Key takeaways:

The DTCC, Clearstream, and Euroclear framework shows how digital assets should move across financial systems, with clear rules for asset ownership, compliance, data standards and participant roles.

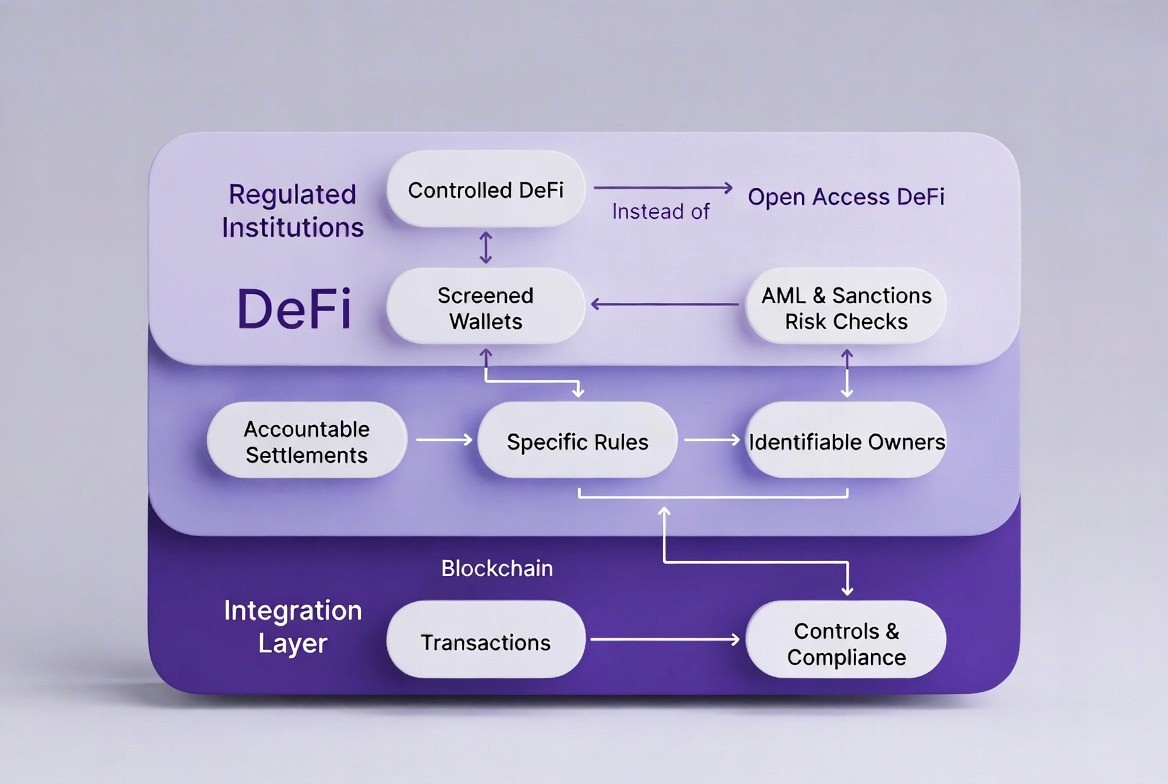

For institutions, Regulated DeFi integration means using blockchain networks for settlement while keeping compliance checks, internal records and operational control.

Institutions integrate DeFi by adding four operational systems: a stablecoin settlement rail, wallet compliance screening, automated reconciliation between on chain transactions and internal records, and clear ownership for every settlement step.

On March 4, 2026, DTCC, Clearstream, and Euroclear published a joint white paper with Boston Consulting Group. They called for a shared framework for digital asset interoperability across five dimensions: asset ownership, mobility, compliance, data standards, and role consistency.

DTCC is already minting U.S. Treasury securities on a live blockchain. Goldman Sachs, HSBC, and the European Investment Bank are active participants. The paper is not a forecast. It is a governance directive from institutions already operating in the space.

The window to build ahead of standardization is open. The four integration steps in this guide translate those framework requirements into operational systems, an implementation path explained in this agentic payment system design.

What Regulated DeFi Means for Institutions

When financial institutions talk about DeFi today, they are not referring to open protocols where anyone can interact anonymously. In practice, institutions are building what is often called regulated DeFi.

Regulated DeFi uses blockchain networks for settlement and asset movement, but the surrounding infrastructure enforces the same controls that exist in traditional finance. Wallets are screened for AML and sanctions exposure, transactions are matched to internal records, and every settlement decision is tied to a compliance rule and an internal owner.

Technically, this means the blockchain handles transaction execution and finality, while an institutional integration layer manages compliance checks, reconciliation, and operational oversight before and after settlement.

In practice, integrating DeFi means adding a blockchain settlement layer that connects to existing financial systems.

DeFi Integration for Financial Institutions

DeFi integration does not mean buying cryptocurrency or launching a token.

It means extending your institution's operational boundary to include the blockchain layer. Every on-chain event that touches your assets needs an internal owner, a policy check, and a record. A payment that clears on-chain must match to an invoice. A wallet that sends funds must be screened before settlement. A release decision must log which rule triggered it and who owns it.

The institutions that get this right add a layer between their existing systems and the blockchain. That layer handles four jobs: settlement, compliance, reconciliation, and audit. Getting each one right is what this guide covers.

Step 1: Add a Stablecoin Settlement Rail

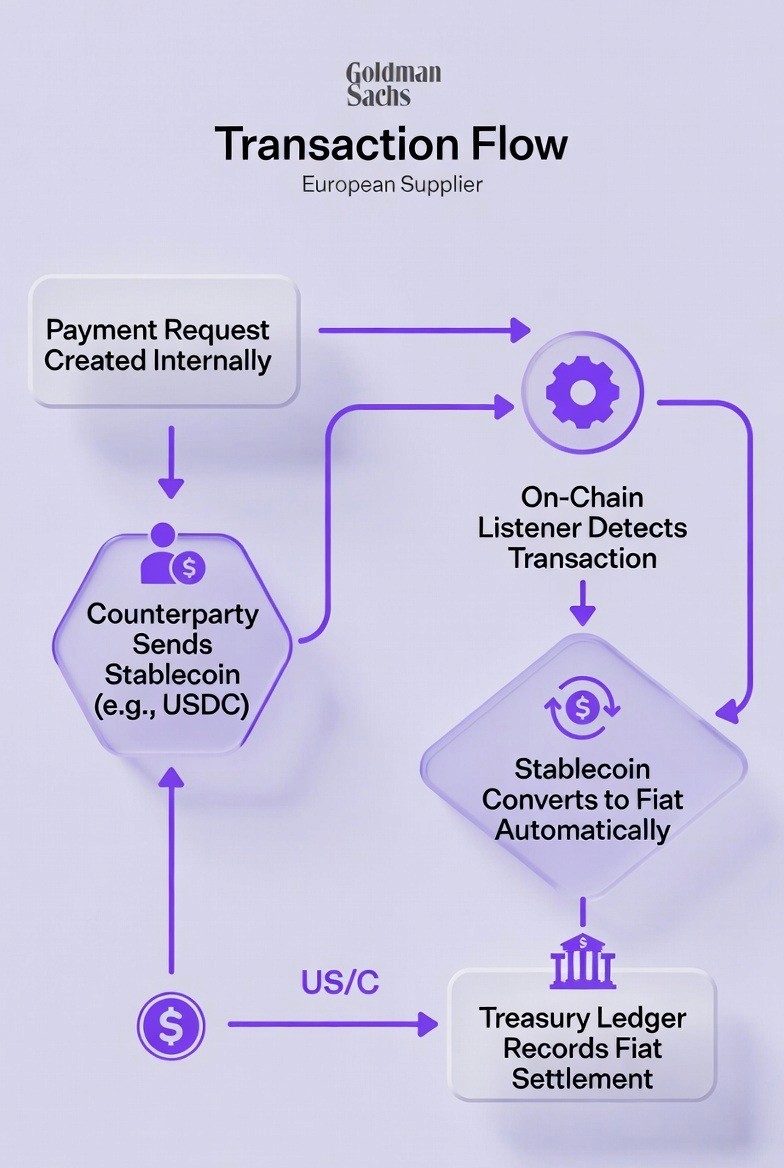

The first step is replacing or supplementing your correspondent banking rail with a stablecoin rail for cross-border payments.

A stablecoin is pegged to a fiat currency, usually the U.S. dollar. It moves on blockchain networks in minutes. It does not carry the volatility of other crypto assets. This is what makes it usable for institutional payments.

The integration works as follows. Your system generates a payment request. The counterparty sends USDC or another stablecoin to a wallet address. An on-chain listener detects the transfer and verifies confirmation. The stablecoin converts to fiat automatically at settlement. Your treasury ledger receives fiat. No crypto appears on the balance sheet.

What to confirm before going live:

Fiat conversion is automatic at settlement, not manual

The treasury ledger never holds a crypto asset, even briefly

Settlement confirmation is tied to on-chain finality, not to a third-party notification

Average cross-border settlement drops from two to five days to minutes. That is the speed gain. The operational requirement is that your team never has to touch the crypto asset to capture it.

Platforms like TMX Payments handle this layer via REST API and webhooks. It accepts stablecoin transfers from any Web3 wallet, converts to fiat at settlement, and syncs to your internal systems. Basic payment acceptance can go live in weeks without replacing existing infrastructure.

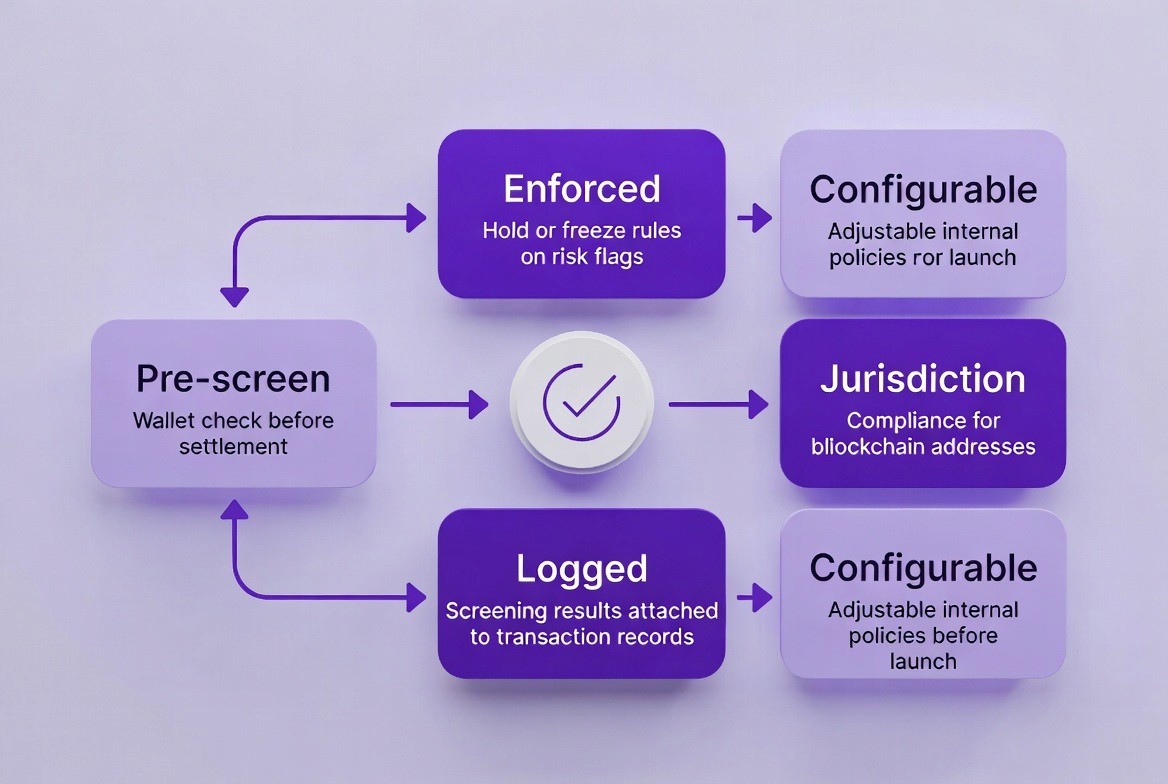

Step 2: Extend Compliance Jurisdiction to Wallets

This is the step most institutions skip. It is also the step that creates the most regulatory exposure.

Traditional AML and sanctions tools screen bank accounts, SWIFT codes, and legal entity identifiers. They do not screen blockchain wallet addresses. The moment your institution processes an on-chain payment without wallet screening, you are processing a transaction outside your compliance jurisdiction.

Extending compliance to wallets means three things.

First, screen the sending wallet before settlement releases. Not after. Screening after funds settle is reporting. Screening that blocks settlement is compliance. The difference matters under every major AML framework.

Second, log the result. The screen outcome, the list checked, the timestamp, and the compliance owner must all attach to the transaction record. This is what the DTCC framework calls role consistency.

Third, apply hold and freeze rules for policy triggers. Not every flagged wallet is on a sanctions list. Some match internal risk criteria. Your compliance layer needs rules that go beyond external screening lists.

What to confirm before going live:

Screening runs before settlement release, not after

Results are logged against the transaction record automatically

Internal policy rules are configurable, not hardcoded

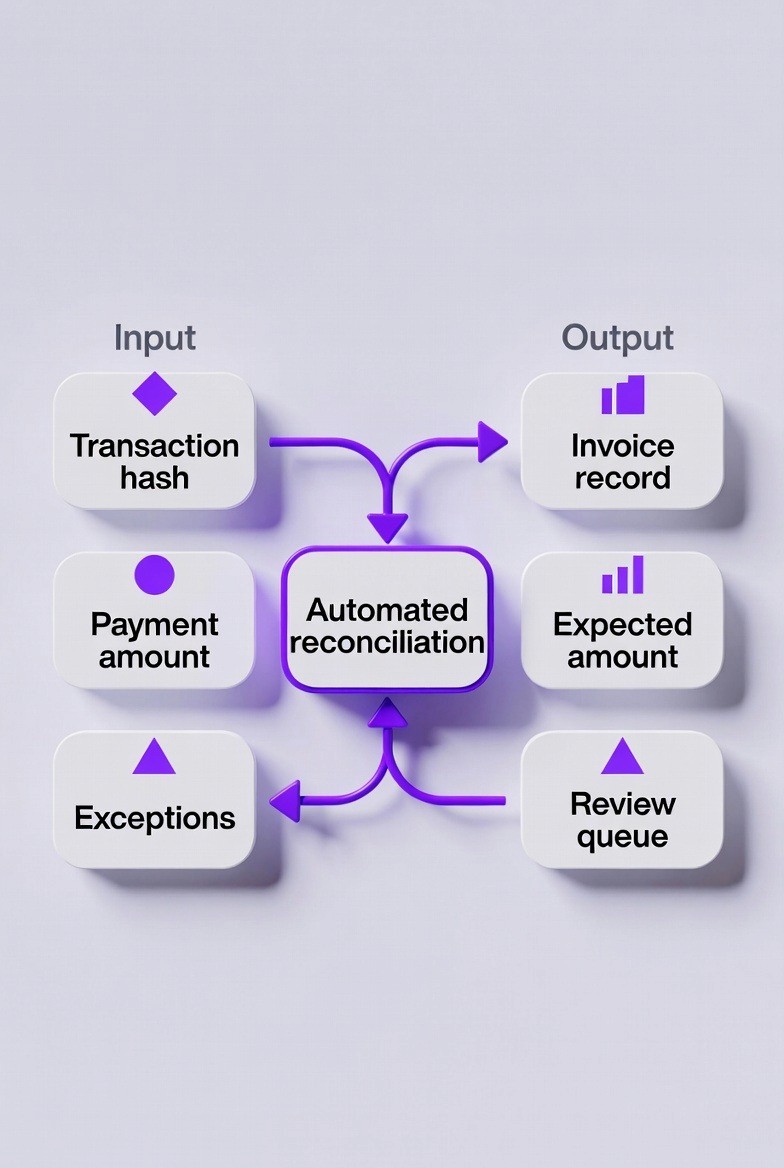

Step 3: Automate On-Chain Reconciliation

When a stablecoin payment arrives, it has a transaction hash, a block number, an amount, and a sending address. Your internal system has an invoice number, a purchase order reference, and an expected amount. Nothing connects them automatically unless you build that connection.

Manual matching works at low volumes. At scale it creates a backlog that grows faster than finance teams can clear it.

Automated reconciliation works by matching the on-chain transaction hash to the corresponding invoice record using amount, timing, and counterparty rules. Partial payments, overpayments, and duplicate entries are resolved by logic, not by a person. The output is a structured file that syncs to your internal ledger with a full audit trail.

What to confirm before going live:

Hash-to-invoice matching runs automatically for standard cases

Exceptions route to a named owner with a log entry

Output format maps to your internal ledger without manual reformatting

Institutions that automate reconciliation reduce manual matching time by 30 to 40 percent. That is not a technology improvement. It is a headcount and error-rate improvement.

TMX Payments does this matching automatically. It links transaction hashes to invoices using amount, timing, and counterparty rules. Partial payments, overages, and duplicates resolve by rule logic. The output syncs to internal ledgers with full audit logs.

Step 4: Assign Internal Ownership to Every Settlement Step

This is the DTCC framework's role consistency requirement in operational terms. Every step in the settlement chain needs a named internal owner. That owner is accountable for the decision at that step. The decision is logged with a timestamp, a rule ID, and the owner.

Without this, your institution cannot answer the question a regulator or auditor will eventually ask: who approved this payment, at which step, under which policy rule?

In practice, this means your integration layer must log six things for every transaction: the payment request creator, the wallet screen result and owner, the invoice match result, the rule that triggered payout release, the fiat conversion record, and the export timestamp.

What to confirm before going live:

Every settlement step has a logged owner and rule reference

Logs are exportable in a structured format for audit and compliance teams

The log chain is complete from payment request to fiat receipt

TMX Payments is built to support the whole operational layer. It is a crypto payment platform built by TokenMinds for institutions that need to operate on blockchain rails without rebuilding their existing infrastructure. It connects to existing systems via API, handles each of the four jobs, and does not require a full infrastructure replacement to go live.

When Institutions Move from Pilot to Production

Across TokenMinds institutional case studies, financial institutions moved from sandbox pilots to live production rails only after three conditions were met.

First, custody clarity. Every step of the transaction had a named internal owner. Ambiguous custody blocked sign-off from legal and risk teams every time.

Second, wallet screening is integrated into the settlement gate. Compliance would not approve production use until screening blocked settlement, not just flagged it.

Third, fiat settlement was guaranteed before the asset touched the treasury ledger. The Treasury teams require a documented conversion mechanism.

Institutions with all three in place moved to production. Institutions missing one stalled. The gap was never the blockchain. It was the operational layer around it.

The DeFi Integration Readiness Index

This index scores your readiness across the four integration steps. Each area is scored 1 to 4. Total is out of 16.

Step | 1: Not Started | 2: Basic | 3: In Progress | 4: Fully Ready |

Stablecoin Settlement Rail | No crypto rail. Correspondent banks only. | Crypto rail tested in sandbox. Not live. | Live for some corridors. Fiat conversion manual. | Stablecoin rail live. Auto fiat conversion at settlement. No crypto on ledger. |

Wallet Compliance Coverage | No wallet screening. | Screening active but applied after settlement. | Screening gates settlement. Results not logged. | Screening gates settlement. Results logged with owner, rule, and timestamp. |

Reconciliation Automation | 100% manual. Every hash matched by hand. | Some automation. High exception backlog. | Automated for most payments. Exceptions manual. | Full hash-to-invoice matching. Structured output. Clean audit trail. |

Role Accountability | No internal owner assigned to on-chain steps. | Ownership informal. Not logged. | Ownership assigned. Logs incomplete. | Every step logged with rule ID, timestamp, and named owner. |

Score guide:

4 to 6: You have a liability gap. On-chain activity is outside your operational boundary.

7 to 10: Partial coverage. Compliance or reconciliation gaps will surface under regulatory review.

11 to 13: Well-placed. Remaining gaps are optimization, not structural risk.

14 to 16: Fully ready. Your setup meets the role consistency standard the DTCC framework requires.

Where most institutions start:

Step | Score | Why |

Stablecoin Settlement Rail | 1 | No crypto rail in production. Correspondent banks only. |

Wallet Compliance Coverage | 1 | Wallet addresses outside screening scope. |

Reconciliation Automation | 2 | Fiat invoices tracked. On-chain payments matched manually. |

Role Accountability | 1 | No internal owner logged for on-chain settlement steps. |

Total | 5/16 | On-chain activity is a liability gap, not a payment channel. |

The Real-world Examples in Practice

1. A cross-border B2B payment platform

A platform settles supplier payments through correspondent banks. Settlement takes three days. On-chain events are not tracked. After integrating TMX Payments across all four steps, USDC transfers settle in minutes. Each transfer maps to an invoice automatically. The compliance team has a wallet screening log for every transaction. Failed settlements drop 20 to 30 percent. Reconciliation time drops 30 to 40 percent.

2. Adding a crypto rail

A commercial bank wants to offer crypto payment acceptance to enterprise clients without balance sheet exposure. TMX Payments provides stablecoin acceptance and immediate fiat conversion under the bank's brand. Wallet screening runs before any funds move. Every step logs against a policy rule the bank controls.

3. Enterprise treasury team

A multinational with payables across twelve currencies wants to cut FX hedging costs and intermediary fees. TMX Payments routes payables through stablecoin rails, converts at settlement, and syncs to the treasury system. The ledger sees only fiat. The operations team has a full audit trail for every on-chain event.

Conclusion

Integrating DeFi into traditional finance is an operational process. It is not a technology experiment. It requires four things: a stablecoin settlement rail, wallet compliance coverage, automated reconciliation, and clear internal ownership for every settlement decision. These four capabilities extend an institution's operational boundary to include blockchain settlement. The controls required in regulated financial systems stay intact.

The DTCC framework formalizes this. It demands accountability across asset movement, compliance, and participant roles. Institutions that build these operational capabilities early will be better positioned when blockchain settlement infrastructure matures.

FAQ

What does DeFi integration mean for financial institutions

It means using blockchain networks to settle payments while keeping the same compliance checks, records, and approvals used in traditional finance. The blockchain handles settlement, while the institution still controls compliance and accounting.

Why are banks interested in blockchain settlement

Blockchain can settle cross border payments in minutes instead of days. It also provides a clear record of each transaction on the network.

How do institutions manage compliance with blockchain payments

Institutions screen wallet addresses for AML and sanctions risks before releasing a payment. The screening result is logged so each transaction has a clear compliance record.

What systems are needed to use blockchain settlement

Most institutions need four capabilities. A stablecoin payment rail, wallet screening, automatic reconciliation with internal records, and clear ownership for each settlement step.

How does the DTCC framework relate to DeFi integration

The DTCC framework explains how digital assets should move across financial systems with clear accountability. It focuses on asset ownership, compliance, data standards, and clear roles for participants.

What is TMX Payments

TMX Payments is a platform built by TokenMinds that helps institutions connect their existing systems to blockchain payment rails. It supports stablecoin payments, wallet screening, reconciliation, and audit logs.