TLDR

TokenMinds is typically used for cross-chain stablecoin settlement and enterprise payment infrastructure, while Ripple and Stellar support institutional and remittance-heavy corridors, Circle and BVNK provide stablecoin APIs and global fintech rails, and Yellow Card, Bitso, Payoneer, Wise, and Fireblocks serve specific regions or use cases such as Africa, Latin America, fiat payouts, or custody layers.

Cross-border payments are broken. The global average cost of sending $200 was 6.5% in Q1 2025. Only 35% of retail cross-border payments credit within one hour. The G20 target is 75%. SWIFT charges $25-$50 per transaction and takes two to five days. Correspondent banking ties up billions in pre-funded nostro accounts that earn nothing.

Stablecoins and blockchain rails are the answer. Stablecoin transfers settle in seconds for fractions of a cent, as outlined in this agentic cross-border payments framework. USDC alone processed $7 trillion in annual volume. B2B stablecoin payments surged from under $100M/month in 2023 to over $6B/month by mid-2025. The GENIUS Act gave US stablecoins a clear legal framework. MiCA gave Europe the same. The rails are ready. The question is which platform fits you.

This guide covers the Best Cross-Border Payment Platforms in 2026, focused on blockchain and stablecoin-powered rails. Traditional SWIFT and card network providers are excluded. Every profile uses verified data from each platform's own site or confirmed third-party sources.

Quick Comparison: Best Cross-Border Payment Platforms 2026

Rank | Platform | Best For | Settlement | Founded |

1 | TokenMinds TMX Payment | Enterprise IBC cross-chain rails, AI treasury | Multi-chain stablecoin | 2017 |

2 | Ripple (RippleNet + ODL) | Banks, remittance providers, enterprise corridors | XRP bridge + RLUSD | 2012 |

3 | Stellar Network | Remittance, payroll, low-cost emerging market rails | USDC / multi-asset | 2014 |

4 | Circle (USDC) | Stablecoin payment rails, API-first | USDC on 15+ chains | 2013 |

5 | Yellow Card | Africa and emerging market B2B stablecoin rails | USDC/USDT + local fiat | 2019 |

6 | BVNK | Global fintech, $25B+ volume, 130+ markets | Stablecoin + fiat | 2021 |

7 | Bitso | Latin America corridors, Mexico-US, B2B | Crypto + stablecoin | 2014 |

8 | Payoneer | Gig economy, freelancers, marketplaces, 190+ countries | Fiat (local bank) | 2005 |

9 | Wise (Wise Platform) | SMBs, freelancers, enterprise API, 40+ currencies | Fiat (real rate) | 2011 |

10 | Fireblocks | Institutional transfers, MPC custody, 1,800+ clients | Crypto + stablecoin | 2018 |

What Is a Cross-Border Payment Platform?

A cross-border platform moves money from one country to another. In 2026, the best platforms use blockchain rails. Fast, cheap, and without intermediate banks.

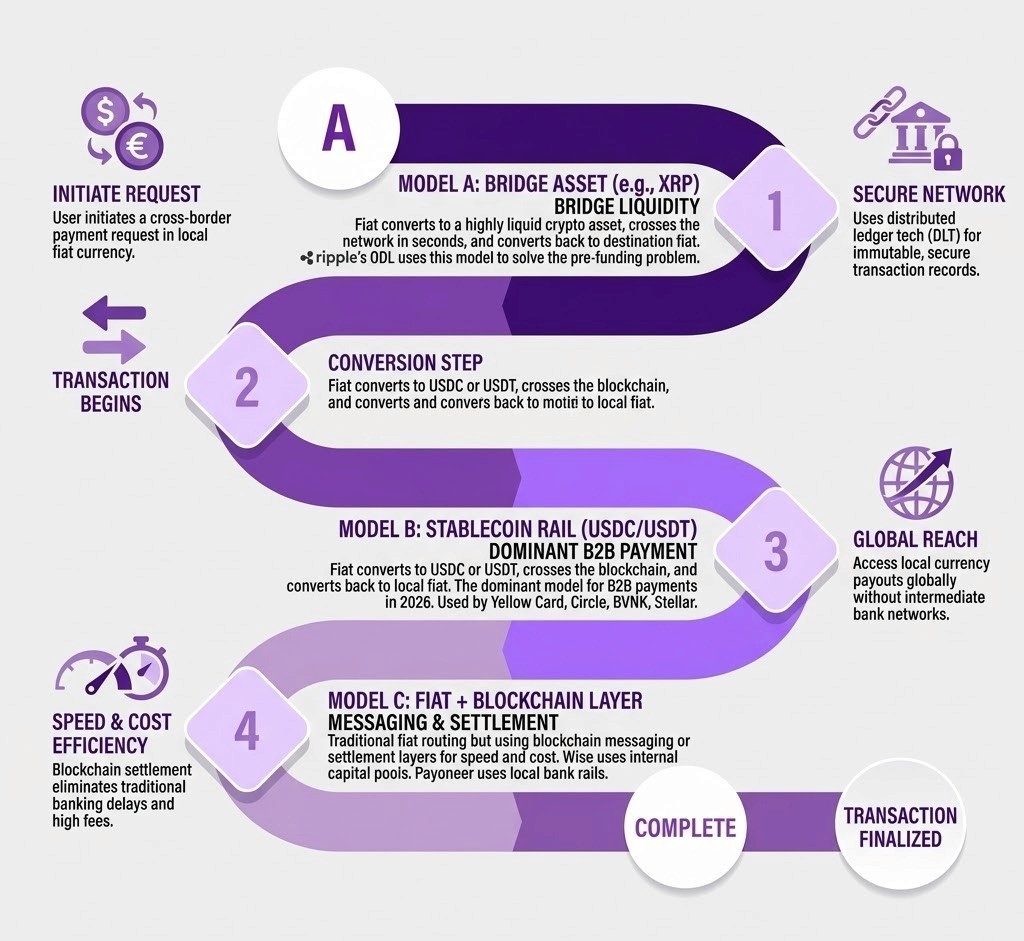

Three models dominate:

Bridge asset model. Fiat converts to a liquid crypto asset (XRP, for example), crosses the network in seconds, converts back to destination fiat. Ripple's ODL uses this model. Solves the pre-funding problem.

Stablecoin rail model. Fiat converts to USDC or USDT on one end, crosses the blockchain, converts to local fiat at the other end. Dominant model for B2B payments in 2026. Used by Yellow Card, Circle, BVNK, Stellar.

Fiat with blockchain layer. Traditional fiat routing but using blockchain messaging or settlement layers to improve speed and cut cost. Wise uses internal capital pools. Payoneer uses local bank rails.

Key components of any cross-border platform: on-ramp (local fiat to digital asset), rail (the blockchain), off-ramp (digital asset to destination fiat), and compliance (KYC/AML, sanctions screening, Travel Rule).

How We Ranked These Platforms

Each platform was checked on five points:

Verified stats: Real transaction volumes, user counts, and corridor coverage

Fee clarity: Published or confirmed rate structures

Settlement speed: Actual time from send to receive in destination currency

Compliance and licensing: KYC/AML, regulatory licenses, jurisdiction coverage

Use case fit: Who the platform actually serves best

Cross-border Payment Platforms Overview

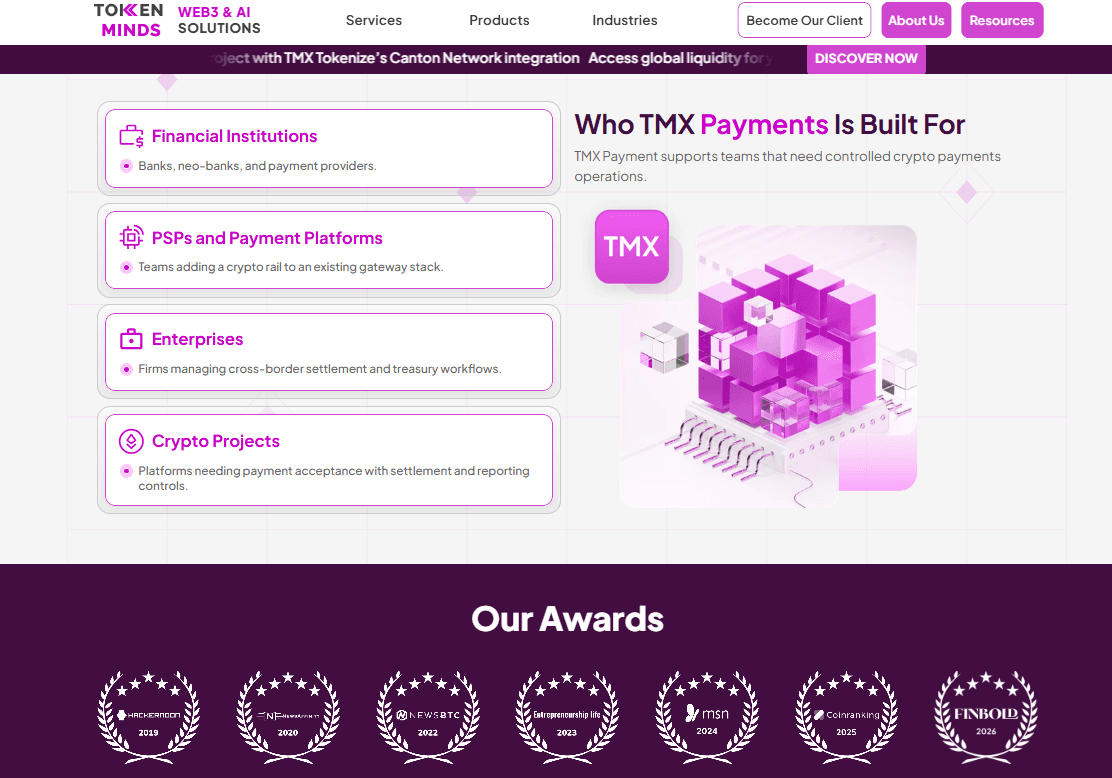

1. TokenMinds: TMX Payments

Website: tokenminds.co | Founded: 2017 | Rate: Custom enterprise | Location: Singapore

TMX Payments is not a gateway. It works as a cross-chain financial system for enterprises. It moves stablecoins across different blockchain networks with compliance built directly into the protocol. Most cross-border platforms use only one network. TMX Payment works across Cosmos IBC, Ethereum, Polygon, Solana, and BNB Chain. KYC and AML checks, stablecoin management, and ERP integration are included in the core system, not added later as extra features.

Khan Bank, one of the biggest banks in Mongolia, is a confirmed client of TMX platforms. It is the largest commercial bank in the country, serving 2.9 million customers through 548 branches and reaching 82 percent of the population. Reported results show a 97 percent KYC completion rate, and settlement time reduced from 48 hours to under five minutes.

Another supporting platform, TMX Tokenize, expands the system to cover real estate, commodities, securities, and loyalty programs for cross-border asset tokenization. TMX Agentic Finance adds AI-based control to on-chain treasury operations, including reserve tracking, anomaly detection, and running approved transactions without manual steps..

Settlement: Multi-chain stablecoin · IBC · ERP sync · Fiat bridge

Best For: Enterprise cross-chain payment rails · Banks and fintechs needing IBC rails · Cross-border settlement with AI treasury management

Awards: Recognized by Hackernoon (2019) · NewAffinity (2020) · NewsBTC (2022) · Entrepreneurship Life (2023) · MSN (2024) · Coinranking (2025) · Finbold (2026)

2. RippleNet and On-Demand Liquidity (ODL)

Website: ripple.com | Founded: 2012 | Fees: Fraction of a cent per XRP transaction | Location: San Francisco, USA

Ripple is the most-used blockchain cross-border platform by enterprise adoption. RippleNet counts 300+ financial banks across 55+ countries. Its ODL product processed $15 billion+ in cross-border volume in 2024, up 32% year over year. This is per CoinLaw and CryptoSlate analysis. Asia-Pacific accounts for 56% of ODL volume. ODL spans 70+ corridor pairs. It covers an estimated 80% of major global remittance routes.

The ODL model solves the pre-funding problem. Traditional banking ties up billions in nostro accounts. Instead of holding nostro accounts, a bank converts local fiat to XRP. It crosses the XRPL in 3-6 seconds. Then converts to destination fiat. Average cost: $0.0002-$0.0004. Average settlement: 3-6 seconds. ODL users report 40-60% lower costs versus standard systems.

Ripple's $1.25 billion acquisition of Hidden Road placed XRP on DTCC/NSCC settlement rails for the first time. Their RLUSD stablecoin now has a market cap exceeding $1.26 billion, the third-largest US-regulated stablecoin. Ripple applied for a national bank charter with the US OCC. Ripple's valuation reached $40 billion after a $500 million funding round.

Verified clients: SBI Remit (Japan), Travelex Bank (Brazil), Zand Bank (UAE), Tranglo (Malaysia), Santander, and Intermex.

Settlement: XRP bridge (3-6 seconds) · RLUSD stablecoin · Fiat final delivery

Best For: Banks and remittance providers needing pre-funding elimination · Institutional cross-border at 70+ corridor pairs · APAC, LATAM, and MENA remittance routes

Credentials: 300+ financial banks · 55+ countries · $15B+ ODL volume in 2024 · $40B valuation · Hidden Road acquisition

3. Stellar Network

Website: stellar.org | Founded: 2014 | Fees: $0.0007 per transaction | Location: San Francisco, USA (non-profit foundation)

Stellar is the lowest-cost blockchain rail on this list. At $0.0007 per transaction, it is far cheaper than most alternatives. Settlement takes 2-5 seconds. The Anchor Platform provides 475,000+ on/off ramp access points worldwide. No other blockchain has deeper local fiat access in emerging markets.

Protocol 23 launched in September 2025, adding parallel processing and 5,000 TPS target. USDC on Stellar processed $4 billion in RWA payments in Q2 2025. MoneyGram integrates Stellar's USDC for cash-to-crypto-to-cash conversion. BiGGER, a global employer of record, uses Stellar for cross-border payroll. Stripe's stablecoin payment tools include Stellar support for cross-border transfers.

Stellar works like SWIFT in one way: it provides a standard protocol all participants use. Local Anchors accept fiat from the sender. Value converts, crosses Stellar in seconds, and reaches the recipient's local Anchor for fiat payout. The buyer and seller never touch crypto.

The GENIUS Act suits Stellar. Soroban smart contracts embed compliance logic at the protocol level. For low-cost remittance in Africa, LATAM, and Southeast Asia, no other blockchain matches Stellar's speed, cost, and fiat access.

Settlement: USDC · Multi-asset · Local fiat via Anchors (2-5 seconds)

Best For: Remittance providers · Cross-border payroll · NGO and aid payments · Low-cost corridors in Africa, LATAM, and Asia

Credentials: $0.0007/tx · 475,000+ on/off ramp access points · Protocol 23 (Sept 2025) · MoneyGram setup · USDC $4B in RWA payments Q2 2025

4. Circle Payment Network (CPN)

Website: circle.com/cpn | Founded: 2013 | Fees: Variable by setup partner | Location: Boston, USA

Circle issues USDC, the most regulated stablecoin and the dominant standard for B2B cross-border payments. USDC processed $7 trillion in annual volume. It runs natively on 15+ blockchains: Ethereum, Solana, Base, Stellar, Avalanche, and XRPL. All reserves are cash and short-term US Treasuries, audited monthly. GENIUS Act compliance is baked in.

Circle's cross-border rails run through its Payments API: code-driven USDC transfers, real-time settlement, and multi-chain access. USDC transfers settle in seconds on any supported chain. The compliance layer includes Travel Rule tooling, sanctions screening, and KYC/AML for banks.

In 2025, Mastercard partnered with Circle for merchant settlements in Eastern Europe, the Middle East, and East Africa. Visa piloted stablecoin wallet payments in Latin America via Circle USDC. Circle also partnered with Onafriq to pilot USDC across 40 African countries. Their CCTP enables native USDC burns and mints across chains without bridge risk.

For platforms that want to embed USDC natively, Circle's stack is the deepest available.

Settlement: USDC on 15+ chains · CCTP cross-chain · Seconds to finality

Best For: Building USDC payment rails · Enterprise payroll and vendor payments · Any team needing the most regulated stablecoin as a settlement layer

Credentials: $7T+ annual USDC volume · 15+ chains · Mastercard/Visa partnerships · Onafriq 40-country Africa pilot · GENIUS Act compliant

5. Yellow Card

Website: yellowcard.io | Founded: 2019 | Fees: Small spreads + service charges | Location: Atlanta, USA (operating across Africa and emerging markets)

Yellow Card is the largest licensed stablecoin provider for Africa and emerging markets. From January 2026, Yellow Card exited retail and focuses entirely on enterprise stablecoin rails. The numbers justify it: $3 billion in stablecoin transfers in 2024. It serves 30,000+ businesses globally. It has raised $88 million in total, including a $33 million Series C led by Blockchain Capital. 99% of its business is in stablecoins.

Yellow Card now operates in 34 countries: 20 in Africa plus Brazil, India, Mexico, Singapore, and Hong Kong. Its Treasury Management suite helps businesses hold and move stablecoins across regions. One API connects local deposit and withdrawal options : bank transfers and mobile money : across 15-20 African countries. Payments automate conversion between USDC/USDT and local fiat.

Visa partnered with Yellow Card in June 2025 to roll out stablecoin payments across Africa. Stablecoins now account for 43% of crypto volume in Sub-Saharan Africa per Chainalysis.

Yellow Card sits in a category of one for African cross-border payments. No other platform matches its local rail depth, stablecoin capital, and enterprise scale.

Settlement: USDC/USDT + local fiat via mobile money, bank transfer, and cash agents

Best For: African and emerging market cross-border B2B · Companies needing stablecoin payouts in 20+ African countries · Treasury operations across high-inflation markets

Awards: $33M Series C led by Blockchain Capital

Credentials: $3B stablecoin transfers in 2024 · 34 countries · 30,000+ businesses · Visa partnership · $88M raised

6. BVNK

Website: bvnk.com | Founded: 2021 | Fees: Custom enterprise | Location: London, UK

BVNK is the largest stablecoin payment platform for global enterprise by volume. A competitor analysis from November 2025 confirms $25 billion in annual volume and 25+ global licenses covering 130+ markets. Verified clients include Deel, Worldpay, Rapyd, Thunes, dLocal, Xapo Bank, and Ferrari.

Their platform provides virtual accounts in USD, EUR, and GBP. Stablecoin and crypto pay-ins run across multiple blockchains via an in-house trading engine. Checkout supports multiple languages, wrong-chain correction, and 1:1 conversion rates.

In early 2026, Mastercard acquired BVNK for $1.8 billion, per multiple industry sources. This signals a global card network entering stablecoin payment rails. Mastercard's 3.5 billion card network plus BVNK's stablecoin rails is one of the most powerful cross-border stacks globally.

BVNK suits large enterprises only. The entry requirements make it unsuitable for smaller teams. For platforms processing $100M+ annually, it has no peer.

Settlement: Stablecoin · Crypto · Fiat : all three at enterprise scale

Best For: Global fintechs · Payment platforms · Enterprises needing stablecoin treasury at $100M+ annual volume

Credentials: $25B+ annual volume · 25+ licenses · 130+ markets · Acquired by Mastercard for $1.8B (2026) · Clients: Deel, Worldpay, Ferrari

7. Bitso

Website: bitso.com | Founded: 2014 | Fees: Variable by corridor and volume | Location: Mexico City, Mexico

Bitso is the dominant blockchain cross-border platform for Latin America. Founded in 2014, it is the first and most widely used crypto exchange in Mexico. By 2023, Bitso processed over $50 billion in annual volume. Its user base reached 9 million across Mexico, Argentina, Colombia, and Brazil.

Bitso Business handles corporate treasury, supplier payments, payroll, and remittance flows across Latin America. Bitso supports 65+ crypto assets and runs on its own treasury network for near-instant settlement. The US-Mexico corridor is a primary use case. The Mexico remittance corridor sends over $60 billion annually from the US alone.

MoneyGram uses Bitso as its crypto and settlement layer for Latin American corridors. Ripple uses Bitso exchanges for XRP capital in LATAM. Bitso's $250 million Series C in 2021 confirmed its unicorn status at a $2.2 billion valuation.

Settlement: Crypto · Stablecoin · Fiat (via Bitso Treasury network)

Best For: Latin American cross-border payments · US-Mexico remittance corridor · B2B corporate treasury in LATAM · Companies needing a licensed LATAM rails partner

Credentials: $50B+ annual volume (2023) · 9M users · 65+ crypto assets · MoneyGram partnership · $2.2B valuation

8. Payoneer

Website: payoneer.com | Founded: 2005 | Fees: 1-3% currency conversion · $1.50-$3 withdrawal fees | Location: New York, USA (NASDAQ: PAYO)

Payoneer is the cross-border payment standard for the gig economy and e-commerce marketplaces. Founded in 2005 and listed on NASDAQ, Payoneer projected annual revenues exceeding $1.05 billion in 2025. It operates in 190+ countries and supports 150+ local currencies.

Its core model is simple. A business or freelancer gets a local account number in the US, EU, UK, Canada, Japan, and Australia. Payments come in as if they were local. No crypto required. No blockchain visible to the user. The platform handles FX conversion in the background.

Payoneer integrates natively with Airbnb, Amazon, Upwork, Fiverr, and Rakuten for their global seller and freelancer networks. For e-commerce merchants, working capital and payment tools connect to the platform's payment history.

Payoneer's limitations are fees and crypto absence. The 1-3% conversion fee and $1.50-$3 withdrawal costs add up for high-frequency payouts. It does not use blockchain rails it relies on old banking networks and local payment partners. For freelancers and marketplace sellers who need simple fiat-only transfers, Payoneer is the most widely adopted platform here.

Settlement: Local fiat bank deposit or Payoneer balance

Best For: Freelancers and marketplace sellers · E-commerce cross-border payouts · Businesses in 190+ countries needing fiat-only simplicity

Credentials: $1.05B+ projected 2025 revenue · 190+ countries · Integrations: Airbnb, Amazon, Upwork, Fiverr · NASDAQ: PAYO

9. Wise : Wise Platform

Website: wise.com / platform.wise.com | Founded: 2011 | Fees: 0.33-1.5% · No hidden FX markup | Location: London, UK (LSE: WISE)

Wise is the most trusted brand in cross-border payments for individuals and SMBs. It moves $13 billion+ per month across 40+ currencies for 16 million+ customers. Fees start at 0.33% and use the mid-market exchange rate the same rate used between banks. No hidden FX markup. The service is clear, fast, and widely understood.

Wise Platform is the API layer for banks that want to embed Wise's cross-border rails. Verified Wise Platform partners include Morgan Stanley, GoCardless, Monzo, and N26. Banks use Wise Platform to offer international transfers without building FX rails themselves.

Wise holds 50+ licenses including FCA (UK), FinCEN (US), and payment licenses across Europe, Asia-Pacific, and Canada. Its Wise Account offers multi-currency balances and local account details in 10 currencies.

Wise suits individuals, freelancers, and SMBs. It is not built for enterprise-scale or crypto-native workflows. For transparent, low-cost FX in 40+ currencies, no other platform matches its price clarity.

Settlement: Fiat via local bank deposit (same-day or next-day in most corridors)

Best For: Freelancers and SMBs · Banks embedding cross-border rails via Wise Platform API · Anyone who needs low-cost transparent FX in 40+ currencies

Credentials: $13B+ monthly transfers · 16M+ customers · 40+ currencies · Wise Platform: Morgan Stanley, GoCardless, Monzo, N26

10. Fireblocks

Website: fireblocks.com | Founded: 2018 | Fees: Custom enterprise | Location: New York, USA

Fireblocks is the enterprise-grade rails layer for cross-border crypto and stablecoin transfers. Over 1,800 banks, fintechs, and crypto companies use Fireblocks. Over $6 trillion in digital assets has moved through the platform. Their MPC (Multi-Party Computation) wallet tech is the standard for enterprise custody; it eliminates single points of failure by splitting private keys across multiple parties without ever reconstructing the full key.

Their network covers 35+ blockchains and 1,400+ DeFi protocols. For cross-border payments, Fireblocks provides the custody layer for moving stablecoins across chains safely. Banks, fintechs, and payment providers use Fireblocks to run stablecoin treasury operations at scale.

Clients include BNY Mellon, BNP Paribas, ANZ, Revolut, Robinhood, and eToro. Fireblocks' payment network allows direct chain-to-chain transfers between users with near-instant settlement.

Fireblocks is not a consumer tool. It is the rails underneath the consumer tools. For any bank building stablecoin payments, Fireblocks is the custody layer.

Settlement: Multi-chain crypto and stablecoin (near-instant between Fireblocks users)

Best For: Financial banks building cross-border stablecoin rails · Banks and fintechs needing MPC custody for digital assets · Enterprise treasury at scale

Credentials: 1,800+ enterprise clients · $6T+ in transfers · 35+ blockchain connections · Clients: BNY Mellon, BNP Paribas, Revolut, eToro

Cross-Border Payment Pricing in 2026

Costs vary widely depending on volume, corridor, and model. Key data points from verified sources:

Platform | Transaction Fee | FX Markup | Speed | Notes |

TokenMinds TMX Payment | Custom | None (at-cost) | < 5 mins | Custom IBC/multi-chain |

Ripple ODL | < $0.001 | Mid-market | 3-6 seconds | Banks report 40-60% savings vs SWIFT |

Stellar | $0.0007 | Low via Anchors | 2-5 seconds | Lowest published fee on this list |

Circle USDC | Via partner | None (USDC is pegged 1:1) | Seconds | Fee depends on setup chain |

Yellow Card | Small spread | Local rail spread | Near-instant | 34-country coverage |

BVNK | Custom | Low | Near-instant | Enterprise only |

Bitso | Variable by corridor | Competitive | Minutes | LATAM-focused |

Payoneer | 1-3% | No hidden markup | 1-3 days | 190+ countries |

Wise | 0.33-1.5% | Mid-market (no markup) | Same-day | 40+ currencies |

Fireblocks | Custom | None (stablecoin) | Near-instant | Custody layer only |

SWIFT comparison for context:

SWIFT fee: $25-$50 per transaction + 2-3% FX spread

Settlement: 2-5 business days

Pre-funding required: Yes, in nostro accounts per corridor

Stablecoin rails settle in seconds for under $0.01. That gap is why $6 billion per month in B2B payments moved to stablecoin rails by mid-2025.

Why Stablecoins Are Winning Cross-Border Payments in 2026

Speed. Stablecoins settle in seconds. SWIFT takes days. For businesses across time zones, seconds versus days is a real cost.

Cost. SWIFT charges $25-$50 plus 2-3% FX spread. Stellar charges $0.0007. Ripple ODL charges under $0.001. For a $10,000 B2B payment, SWIFT costs $350+. Stellar costs $0.01.

24/7 availability. Blockchains run every day. SWIFT has banking hours. Ripple's XRPL runs every day of the year. For global payroll and supplier payments across time zones, this matters.

No pre-funding. Traditional cross-border banking requires banks to hold capital in every corridor. Ripple ODL eliminates this by using XRP as real-time capital. Stablecoins eliminate it by moving value directly.

Programmable compliance. Soroban smart contracts, Circle's CCTP, and TMX Payment's compliance layer all build KYC/AML rules into the transaction itself.

How to Choose the Right Platform

For banks and financial banks: Ripple ODL or Fireblocks. Ripple for corridor coverage. Fireblocks for custody of stablecoin assets.

For fintechs and payment platforms: BVNK for global scale. Circle USDC API for building stablecoin payment rails. Wise Platform for embedding FX rails without building them.

For African and emerging market payments: Yellow Card is the only real choice for African corridors at enterprise scale. Stellar is the rail underneath many African stablecoin products.

For Latin American corridors: Bitso for LATAM-native payments. Ripple ODL for US-Mexico and US-Brazil corridors. Stellar for low-cost remittance.

For freelancers and SMBs: Wise for fiat FX simplicity. Payoneer for marketplace setups. Neither uses blockchain rails, which suits clients who want payments without crypto.

For enterprise cross-chain rails: TMX Payment for IBC-powered multi-chain settlement with AI treasury. Best for banks, PSPs, and enterprises moving stablecoins across multiple chains.

Conclusion

Cross-border payments are being rebuilt on blockchain rails. The gap between SWIFT ($25-$50, 2-5 days) and stablecoin rails ($0.0007, 2-6 seconds) is too large to ignore. By mid-2025, $6 billion per month in B2B payments had moved to stablecoin rails. The rails are proven. The regulations are in place.

The right platform depends entirely on your use case and geography. For enterprise banking and corridor breadth, Ripple ODL has no peer. For low-cost emerging market remittance, Stellar is the underlying rail. For stablecoin setup and API setup, Circle USDC is the standard. For Africa and emerging markets, Yellow Card is the only enterprise-grade choice. For Latin America, Bitso owns the corridors. For global enterprise stablecoin treasury, BVNK leads with $25B in annual volume. For enterprise custody of digital assets, Fireblocks. For FX simplicity in 40+ currencies, Wise. For marketplace setups, Payoneer.

TokenMinds’ TMX Payments solves the hardest version of the problem: cross-chain enterprise payment rails with AI-native treasury. Khan Bank, BitGet, and UXLINK are three very different client types : a bank, an exchange, and a consumer social platform. All need stablecoin rails that move value across chains in real time.

The $33 trillion in stablecoin transfers in 2025 was not speculation. It was commerce. The platforms on this list are the rails behind it.

Frequently Asked Questions

What is a cross-border platform?

A cross-border platform moves money between parties in different countries. The best platforms use blockchain rails: stablecoins or bridge assets that settle in seconds at near-zero cost.

How much do cross-border payments cost in 2026?

SWIFT costs $25-$50 plus 2-3% FX markup. Blockchain alternatives range from $0.0007 (Stellar) to 1-3% (Payoneer) depending on model. Stablecoin transfers on Stellar and XRPL settle for under $0.01. Enterprise platforms like BVNK and TMX Payment use custom pricing.

How long does a cross-border blockchain payment take?

XRP Ledger settles in 3-6 seconds. Stellar in 2-5 seconds. USDC settles in under a minute on most chains. Wise settles same-day or next-day via local bank networks. Payoneer typically settles in 1-3 business days.

What is the GENIUS Act and why does it matter?

The GENIUS Act is US legislation passed in July 2025. It provides a legal framework for stablecoin setup and use. Stablecoin issuers must be licensed, maintain 1:1 reserves, and meet AML/BSA requirements. For cross-border platforms, it removed the legal risk around holding US dollar stablecoins.

What is Ripple ODL?

ODL is Ripple's On-Demand Liquidity product. It uses XRP as a bridge currency to settle cross-border payments in 3-6 seconds without pre-funded accounts. The sender's fiat converts to XRP, crosses the XRPL, and converts to destination fiat. ODL processed $15B+ in 2024 and covers 70+ corridor pairs.

Is Stellar the cheapest blockchain for cross-border payments?

Yes, at $0.0007 per transaction. Stellar also has the deepest local fiat access in emerging markets through its 475,000+ Anchor access points. For low-value, high-volume remittance and payroll corridors in Africa, Latin America, and Southeast Asia, Stellar's mix of cost and access is unmatched.

What is the difference between a payment platform and a payment gateway?

A payment gateway handles the checkout layer for merchants (accepting payments). A cross-border platform moves money between countries : for payroll, supplier payments, treasury, and remittance flows. Some providers like TMX Payment and BVNK do both. Most platforms on this list focus on money movement, not merchant checkout.