TL;DR

This guide helps banks decide whether receivables or inventory tokenization is the stronger first collateral pilot. It compares both options across seven dimensions and applies a weighted scoring model for 90-day pilot selection. It adds corridor recommendations, bank-readiness profiles, failure-mode controls, and a 12-week execution roadmap.

Default Recommendation

Most commercial banks should start with receivables if invoice data and legal assignment workflows already exist, unless the bank already operates commodity finance workflows. Inventory should come first for commodity-focused lenders with certified warehouse partners, inspection workflows, and enforceable warehouse receipt controls.

Why Sequencing Determines Pilot Outcomes

Starting with the wrong use case wastes a pilot cycle. A program that stalls on legal gaps produces skepticism, not evidence.

The BIS documents real-world receivables tokenization examples, including Credix and AmFi. Both models use tokenized receivables as collateral to support credit access. This makes receivables a clearer first pilot candidate when banks need existing examples to benchmark. Inventory-backed programs have parallel momentum through warehouse receipt law reform. Both are viable. The question is which one your bank can execute in 90 days.

Inventory Legal Foundation

Inventory tokenization has separate legal momentum. The UNCITRAL–UNIDROIT Model Law on Warehouse Receipts (2024) supports modern warehouse receipt systems, including electronic and paper-based receipts. This strengthens the legal foundation for inventory-backed collateral pilots, especially in commodity corridors with licensed warehouses.

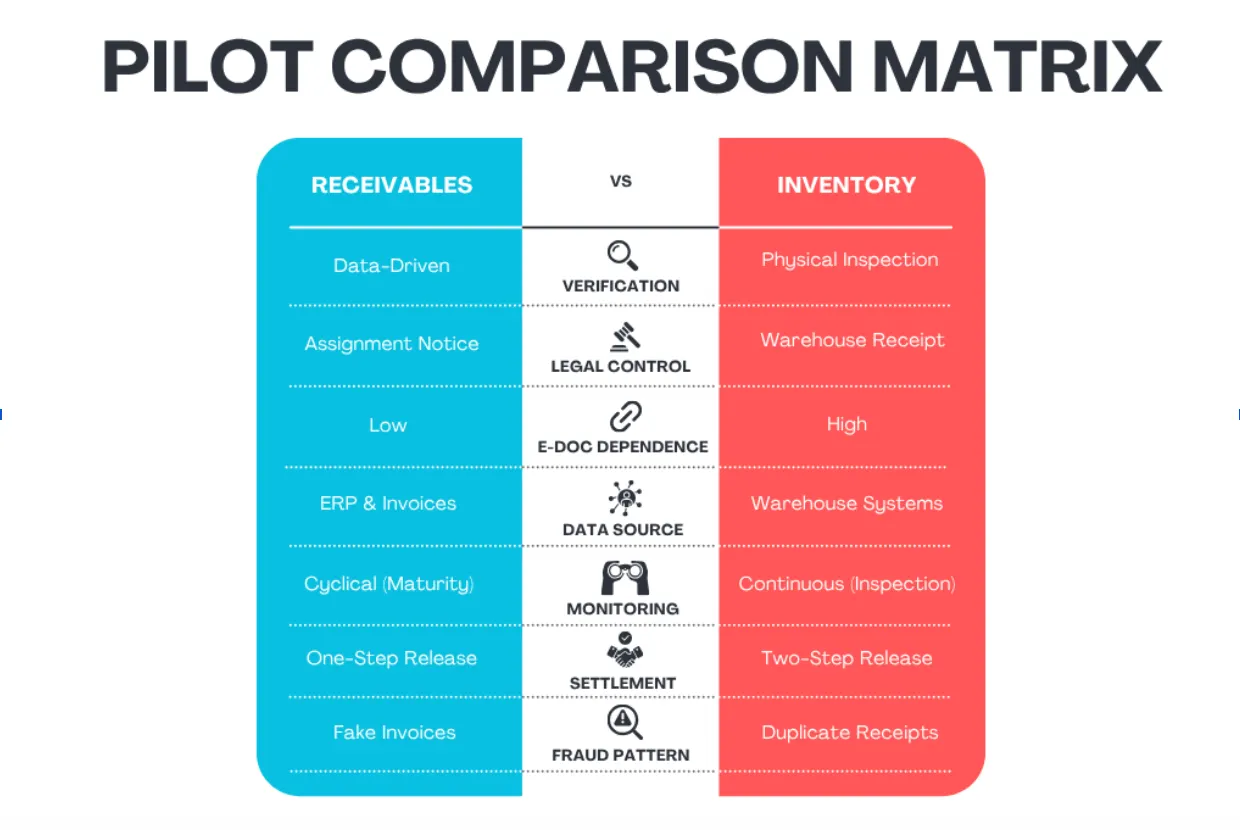

Seven-Dimension Comparison

Dimension | Receivables | Inventory |

Verification method | Data-driven, automatable | Physical inspection, not fully automatable |

Legal control instrument | Assignment notice plus perfection filing | Warehouse receipt plus warehouse agreement |

Electronic document recognition | Low dependence | High dependence |

Data source | ERP, invoice network | Warehouse system, price feed |

Monitoring cycle | Per invoice maturity, 30 to 90 days | Continuous, inspection every 30 to 90 days |

Settlement steps | One: cash received, pledge released | Two: cash received and physical release authorized |

Fraud pattern | Fake invoice, duplicate pledge | Duplicate receipt, quantity misrepresentation |

Weighted Pilot Scoring Model

Equal-factor scoring understates the most important decisions. Legal enforceability and verification integrity determine whether a pilot produces defensible results. The weights below reflect these priorities.

Factor | Weight | Receivables Score (1 to 3) | Inventory Score (1 to 3) |

Legal control readiness | 25% | 3 | 2 |

Verification feasibility | 20% | 3 | 1 |

Monitoring infrastructure | 20% | 2 | 1 |

Data integration readiness | 15% | 2 | 1 |

Borrower base availability | 10% | 3 | 2 |

Settlement complexity | 10% | 3 | 1 |

Weighted Total | 100% | 2.7 | 1.45 |

Sample scoring interpretation: The example above shows a typical SME lending bank where receivables score 2.7 (above the 2.4 threshold for pilot readiness) while inventory scores 1.45 (below 1.8, indicating significant gaps). Receivables win for most SME lending banks, while inventory wins only when warehouse infrastructure is already mature.

Score each factor from 1 to 3. Multiply by weight. Add results together. These thresholds are part of the TokenMinds pilot prioritization framework. A weighted total above 2.4 means the use case is ready for a 90-day pilot. Below 1.8 means gaps must be closed first. Between 1.8 and 2.4 suggests a 4-week preparation phase.

Scoring guide:

Legal control readiness scores 3 if perfection requirements are confirmed and documented. It scores 2 if the framework is understood but gaps exist. It scores 1 if requirements are unclear.

Verification feasibility scores 3 if system connectivity is in production. It scores 2 if integration is in development. It scores 1 if no integration exists.

Monitoring infrastructure scores 3 if automated alerts cover all key events. It scores 2 if partial automation exists. It scores 1 if monitoring is manual only.

Data integration readiness scores 3 if active API connections exist. It scores 2 if connections are planned. It scores 1 if no connections exist.

Borrower base availability scores 3 if a committed borrower with data access is identified. It scores 2 if one is in discussion. It scores 1 if none is identified.

Settlement complexity scores 3 if the settlement workflow is mapped and tested. It scores 2 if designed but untested. It scores 1 if design has not started.

Borrower Demand Validation

Borrower demand should not be treated as a sales assumption. Banks should confirm whether target borrowers already use invoice finance, warehouse financing, commodity storage, or trade credit lines. A pilot with strong legal design but weak borrower participation will not generate useful evidence.

Corridor-Specific Pilot Recommendations

The right use case depends on the market environment, not just internal readiness.

Domestic SME invoice finance with mature invoice networks. Receivables do better here. Invoice networks have independent validation. Legal assignment rules are often clearer in markets where invoice finance and receivables assignment are already common. Banks in Singapore, the UK, Australia and EU markets with active invoice networks should start with receivables.

Commodity export corridor with licensed warehouses. Inventory may do better, despite higher operational burden. Where licensed warehouses, established inspection firms and commodity price feeds exist, inventory builds on infrastructure already in place. Banks serving grain exporters, metals traders or energy commodity holders should evaluate inventory first.

Cross-border corridor without recognition of electronic documents. Neither use case is straightforward. Receivables face legal complexity for cross-border assignment. Inventory requires paper receipts in markets where electronic ones are not recognized. Banks in these corridors should pilot domestically first.

Emerging market with limited data infrastructure. Receivables with manual verification reduce the data dependency risk. Build toward automation in a second phase.

Corridor Type | Recommended First Pilot | Key Enabler Required |

Domestic SME, mature invoice network | Receivables | ERP or invoice system connectivity |

Commodity export, licensed warehouses | Inventory | Certified warehouse partner, written agreement |

Cross-border, no electronic document recognition | Receivables, domestic first | Domestic legal control confirmed first |

Emerging market, limited data | Receivables with manual verification | Structured debtor confirmation workflow |

Bank-Readiness Profiles

The right starting point also depends on the bank's existing capabilities.

Regional commercial bank with SME lending focus. Start with receivables. The borrower base already knows invoice financing. Legal assignment rules are well understood internally. The monitoring burden fits the existing credit review cycle.

Commodity-focused lender or trade finance specialist. Existing warehouse relationships and inspection flows exist. The written warehouse agreement and operator SLA framework fits current operations.

Large bank with capacity for parallel programs. Run both pilots with separate teams and separate governance. Each requires different legal counsel, operations staff, and borrower profiles. Parallel pilots produce comparative data that a sequential approach cannot.

Failure-Mode Controls

Knowing the failure modes is not enough. Banks need defined controls before the pilot begins.

Fake invoice. Require invoice data sourced directly from a verified system. Add a proof of completion check before pledge registration.

Duplicate invoice pledge. Check uniqueness against all previous submissions before taking any invoice. Require debtor confirmation via connected portal, not by email. Check any available cross-platform invoice registry before funding.

Assignment limitation provision. Review borrower agreements prior to facility set-up. Mark assignment limitations for legal review. Blacklist invoices from counterparties with existing limitations.

Duplicate warehouse receipt. Require receipts to carry a unique identifier tied to the operator's license. Register receipts in a central registry at issuance, not at pledge. Run duplication checks on all submitted receipts.

Quantity misrepresentation. Require independent physical inspection at origination. Set a mandatory re-inspection schedule. Freeze affected receipts on any quantity variance above 2 percent.

Warehouse operator failure. Include a step-in clause in the warehouse agreement. Confirm the clause is legally enforceable in the storage jurisdiction. Identify a replacement operator before the first lot is pledged.

Failure Mode | Use Case | Primary Control | Secondary Control |

Fake invoice | Receivables | System-sourced data only | Completion evidence check |

Duplicate pledge | Receivables | Uniqueness check | Cross-platform registry query |

Assignment restriction | Receivables | Contract review before facility | Exclude flagged counterparties |

Duplicate receipt | Inventory | Registry at issuance | Uniqueness check on all submissions |

Quantity misrepresentation | Inventory | Independent inspection | Freeze on variance above 2% |

Operator failure | Inventory | Step-in clause in agreement | Replacement operator identified |

Next step for receivables teams: Read Tokenized Receivables Collateral Guide 2026 for the full receivables lifecycle and verification framework.

Next step for inventory teams: Read Tokenized Inventory Collateral Guide 2026 for the full inventory lifecycle and warehouse receipt control framework.

12-Week Execution Roadmap

Stage | Weeks | Key Activities | Gate Criteria |

Legal validation | 1 to 2 | Confirm legal requirements, draft agreement templates, get legal sign-off | Written legal approval before data work begins |

Data integration | 3 to 5 | Connect data systems, test field mapping, validate uniqueness checks | Pass rate above 90% on test submissions |

Controlled testing | 6 to 9 | Run pledge, funding, and release simulations, test failure scenarios | Zero critical defects, all KPI baselines set |

KPI assessment | 10 to 12 | Run live transactions, measure six KPIs, complete go or no-go review | All sign-offs received before expansion |

Pilot KPIs to Measure

The six KPIs referenced in the roadmap are defined below:

KPI | Why it matters |

Legal sign-off completion | Confirms enforceability before expansion |

Data match pass rate | Tests verification quality |

Duplicate detection rate | Measures fraud control effectiveness |

Settlement release time | Measures operational efficiency |

Monitoring exception rate | Shows post-funding control burden |

Borrower participation rate | Confirms real borrower demand |

Next step after pilot selection: Read How to Build a Collateral Eligibility Engine for Receivables and Inventory for how eligibility rules translate into system requirements after pilot prioritization.

Request a Collateral Pilot Prioritization Workshop With TokenMinds

Choosing the right use case is the first decision. Scoping the pilot, designing phase gates, and mapping legal and operational requirements are the harder steps.

TokenMinds helps trade finance and innovation leads design the weighted scoring model, corridor analysis, and governance framework for collateral pilots.

Frequently Asked Questions

Q: Should banks tokenize receivables or inventory first?

A: Most banks should start with receivables when invoice data and legal assignment workflows already exist. Inventory is better suited for banks with established warehouse and inspection infrastructure.

Q: Which use case is faster to execute in 90 days?

A: Receivables are typically faster when system connectivity exists. The verification steps are data driven. Inventory pilots need a physical inspection partner, a certified warehouse and a written agreement before testing begins. These add 2 to 4 weeks to the preparation phase.

Q: Can a bank run both pilots at the same time?

A: Yes, but only with separate teams and separate governance. Running both in the same team creates resource conflicts. A large bank with dedicated trade finance and commodity desks can run parallel pilots if phase gates and KPIs are tracked separately.

Q: What is the biggest operational difference between the two?

A: Post-funding monitoring. Receivables monitoring is cyclical with invoice maturity. Inventory monitoring is continuous. It requires physical inspections, insurance tracking and price surveillance throughout the life of the loan. Banks without a dedicated collateral management function will find inventory monitoring significantly harder in the first pilot.

References

Bank for International Settlements: "Tokenisation of deposits and other financial assets" (othp92). Documents real-world tokenization initiatives and discusses Credix and AmFi using tokenized receivables as collateral for credit lines.

UNCITRAL–UNIDROIT: “Model Law on Warehouse Receipts 2024.” Supports modern warehouse receipt systems, including electronic and paper-based receipts, and explains how stored goods can be used as collateral.