TL;DR

Tokenized collateral shifts operations from batch cycles to continuous workflows. Margin calls move from end-of-day to real-time triggers. Substitutions become granular and programmable. Settlement windows compress from T+1 to near-instant finality. This is a workflow redesign, not a speed upgrade.

From Batch Margin Calls to Continuous Collateral Management

Most collateral operations run on a batch model. Margin calls go out once or twice a day. Teams calculate exposure at fixed intervals. They send calls in the morning. They wait hours for responses. The institution carries unhedged exposure during that lag.

This lag is structural. Legacy systems process data slowly. Batch scheduling adds time. Overnight reconciliation adds time. Manual confirmation chains add time. The margin call rhythm does not match intraday market movement.

Tokenized collateral changes this at the infrastructure level. Smart contracts embed margin triggers into position monitoring logic. A position breaches a threshold. The system makes a call. It automatically moves eligible collateral. The process is continuous, not scheduled.

This operational change alters daily operating routines. Collateral managers move away from morning task lists to track risk limits all day long. The workflow changes from reactive to continuous. Teams need new tooling. They need new escalation protocols. They need clear rules for automated versus manual intervention.

Margin Call Timing: Batch vs. Continuous

Dimension | Batch Model | Continuous Model |

Call frequency | Once or twice daily | Event-triggered, continuous |

Exposure calculation | Fixed interval snapshots | Real-time position monitoring |

Response window | 2 to 4 hours typical | Near-instantaneous for automated calls |

Manual intervention | Required for most calls | Reserved for exceptions and disputes |

Capital at risk during lag | High | Materially reduced |

The SWIFT Institute working paper highlights structural tension in current arrangements. Settlement lags force institutions to maintain prefunded positions. They hold buffer capital to cover exposure during the gap. Tokenized infrastructure can reduce that gap.

Continuous margin calls change counterparty relationships. Both sides must agree on trigger logic before going live. They must agree on eligibility parameters. They must agree on dispute resolution procedures. Operational readiness at the counterparty level becomes a prerequisite.

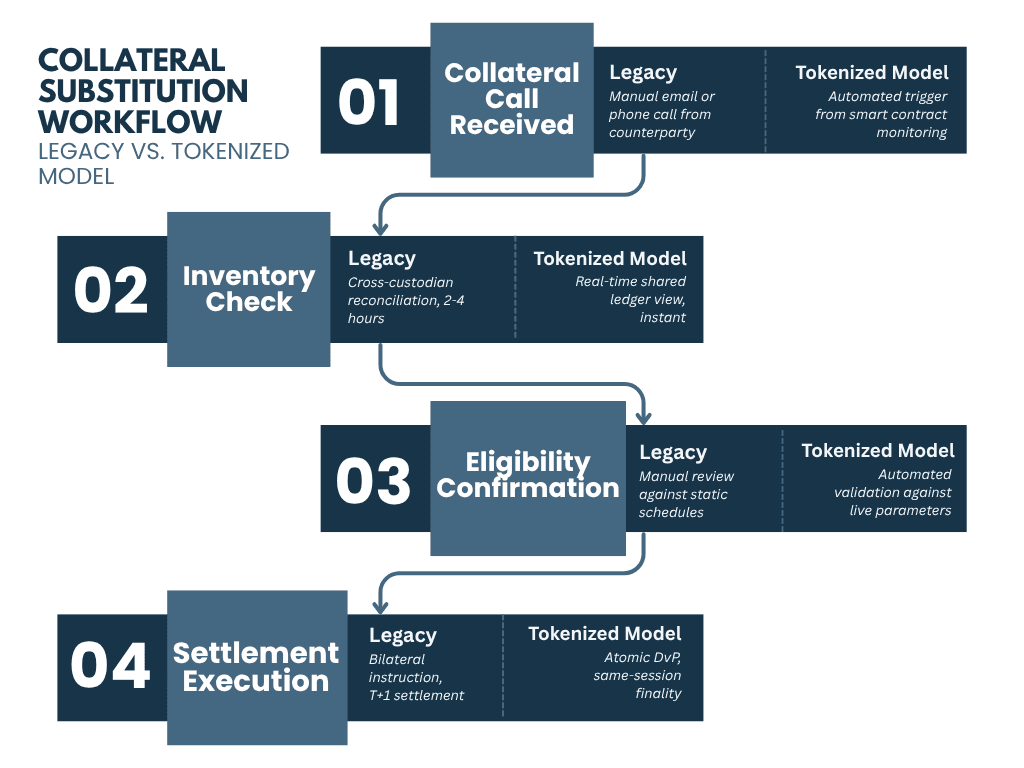

Micro-Substitutions and Granular Collateral Control

Legacy substitution processes work at the asset level. An institution swaps one bond for another. The process requires bilateral agreement. The process requires manual approval. The transfer takes a full business day to clear, so asset swaps happen rarely. The friction is too high relative to the optimization benefit.

Tokenized collateral enables micro-substitutions. A collateral manager can reallocate a specific notional amount within a basket. The system replaces part of an asset pool. This happens when rules change, risk discounts shift, or new trading signals arrive.

Substitution Granularity Comparison

Substitution Granularity Levels

Level | Legacy Capability | Tokenized Capability |

Asset swap | Yes, bilateral and manual | Yes, programmable and automated |

Notional slice | No | Yes, configurable thresholds |

Basket rebalancing | No | Yes, rule-based and continuous |

Eligibility-driven routing | No | Yes, embedded in smart contract logic |

Haircut-adjusted substitution | Manual recalculation | Automated, real-time |

The IMF notes that smart contracts embed eligibility checks and risk parameters directly. This keeps asset swaps running smoothly all day. Teams need a system that handles routine moves on its own when the market changes.

Evaluate the specific economic gains from granular substitution in this workflow analysis: Tokenized Collateral Operational Gains in Securities Financing.

Operationally, micro-substitution requires a well-maintained eligibility matrix. The smart contract logic only works if underlying rules are current and correctly encoded. Teams must invest in eligibility governance as a core function.

Why Collateral Mobility Matters for Intraday Liquidity

Collateral mobility transforms static asset pools into dynamic liquidity sources. Institutions currently trap significant capital in unproductive buffers. Industry analysis suggests firms hold 7% excess collateral as an operational buffer to cover settlement lags. Another 25% of collateral usage generates no return because assets sit idle between calls.

Tokenized collateral releases this trapped capital. Cross-venue reuse allows teams to deploy the same asset across multiple financing relationships within a single session. A bond pledged for a repo trade at 9 AM can be released and pledged for a margin call at noon. This can reduce dependency on overnight batch windows that legacy systems enforce.

Cross-border movement can improve when legal and settlement rails align. Traditional transfers face jurisdiction-specific cutoffs and intermediary delays. Tokenized movement follows global network hours. Institutions may reduce intraday liquidity drag when assets can move across borders outside traditional CSD windows.

Read how shared settlement infrastructure resolves intraday funding gaps and collateral mobility bottlenecks: On-Chain Repo for Intraday Funding and Collateral Mobility.

Collapsing Settlement Windows: From T+1 to Near Real-Time

The shift to T+1 in North American equity markets compressed settlement cycles. It exposed operational limits of legacy infrastructure. Trade confirmation deadlines moved earlier. Collateral availability requirements tightened. Cross-border participants faced new time zone pressures.

Tokenized settlement takes this further. Atomic delivery-versus-payment removes the gap between asset transfer and cash settlement. Both legs complete simultaneously on-chain. There is no intermediate state where one party has delivered but the other has not. Settlement finality occurs at the transaction level, not at the end of a batch cycle.

Deutsche Bank notes that digital networks let firms use the same collateral many times a day across different markets. This makes assets move much faster. Firms can shift assets late in the day to cover margin calls or payments. This removes the need to keep large cash cushions just in case.

Settlement Window Compression Stages

Stage | Settlement Model | Typical Window | Key Operational Implication |

Legacy | T+2 | 48 hours | Large prefunding requirement |

Current standard | T+1 | 24 hours | Earlier confirmation deadlines |

Tokenized (near-term) | Same-day | Hours | Intraday liquidity management required |

Tokenized (target state) | Atomic DvP | Minutes to seconds | Fail buffers may shrink when settlement becomes atomic |

Fast trade deadlines create asset shortages for teams stuck on old systems. A counterparty settles in minutes. An institution's internal systems batch-process collateral movements overnight. The mismatch creates fails and operational exceptions.

The Canton Network group showed cross-border intraday repo using tokenized Gilts and tokenized deposits. Participants included LSEG, Euroclear, Citadel Securities, Tradeweb, Societe Generale, Virtu Financial, DTCC, Digital Asset, Cumberland DRW, TreasurySpring, Archax, and IntellectEU. These tests cut out dead time, which is the period when cash sits idle between making a trade and finishing it. The proof-of-concept results confirm atomic settlement is operationally achievable in institutional contexts.

Map the specific workflow changes required to move from batch to continuous operations.

What the Target Operating Model Must Change

Moving to tokenized collateral requires more than new technology. The operating model must change first. The table below maps specific workflow areas that require redesign.

Operating Model Redesign Map

Workflow Area | Current Model | Tokenized Collateral Model |

Margin trigger | Scheduled call cycle | Threshold-based event trigger |

Eligibility check | Manual schedule review | Encoded eligibility matrix |

Substitution | Bilateral approval | Rule-based exception flow |

Settlement | Batch window | Atomic or same-session settlement |

Exception handling | End-of-day queue | Real-time monitoring |

Legal workflow | Static CSA process | Updated DvP and trigger terms |

Reporting | End-of-day reconciliation | Intraday position visibility |

This redesign shifts teams from reactive batch processing to proactive continuous monitoring. Each change requires new tools, new protocols, and new counterparty coordination.

Why Interoperability Determines Tokenized Collateral Adoption

Tokenized collateral cannot exist in isolation. It must connect to legacy custody systems, central bank money rails, and existing messaging standards. SWIFT and DTCC emphasize interoperability as the primary adoption driver. Institutions reject siloed token networks that fail to integrate with current infrastructure.

Hybrid settlement architecture bridges the gap. Permissioned DLT networks handle the tokenized asset layer. Traditional rails handle fiat settlement and final regulatory reporting. ISO 20022 messaging standardizes the data exchange between these layers. This ensures that tokenized collateral movements translate correctly into core banking ledgers and risk systems.

Tokenized deposits play a critical role here. They provide the cash leg for atomic delivery-versus-payment without requiring stablecoin volatility. Central bank digital currencies and commercial bank tokenized deposits both offer programmable money rails that match the speed of tokenized assets. This alignment allows institutions to settle trades in seconds while maintaining regulatory compliance.

Multi-chain interoperability also matters for scale. Collateral pools span multiple jurisdictions and asset types. A unified collateral management layer must read positions across different permissioned ledgers. Standardized APIs and shared state protocols enable this cross-chain visibility. Institutions demand this flexibility before committing production volumes.

Operational Readiness for Continuous Settlement

Moving to continuous collateral management requires more than deploying new technology. The operating model must change first. Three areas require specific preparation.

First, eligibility governance needs to become a real-time function. Old systems update asset rules once a day or once a week. New systems feed rule changes into smart contracts instantly. Any delay creates a gap between system choices and true company risk rules. Operations teams have to build processes to manage this lag.

Second, exception management protocols must shift from reactive to proactive. Batch systems generate exceptions at defined points in the cycle. Continuous systems generate exceptions at any time. Teams need monitoring tools that surface issues in real time. They need escalation paths that work outside standard business hours.

Third, counterparty connectivity and legal infrastructure must enable atomic settlement. Both sides of a bilateral trade can only settle atomically if they operate on compatible infrastructure. Institutions must evaluate counterparty readiness when considering tokenized collateral. Legal documentation must be updated to incorporate the new settlement mechanics.

Continuous systems introduce unique failure modes that batch systems avoid. Smart contract trigger misfires can execute margin calls on stale data. Stale eligibility matrices may reject valid collateral during volatile markets. Oracle latency can delay price feeds, causing automated substitutions to fail. Conflicting counterparty logic can trigger cascading automated liquidations. Intraday liquidity exhaustion loops occur when rapid margin calls drain available collateral across connected pools. Teams must stress-test these scenarios before production deployment.

Operational Readiness Checklist for Continuous Settlement

Readiness Area | Key Requirement | Status Indicator |

Eligibility governance | Real-time update capability | Daily update cycle still in use |

Exception management | 24-hour monitoring and escalation | Batch exception window active |

Counterparty connectivity | Compatible settlement infrastructure | Bilateral assessment completed |

Legal documentation | Atomic DvP terms reflected | ISDA or CSA amendments confirmed |

Internal systems | Intraday collateral position data | Overnight batch replaced |

Risk policy alignment | Continuous margin trigger parameters | Risk committee sign-off required |

The CFTC issued guidance in December 2025 on tokenized collateral. The guidance clarifies regulatory concerns for tokenized assets used as collateral in derivatives markets. It covers eligible assets, legal enforceability, custody and control, haircuts, valuation, and operational risks. It also states that each tokenized asset or structure must be analyzed individually. This gives US operations teams a clearer review framework.

Institutions that address readiness gaps before deployment avoid the most common failure mode. That failure mode is a tokenized front end sitting on top of a batch-driven back office. That configuration creates new reconciliation problems without delivering efficiency gains.

Request a collateral ops redesign session. TokenMinds maps current collateral workflows, margin triggers, eligibility rules, exception paths, counterparty readiness, and settlement integration gaps. Contact us at https://tokenminds.co/contact.

Frequently Asked Questions

Q: What is the primary operational change when moving from batch to continuous margin calls?

A: The primary change is timing. Batch systems generate margin calls at fixed intervals, typically once or twice a day. Continuous systems trigger calls in real time based on position thresholds. This setup requires new tracking tools, fresh error rules, and pre-set automated logic between both trading firms.

Q: How do micro-substitutions differ from standard collateral substitutions?

A: Standard substitutions swap one asset for another at the full position level. Micro-substitutions allow teams to reallocate a specific notional amount within a position. Triggers include eligibility changes, haircut updates, or optimization signals. Smart contracts run the process, so both sides can skip manual checks for basic asset moves.

Q: What does atomic delivery-versus-payment mean for settlement fails?

A: Atomic DvP settles both parts of a trade at once. There is no middle step where an asset moves without the cash, or the cash moves without the asset. This reduces delivery and payment mismatch risk in legacy workflows. Because of this, firms may reduce some prefunding buffers, depending on controls.

References

SWIFT Institute Working Paper: Analysis of tokenized settlement mechanics and real-time infrastructure implications for collateral management. https://www.swift.com/swift-resource/252290/download

IMF Note 2025/011: Smart contract-embedded eligibility checks and real-time margin calls in institutional contexts. https://www.imf.org/-/media/files/publications/ftn063/2025/english/ftnea2025011.pdf

Deutsche Bank Flow: How tokenized assets transform liquidity management through increased collateral velocity. https://flow.db.com/Topics/trust-and-securities-services/how-tokenised-assets-transform-liquidity-management

CFTC December 2025 Staff Guidance: Regulatory framework clarification for tokenized collateral settlement finality and custody treatment. https://www.cftc.gov/csl/25-39/download

Canton Network February 2026: Industry working group completes first cross-border intraday repo with tokenized Gilts https://www.canton.network/canton-network-press-releases/cantons-industry-working-group-advances-cross-border-collateral-mobility-on-canton

DTCC/Clearstream/Euroclear: Interoperability requirements for digital asset adoption across ledgers, contracts, networks, and traditional infrastructure. https://www.dtcc.com/-/media/interoperable-digital-asset-securities-white-paper.pdf

SIFMA/CCMA/ISDA T+1 Booklet: Operational framework and compliance implications of the May 2024 T+1 transition for collateral availability. https://www.sifma.org/resources/guides-playbooks/t1-settlement-cycle-booklet

Nasdaq, & The ValueExchange. (2023). The $340 million case for tokenized collateral: What industry steps are needed for adoption [Research report]. https://www.nasdaq.com/solutions/fintech/resources/reports/making-the-case-for-tokenized-collateral