Key takeaways:

Crossmint's partnership with Western Union to launch USDPT on Solana connects on-chain dollar transfers to 360,000 cash collection points across 200 countries, confirming that stablecoin remittance infrastructure has moved from pilot to global payment rail.

Stablecoin remittance platforms typically require four operational systems to run compliantly at scale: stablecoin acceptance with proven reserves and confirmed legal status per market, wallet-level AML and sanctions screening before every transfer, automated hash-to-record reconciliation, and programmable settlement control with configurable confirmation rules per chain.

On March 4, 2026, Crossmint announced a partnership with Western Union to support USDPT. USDPT is a new U.S. dollar stablecoin issued on Solana. Western Union's Digital Asset Network links that stablecoin to real-world cash access. Users can convert digital dollars into local currency through more than 360,000 collection points in over 200 countries, a structure explored on blockchain-based payment infrastructure.

This is not a blockchain experiment. Western Union moves billions of dollars a year in cross-border payments. When a company that size builds a stablecoin and connects it to its global cash network, the direction of the industry is clear.

Stablecoins are becoming the standard rail for moving value across borders. The question is no longer whether this will happen. The question is how to build the infrastructure to do it correctly.

Traditional Remittances Core Problems

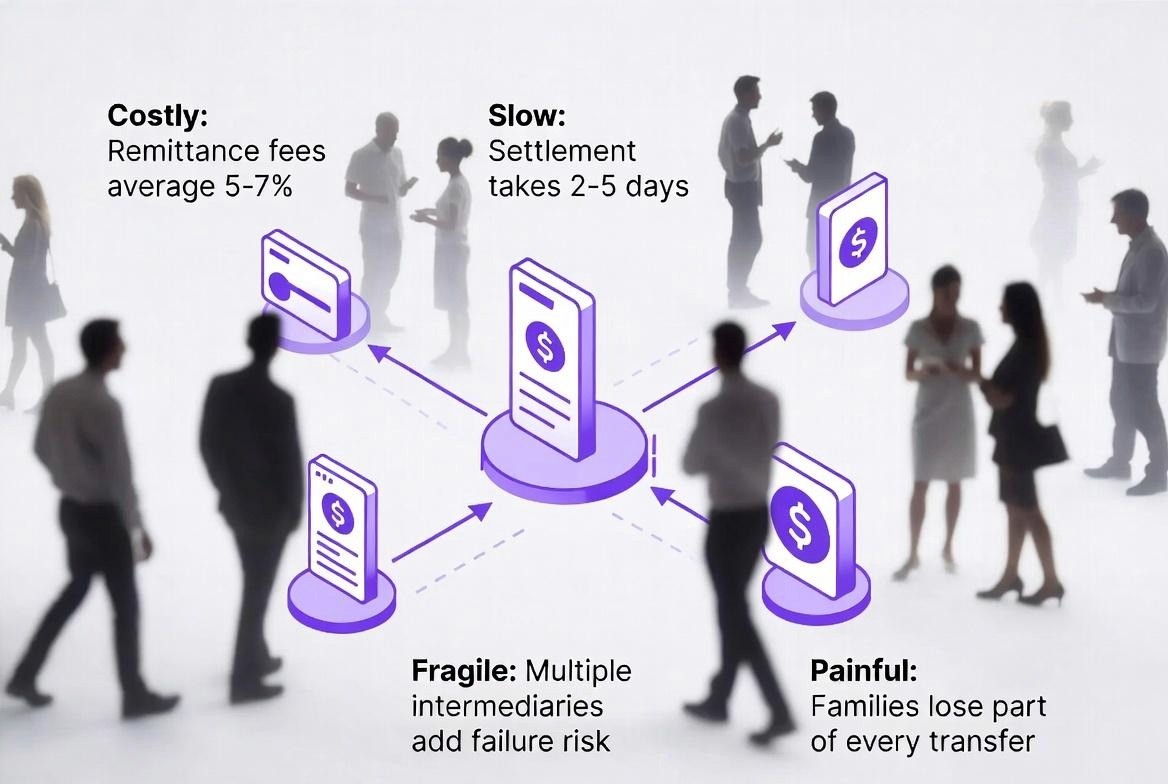

A worker in Singapore sends money to a family in the Philippines. The transfer moves through a local bank, a correspondent bank, a clearing network, and a receiving bank. Each step adds time. Each step adds cost. Each step is a point where the transfer can fail, delay, or shrink.

The average global remittance fee is between 5% and 7% of the amount sent. For every $200 sent, between $10 and $14 disappears in fees, a friction that newer blockchain settlement models attempt to remove. For families that rely on remittances as income, that gap is money that never arrives.

Settlement takes between 2 and 5 business days in most corridors. The recipient cannot plan around that delay. If the money is needed for rent, food, or school fees, the timing gap creates real hardship.

The problem is structural. Correspondent banking routes were built for large institutional payments. They were never designed for small, frequent, cross-border transfers between individuals. Stablecoins were.

What Stablecoins Actually Change for Remittances

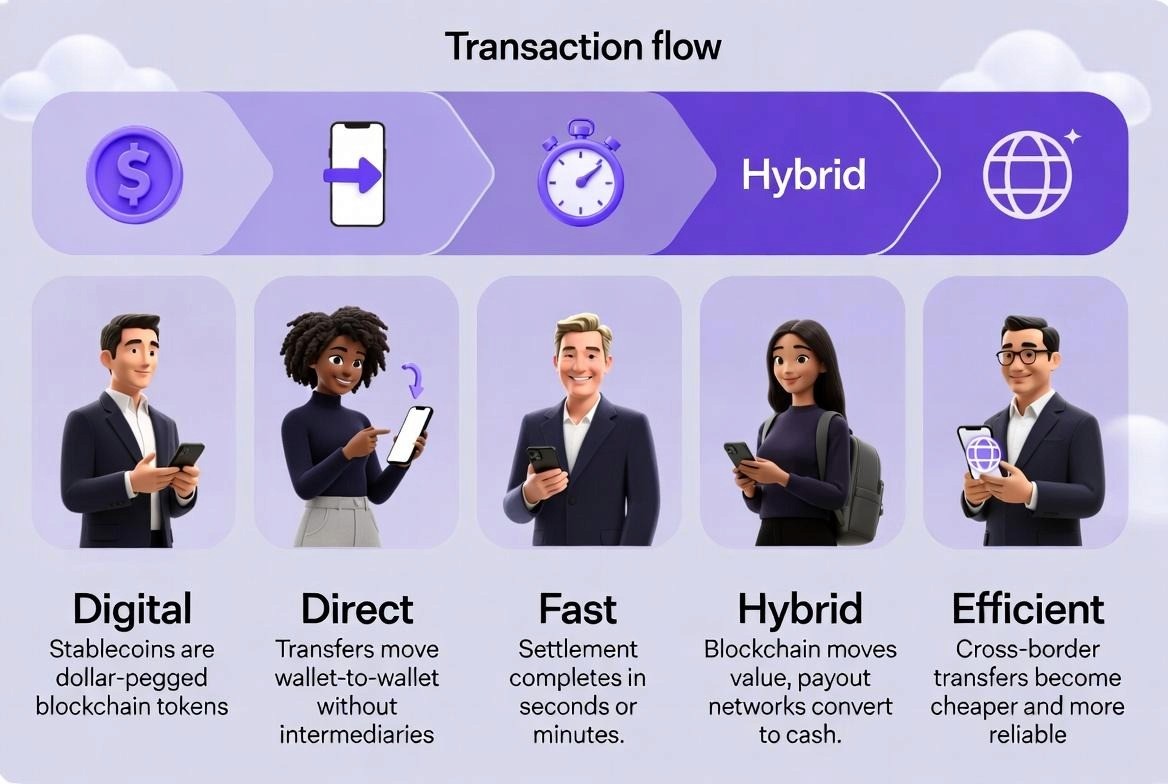

A stablecoin is a digital token pegged to a fixed asset, usually the U.S. dollar. It lives on a blockchain. It moves like a cryptocurrency. Fast, borderless, and without a correspondent bank in the middle.

When a sender uses a stablecoin for a cross-border transfer, the value reaches the recipient's wallet in seconds or minutes. The fee is a fraction of a percent. The transfer skips three intermediaries. It moves directly from wallet to wallet on-chain.

That is the model Western Union is building with USDPT. The stablecoin moves on Solana. Once it arrives, Western Union's cash network converts it into local currency at a nearby collection point. The sender uses blockchain rails. The recipient gets local cash. Both sides get a faster, cheaper, and more reliable transfer.

This model works because it splits the problem in two. The first part is moving value across borders without banks. The second part is converting that value into something the recipient can use. Stablecoins solve the first part. A payout network solves the second.

How Stablecoin Remittances Work in Practice

A mid-sized remittance company in Singapore wants to offer stablecoin transfers to workers sending money to Indonesia, the Philippines, and Vietnam. It accepts USD-backed stablecoins for retail corridors because of low transaction costs. It uses the same rails for larger institutional settlements with partner banks.

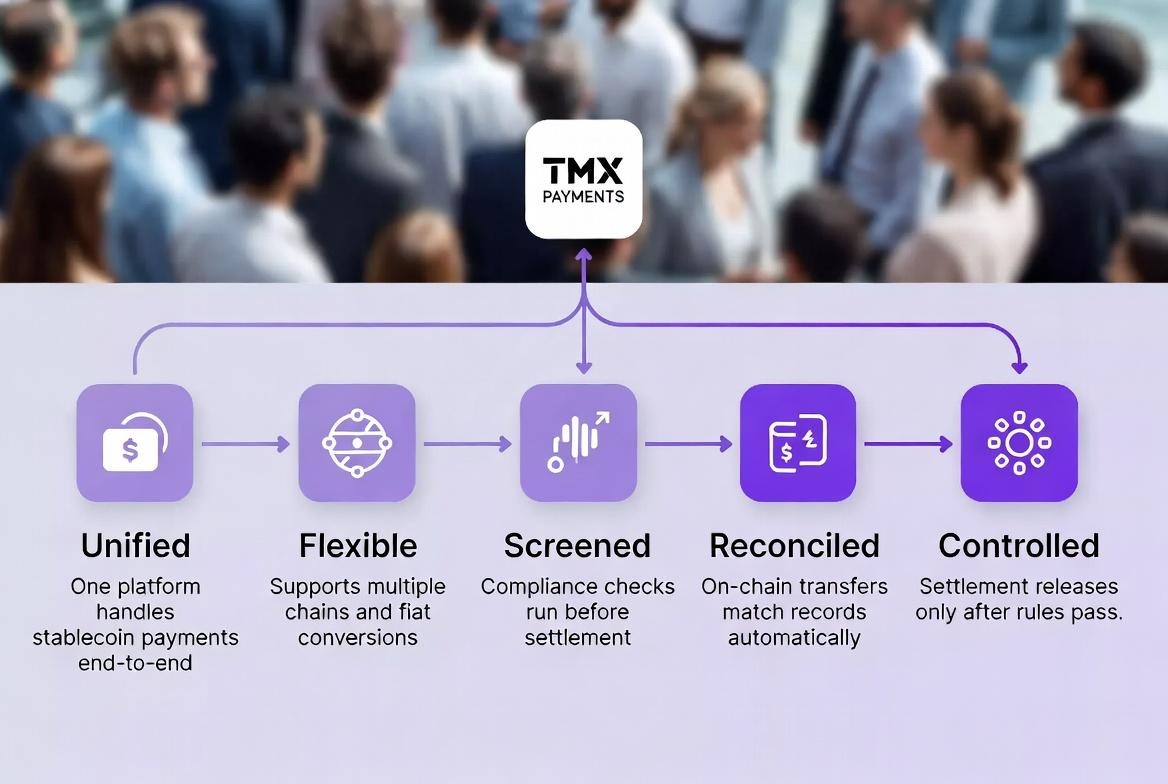

The company builds its platform on TMX Payments by TokenMinds. TMX Payments handles stablecoin acceptance, wallet screening, reconciliation, and settlement logic across all corridors from a single platform. The company does not build a separate compliance layer for each corridor. It configures rules once and they apply across all markets.

Here is how a single transfer flows through the system.

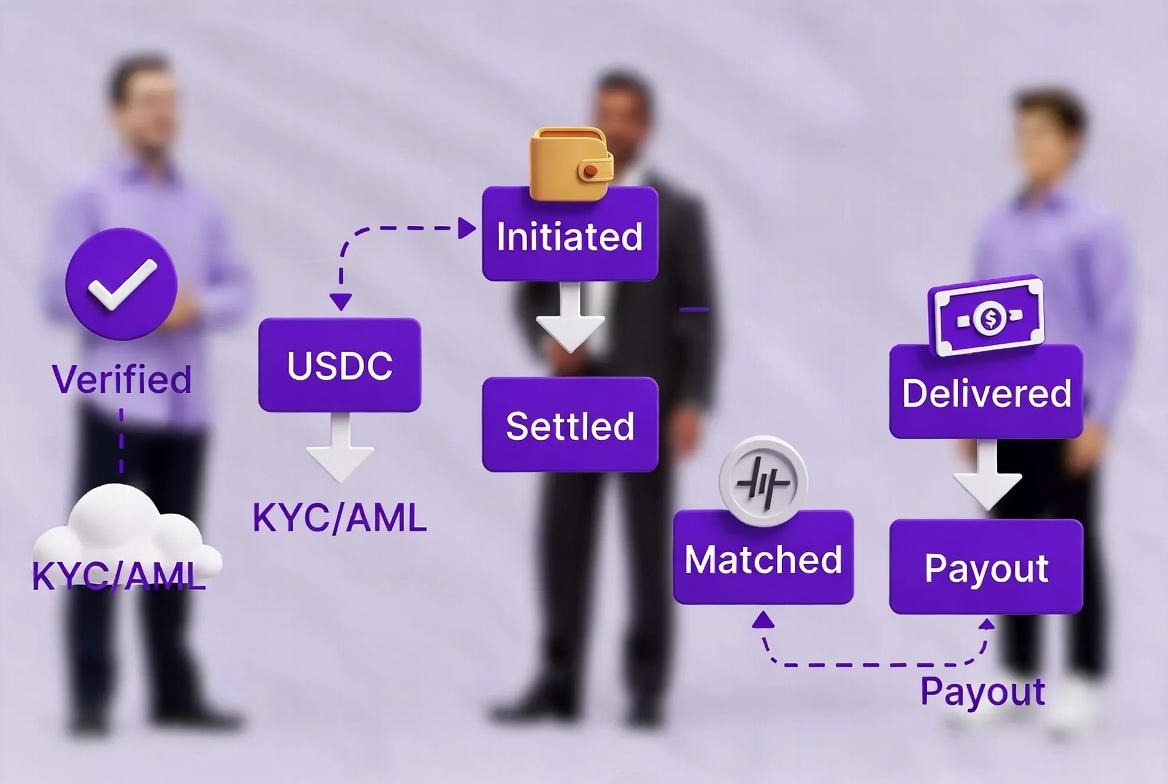

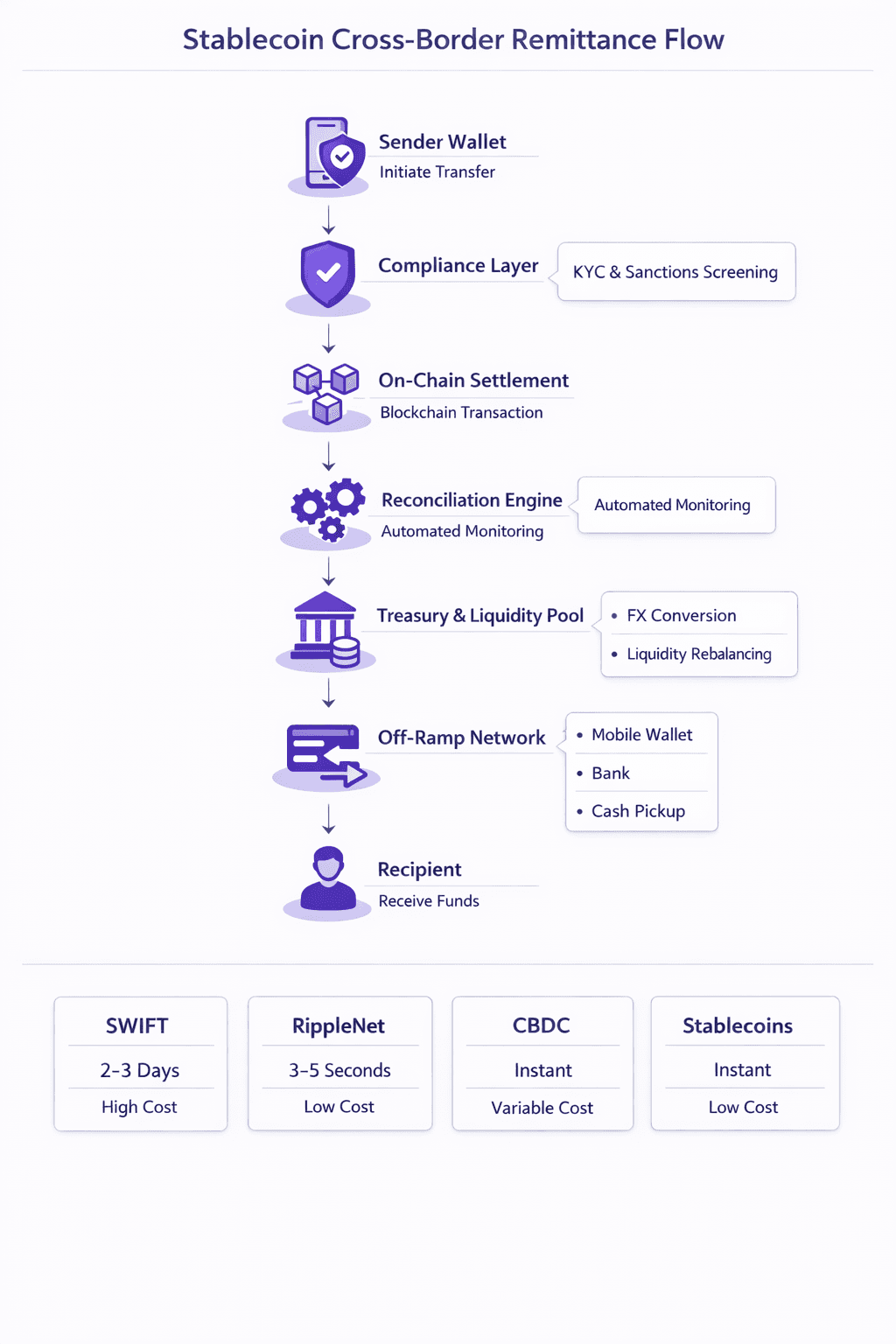

Step 1: The sender starts the transfer

A worker in Singapore opens the remittance app and sends $300. The platform checks the sender's wallet before the transfer goes through. KYC confirms the sender's identity. AML confirms the wallet is not on any sanctions list. The compliance gate passes. The transfer is released.

Step 2: The stablecoin moves on-chain

The $300 converts into 300 USDC. It moves from the sender's wallet to the company's settlement wallet on-chain. The transaction records a hash, a block number, an amount, and a timestamp. Settlement is atomic. The transfer completes fully or not at all. There is no partial arrival and no counterparty exposure during the transfer.

Step 3: The platform matches the transfer to the internal record

The reconciliation engine picks up the transaction hash. It matches it to the pending transfer record by amount, sender address, and reference code. No one does this by hand. The match happens in seconds. The internal record updates to show the transfer as settled. The finance team has a full audit trail without assembling it manually.

Step 4: The recipient gets local currency

The platform converts the stablecoin to Indonesian rupiah, Philippine pesos, or Vietnamese dong via TMX Payments' auto-fiat settlement engine. It pushes the funds to the recipient's mobile wallet, bank account, or nearest cash pickup point. The recipient collects the money. The transfer is complete.

The same transfer that would have taken 3 business days and cost $18 through traditional rails took under 10 minutes and cost less than $1.

The Four Systems Every Stablecoin Remittance Platform Needs

The stablecoin is not the hard part. Solana, Stellar, and Ethereum all settle in seconds. The blockchain works.

The hard part is the four systems that sit between the stablecoin and the real-world financial system. Without these, a stablecoin remittance platform is not compliant, not scalable, and not safe to operate.

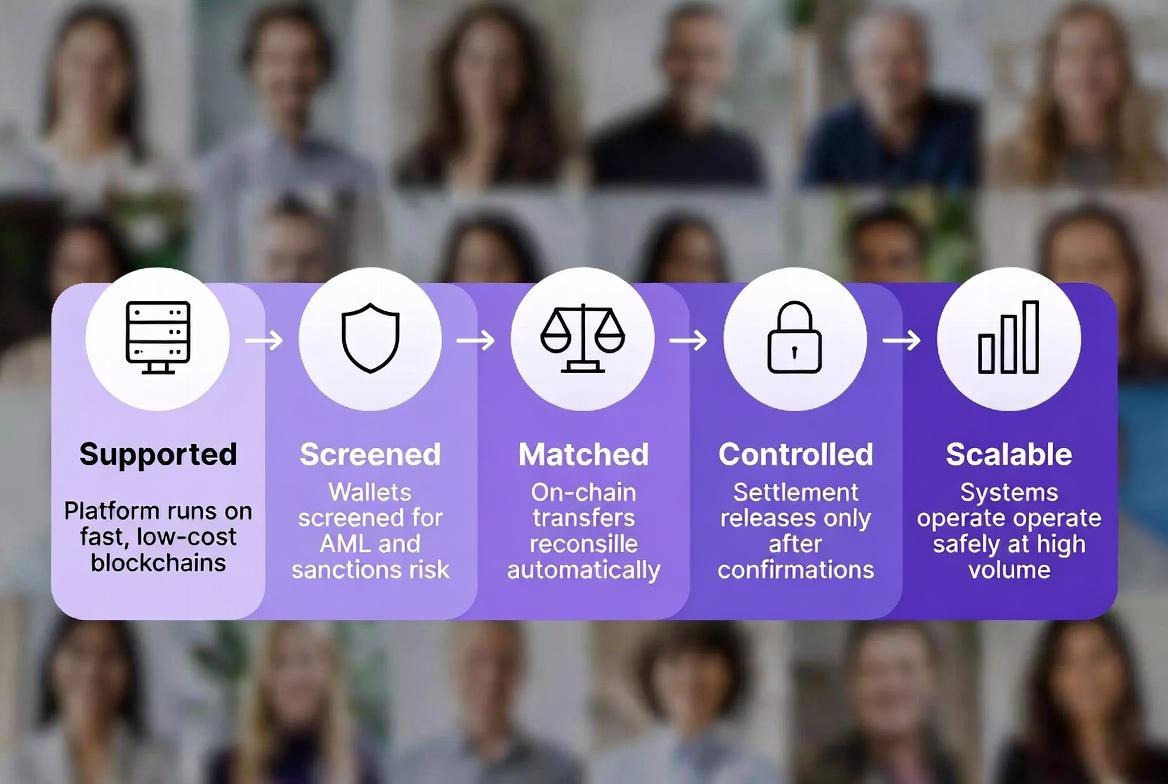

1. Stablecoin Acceptance on a Supported Blockchain

A stablecoin payment platform used for remittances must support fast, low-cost settlement chains. Stellar and Algorand suit high-volume retail corridors. Ethereum and BNB Chain are common for institutional-scale transfers where compliance depth matters more than transaction cost.

The stablecoin must be backed one-to-one by the reference asset. If it is pegged to the U.S. dollar, one dollar must sit in reserve for every token in supply. The platform must prove this at any time. Regulators in most markets now require proof of reserves for any stablecoin used in payment services.

The token must also carry the correct legal status in each country it operates in. What counts as a stablecoin under Singapore's Payment Services Act differs from what counts as electronic money under the EU's MiCA regulation. The payment layer must satisfy both.

TMX Payments accepts stablecoins including USDC and USDT and supports auto-conversion to fiat on settlement. It connects to both fiat and crypto rails from a single integration. A business running multiple corridors does not rebuild its payment stack per market.

2. Wallet Compliance Screening

Every wallet that sends or receives stablecoins must pass screening before settlement releases. Remittances are one of the highest-risk categories for money laundering and sanctions evasion. Screening must happen before the transfer, not after.

Traditional AML tools screen bank accounts and SWIFT codes. They do not screen blockchain wallet addresses. When a platform processes an on-chain transfer without wallet screening, it operates outside its compliance boundary. Even if the legacy AML tool shows green, the on-chain transfer is unscreened.

Screening must gate settlement. The result must log with a timestamp, the rule that triggered the check, and the compliance owner. That log is the evidence file when a regulator asks why a transfer was cleared.

TMX Payments screens every wallet against sanctions lists before any transfer releases. The check runs automatically before each leg of the payment. The result logs to the transfer record without manual input. The audit trail is complete from the first transfer.

3. Automated Reconciliation

Every on-chain transfer must match to an internal record without manual work. At 50 transfers a day, manual matching is slow but possible. At 5,000 transfers a day, the backlog never clears.

When a stablecoin arrives in the settlement wallet, it carries a transaction hash, a block number, an amount, and a sender address. The internal system has a transfer reference, a sender ID, and an expected amount. Nothing connects them unless the reconciliation layer is built.

The system must match hash to record automatically. It must handle partial arrivals, overpayments, and duplicate submissions without creating exceptions that need human review. The output must sync to existing treasury and accounting systems without reformatting.

TMX Payments runs this reconciliation layer automatically. When a stablecoin lands on-chain, the hash matches to the internal invoice or transfer record within seconds. The reconciliation engine handles partials, overpayments, and idempotent processing without manual exceptions. The output syncs to internal ledgers in a format that maps to existing ERP and treasury systems.

4. Settlement Control Logic

Fast blockchains like Solana settle in under a second. That speed creates a risk. A transfer confirmed on the first block is technically reversible if the blockchain reorganizes. A system that releases funds on the first confirmation is exposed to that risk.

Confirmation rules must define how many blocks must pass before settlement is final. For Solana, this takes seconds. For Ethereum, it takes longer. The platform must set these rules per chain and enforce them automatically. Settlement must not be released until the confirmation threshold and the compliance gate both pass.

TMX Payments enforces confirmation rules and compliance gates together through its programmable settlement engine. Confirmation rules, hold logic, and escrow conditions are all configurable. Transfers complete fully or not at all. Partial settlement is removed at the infrastructure level. Finance teams do not chase incomplete transfers or create manual exceptions.

What the Western Union Model Proves

The Western Union and Crossmint deal makes one thing clear. A stablecoin without a real-world off-ramp is only half a solution. USDPT on Solana moves value across borders in seconds. Western Union's 360,000 collection points convert it to local cash. The combination closes the loop.

Any remittance platform that wants to compete needs the same two-part structure. The on-chain layer must move value fast, cheaply, and with full compliance screening. The off-ramp layer must convert that value into something the recipient can actually use.

The platforms that win will not be the ones with the fastest blockchain. They will be the ones with the most complete operational layer around that blockchain. Compliance, reconciliation, settlement, and real-world conversion are not add-ons. They are the product.

The Stablecoin Remittance Readiness Index

Most businesses entering this space do not know where their operational gaps are. This index scores readiness across four areas. Each area scores 1 to 4. Score of 1 means nothing is in place. Score of 4 means fully ready. Total out of 16.

Area | 1 - Not Started | 2 - Basic | 3 - In Progress | 4 - Fully Ready |

Stablecoin Acceptance | No stablecoin infrastructure. No blockchain setup. | Sandbox tests done. No reserve proof or legal opinion. | Live on one chain. Reserve proof in progress. Legal status under review. | Live on supported chains. One-to-one reserve proven. Legal status confirmed per market. |

Wallet Compliance | No wallet screening. Legacy AML only. | Screening exists but runs after settlement. | Screening gates settlement. Results not logged automatically. | Screening gates every transfer. Results logged with rule, timestamp, and compliance owner. |

Reconciliation | Every transfer matched by hand. No automation. | Some automation. High exception backlog. | Auto-matching for standard transfers. Exceptions still manual. | Full hash-to-record matching. Output syncs to ledger without reformatting. |

Settlement Control | Transfers release on first block. No rules. | Basic block count. No compliance gate. | Rules in place. Compliance screening runs apart from settlement. | Atomic settlement. Confirmation rules and compliance gate both required before funds release. |

Score guide:

4 to 6: You cannot run a compliant stablecoin remittance platform yet. Every transfer is a liability gap.

7 to 10: Partial coverage. Compliance or reconciliation gaps will show up under regulatory review or at volume.

11 to 13: Well-placed. Remaining gaps are optimization, not structural risk.

14 to 16: Fully ready. Your operational layer meets what regulators and partners expect.

Where most businesses start:

Area | Score | Why |

Stablecoin Acceptance | 1 | No stablecoin payment setup in production. Reserve proof and legal status not confirmed. |

Wallet Compliance | 1 | Wallet addresses sit outside existing AML screening entirely. |

Reconciliation | 2 | Transfer records tracked internally. On-chain transactions still matched by hand. |

Settlement Control | 1 | No confirmation rules. Transfers release on first block. |

Total | 5/16 | Not ready to scale or pass regulatory review without infrastructure changes. |

The gap between 5 and 16 is not a blockchain gap. Solana settles in under a second. Stellar handles millions of transactions a day. The blockchain is not the problem. The operational layer around it is.

Traditional Remittance vs Stablecoin Infrastructure

Factor | Traditional Correspondent Banking | Stablecoin Remittance Platform |

Settlement time | 2 to 5 business days | Under 10 minutes |

Average fee | 5% to 7% of transfer value | Under 1% |

Intermediaries | 2 to 4 correspondent banks | None |

Compliance layer | Manual AML review, SWIFT screening | Automated wallet screening, on-chain record |

Reconciliation | Manual matching across multiple statements | Automated hash-to-record matching |

Off-ramp options | Bank account only | Mobile wallet, bank account, cash pickup |

Audit trail | Multi-party documents, slow to retrieve | Single on-chain record, exportable on demand |

Scalability | Limited by correspondent bank capacity | Scales with blockchain throughput |

Platforms like TMX Payments automate these functions so remittance providers can operate stablecoin corridors without building separate infrastructure for compliance, reconciliation, and settlement.

How TMX Payments Supports the Full Stack

TMX Payments by TokenMinds provides the full operational layer for stablecoin remittance platforms. It covers stablecoin acceptance, auto-fiat settlement, compliance, reconciliation, and payment control in one platform. Businesses do not piece together separate tools for each function.

Stablecoin acceptance runs across major chains and currencies including USDC and USDT. Incoming stablecoins convert automatically to fiat at settlement. The dual-rail architecture handles both fiat and crypto from a single integration. KYC, AML rules, hold logic, and country restrictions are configured once and apply across all corridors.

Wallet screening gates every transfer. The check runs before settlement releases and before each leg of the payment. It logs the result with a timestamp and compliance owner on every transfer. The audit trail is built into the process, not assembled after the fact.

Reconciliation runs without manual input. Every hash matches to an internal invoice or transfer record within seconds of landing on-chain. Partial arrivals, overpayments, and duplicate submissions are handled automatically through idempotent processing. The output syncs to existing ledgers in a format that maps to ERP and treasury systems. Finance teams do not reformat files or chase exceptions.

Settlement holds until confirmation rules and compliance checks both pass. The programmable settlement engine supports configurable confirmation rules, hold conditions, and escrow logic per corridor. Transfers complete fully or not at all. The platform handles the finality window per chain automatically.

The merchant dashboard gives real-time visibility into payment status, refunds, disputes, and compliance flags. Everything is exportable with one click for audit or reporting. The agentic AI layer handles payment routing and recommendation across corridors, reducing failed transfers and optimizing settlement paths.

Real Corridor Data: What Stablecoin Remittances Actually Deliver

Regulatory Architecture for Stablecoin Remittance Platforms

A stablecoin remittance platform operating across multiple markets does not face one regulatory framework. It faces several simultaneously, and each one has a different requirement for the same underlying activity.

Licensing by market. A platform operating across Singapore, the EU, and the Philippines typically requires a Major Payment Institution license under Singapore's Payment Services Act, an Electronic Money Institution license in the EU under MiCA, and local remittance operator licensing in each destination market it serves. Some corridors require licensing in both the send and receive country. A platform that goes live without confirming its licensing position in each market is operating with unquantified regulatory exposure from day one.

Stablecoin issuer requirements. MiCA requires stablecoin issuers serving EU users to hold one-to-one reserves, publish monthly reserve disclosures, and maintain custody arrangements with regulated institutions. Singapore's MAS requires similar reserve backing and imposes redemption rights for holders. Platforms that accept third-party stablecoins rather than issuing their own must confirm that those stablecoins meet the reserve and disclosure requirements of every market they operate in.

Travel Rule enforcement. The Financial Action Task Force Travel Rule requires platforms to collect and transmit originator and beneficiary information on transfers above threshold amounts, typically $1,000 or the local equivalent. On-chain, this means the compliance layer must attach identity data to the transaction record before settlement releases and share it with the receiving platform automatically. Platforms without Travel Rule tooling built into their settlement flow are non-compliant in every FATF member jurisdiction.

Reserve audits and custody. Regulators in Singapore, the EU, and increasingly in Southeast Asian markets require proof of reserves on demand. That means the platform must be able to demonstrate at any point that stablecoin liabilities are fully backed by segregated, auditable reserves held with regulated custodians. Annual attestations are the minimum. Monthly third-party audits are becoming the standard in licensed markets.

TMX Payments is built to support Travel Rule compliance, reserve documentation, and multi-jurisdiction licensing workflows from a single platform configuration rather than requiring separate compliance builds per corridor.

Conclusion

The Western Union and Crossmint deal did not create the stablecoin remittance category. It confirmed that the category has arrived. One of the largest payment networks on earth built a stablecoin, put it on Solana, and connected it to 360,000 cash collection points across more than 200 countries. That is not an experiment. That is infrastructure.

The businesses that compete in this space will be the ones that build the operational layer now. The stablecoin is the easy part. The compliance, reconciliation, settlement, and off-ramp infrastructure around it is what separates a working platform from a liability.

Most platforms start at 5 out of 16 on the Readiness Index. The gap between 5 and 16 is an operational gap, not a technology gap. The tools to close it exist today. The businesses that close it first will define what cross-border remittances look like for the next decade.

FAQ

What is a stablecoin?

A stablecoin is a digital token pegged to a fixed asset, most often the U.S. dollar. It holds a stable price and can be sent across borders using blockchain technology without a bank in the middle.

How do stablecoins work for remittances?

A sender converts local currency into a stablecoin. It moves on-chain to the recipient's wallet in minutes at low cost. The recipient converts it into local currency through a cash pickup point, mobile wallet, or bank account.

Are stablecoin remittances regulated?

Regulation varies by country. Most markets now require one-to-one reserves, proof of reserves on demand, and wallet screening for AML and sanctions. Platforms operating in multiple countries must confirm the legal status of their stablecoin in each market they serve.

What blockchain is best for stablecoin remittances?

Stellar and Solana suit retail remittance corridors because of low costs and fast finality. Ethereum and BNB Chain suit institutional-scale transfers. The right choice depends on the corridor, the volume, and the compliance rules of each market.

What is TMX Payments?

TMX Payments is a stablecoin payment platform built by TokenMinds. It accepts stablecoins and settles automatically to fiat, screens wallets against sanctions lists before every transfer, reconciles on-chain transactions to internal records without manual work, and controls settlement through a programmable engine with configurable confirmation rules and hold logic. It runs on both fiat and crypto rails from a single integration.