablecoins are commonly cited in tokenization of assets discussions. They operate in hybrid structures. Their tokens circulate on-chain while reserves remain off-chain.

What is the tokenization infrastructure?

Tokenization infrastructure is the technical stack behind asset tokenization. It supports issuance, ownership recording, and settlement on distributed ledgers. It includes blockchain, smart contracts, token standards, and settlement systems.

Why does tokenization need to use more than one layer?

Each layer performs a different role. The blockchain records ownership. Smart contracts define asset rules. Token standards structure tokens. Settlement infrastructure governs issuance and transfers.

How is settlement different in tokenization?

Settlement can occur directly on the distributed ledger. Consensus validates transactions and updates ownership records. This can reduce reconciliation and reliance on intermediaries.

What is the difference between tokenization and securitization?

Securitization converts assets into tradable financial securities. Tokenization represents assets digitally on distributed ledgers.

Tokenization focuses on digital issuance and on-chain transfer. Securitization relies on traditional financial infrastructure.

Is tokenization legal?

Tokenization may be legal depending on jurisdiction. Legality depends on asset classification and local regulations. Issuers must follow securities, AML, and data laws. Cross-border issuance increases regulatory complexity.

How are tokenized assets backed?

Tokenized assets are backed by real-world assets. A technical ramp locks the off-chain asset. In some cases, a trusted custodian safeguards the asset. The token represents economic rights to that asset.

Is asset tokenization legal in the United States?

Yes. Asset tokenization is legal when it follows existing financial regulations. Regulators evaluate tokenized assets under federal securities laws and other financial rules. If a tokenized asset qualifies as a security, issuers must comply with SEC requirements. These include disclosure obligations and investor protection rules.

Does MiCA apply to tokenized securities?

MiCA regulates many crypto assets in the European Union. However, tokenized securities usually fall under existing financial regulations. If a tokenized asset qualifies as a financial instrument, MiFID II rules apply. These rules govern trading, disclosure, and investor protection.

What license is required for a tokenization platform?

Licensing requirements depend on the jurisdiction and the services provided. Platforms offering trading or custody services usually require regulatory authorization. In the European Union, crypto-asset service providers must obtain authorization under MiCA. Other jurisdictions require licenses for digital asset service providers.

How does the FATF Travel Rule apply to tokenized assets?

The FATF Travel Rule applies to digital asset transactions between service providers. Platforms must collect and share sender and receiver information during transfers. These rules support AML monitoring and financial crime prevention. Tokenization platforms must implement compliance procedures for these requirements.

Are tokenized assets considered securities?

Some tokenized assets qualify as securities under financial regulations. Regulators evaluate the economic structure of the asset. If the token represents investment rights or profit expectations, it may qualify as a security. In such cases, securities regulations apply to issuance and trading.

What is asset tokenization governance?

Asset tokenization governance explains how decisions are made. It sets rules for voting and changes. It shows who can vote and how decisions happen.

On-chain vs. off-chain governance, what is the difference?

On-chain governance occurs within the blockchain. Smart contracts are used to vote by people. Off-chain governance occurs out of the blockchain. Individuals deliberate and reach the consensus before making modifications.

What is the relevance of governance in tokenization?

There is a system order maintained by governance. It assists individuals to make decisions equitably. Lack of good governance may bring about imbalance or delays. Good governance enhances stability and coordination.